Will the Bank of England cut interest rates this month?

- Go back to blog home

- Latest

14 January 2020

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The last 24 hours or so have been pretty remarkable as far as UK interest rate expectations are concerned.

First, fellow MPC member Silvana Tenreyro claimed on Friday that UK growth was likely to undershoot the bank’s November projections and that she would support a rate cut should the economy continue to slow. Gertjan Vlieghe, who joined the rate-setting board in 2015, was even more forthright in his comments over the weekend, saying that he would vote for a rate cut this month, barring an ‘imminent and significant’ turnaround in UK growth data.

This aforementioned data took a significant turn for the worse on Monday, with the UK economy contracting by 0.3% in November alone according to monthly data from ONS. This was well short of expectations and dragged the three-month rolling growth number to 0.3% quarter-on-quarter. Manufacturing and industrial production also posted sharp contractions during the month, the latter putting in its worst performance since April 2019.

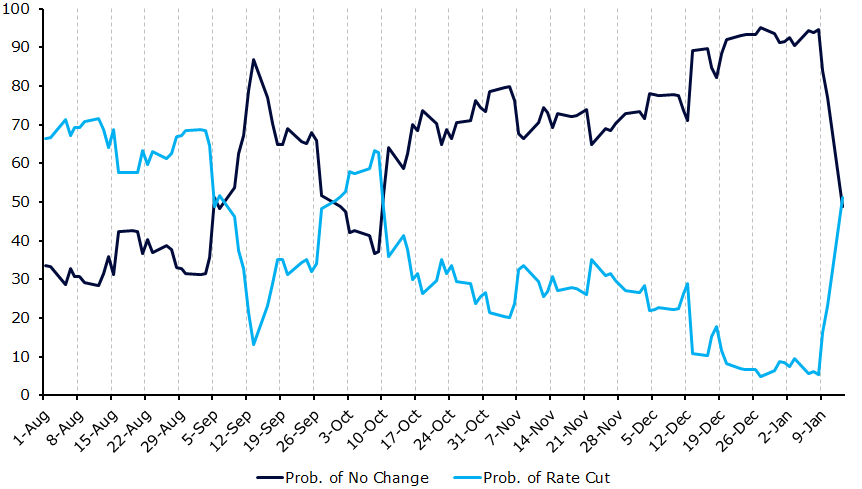

Investors quickly reacted by selling the pound, sending the currency around half a percent lower against the dollar back below the 1.30 level. Expectations for immediate Bank of England action were also ramped up aggressively, with futures markets now placing a greater than 50% chance of a rate cut at the bank’s next meeting on 30th January (Figure 1).

Figure 1: Bank of England Interest Rate Market Pricing [January 2020]

While we acknowledge that the chances of a cut later this month have undoubtedly increased in the past few days, we think that the market has slightly overreacted. It is worth stressing that the three BoE members (Carney, Vlieghe and Tenreyro) all noted that additional data would be required before they decide on whether to vote for lower rates. The November growth data does, of course, encompass a period before the general election, a time of intense political uncertainty and heightened concerns surrounding a ‘no deal’ Brexit.

For a January cut to become a reality, we think that we would need to see signs that business and consumer confidence has not recovered since the election to the extent that would ensure a continued slowdown in UK growth at the beginning of 2020. The January PMIs, out on 24th, now take on added importance. Any sign of a continued slowdown here would undoubtedly increase the chances of a rate cut later this month.

US-China set to sign ‘phase 1’ trade deal

Aside from the pound, the other major currencies spent much of trading yesterday relatively rangebound. EUR/USD ticked higher slightly, although with macroeconomic and political news at a premium, there was very little volatility to write home about.

Investors are instead gearing up for the eventual signing of the ‘phase one’ trade deal between the US and China, which is expected to take place in the White House tomorrow. With the signing of the deal on track and the US-Iran spat seemingly on the path to de-escalation, traders have piled into equities and reduced holdings of the safe-havens. The S&P 500, Nasdaq and indeed the MSCI world equity index all hit record highs on Monday, while government bond yields in the US and Euro Area also rose. While the reaction in the FX market has been relatively limited, we think that the avoidance of additional negative headlines on these fronts should be good news for emerging markets in the coming weeks.

Next up in the markets will be this afternoon’s US inflation data, which is generally key for Federal Reserve policy.

SHARE