FOMC March Meeting Preview

- Go back to blog home

- Latest

18 March 2019

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Will the Federal Reserve signal the end of its rate hike cycle next week?

At the FOMC’s December meeting, when the most recent set of rate forecasts were released, the central bank indicated that it was on course to raise interest rates at a much slower pace in 2019 than in 2018. The Fed’s so-called ‘dot plot’, which shows where each member of the committee expects rates to be at the end of each year, showed that policymakers expected to hike on two occasions this year, compared to the four hikes from last year.

Since then, however, the Fed has executed a sharp U-turn on policy, taking on a far more dovish stance during recent communications. Fed Chair Jerome Powell struck a cautious tone following the bank’s January meeting, removing the phrase that risks to the outlook were ‘roughly balanced’ and stating that the case for additional hikes had ‘weakened’. Powell has also recently indicated that rates may be around the estimated ‘neutral’ level, which ensures both steady long-term inflation and on trend growth.

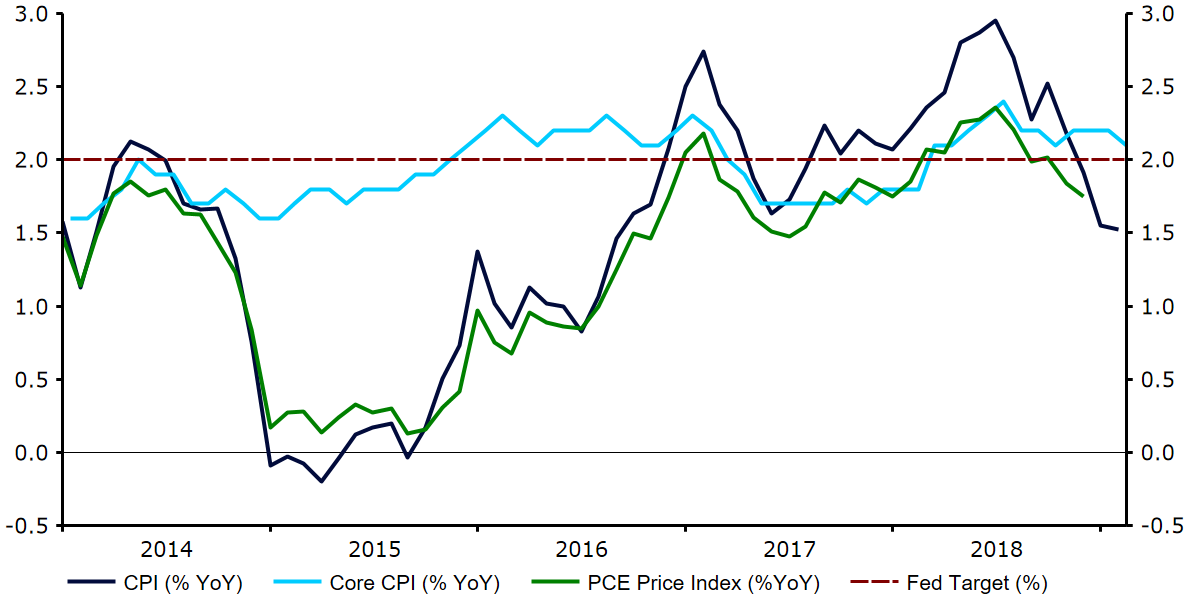

This dramatic shift in stance from the Fed has, we believe, been in large part due to a downturn in domestic macroeconomic data, in particular a slowdown in US inflation. The headline rate of consumer price growth has fallen to just 1.5% in the past couple of months (Figure 1), now fairly comfortably below the 2% target for the first time since mid-2017.

Figure 1: US Inflation Rate (2014 – 2019)

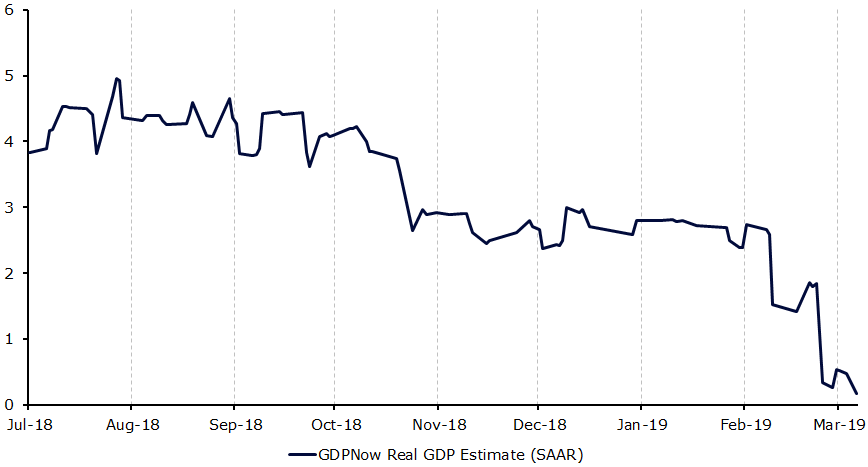

Generally weaker domestic activity data since the January meeting, particularly out of the manufacturing sector and retail sales, have also somewhat quelled the narrative surrounding a divergence in economic performance between the US and the rest of the developed world. The Atlanta Fed’s so-called GDPNow growth forecast, which provides a timely running estimate of overall US economic activity based on previously released data, has declined sharply so far in 2019 (Figure 2). The indicator suggests that the US economy may now only be set for negligible growth of 0.3% SAAR (seasonally adjusted annual rate) in the first quarter. This is a considerably slower pace than recorded throughout 2018.

Figure 2: Atlanta Fed’s US GDPNow Estimate (July ‘18 – Mar ‘19)

, The growing emergence of downside risks from abroad also presents a risk to the US outlook and should lessen the need for additional policy tightening from the Fed this year. Global growth has slowed, particularly in China and the Eurozone, while uncertainty stemming from the Brexit process and concerns over global trade do not provide a conducive environment for higher rates. While we don’t think that a recession is on the cards in the US any time soon, it appears that the world’s largest economy is more likely to be in a cooling off phase than at risk of overheating.

Given the above, we think that a further downward revision to the FOMC’s ‘dot plot’ at next week’s meeting is highly likely. We expect the bank’s projections to show that the median committee member does not expect to hike interest rates at all in 2019. This would also entail a lowering of its long term equilibrium rate forecast to around, or modestly above, current levels, putting the Fed’s projections much more in line with that of the market. Fed fund futures are now showing less than a 5% implied probability of at least one hike from the FOMC this year and a non-negligible chance of a rate cut.

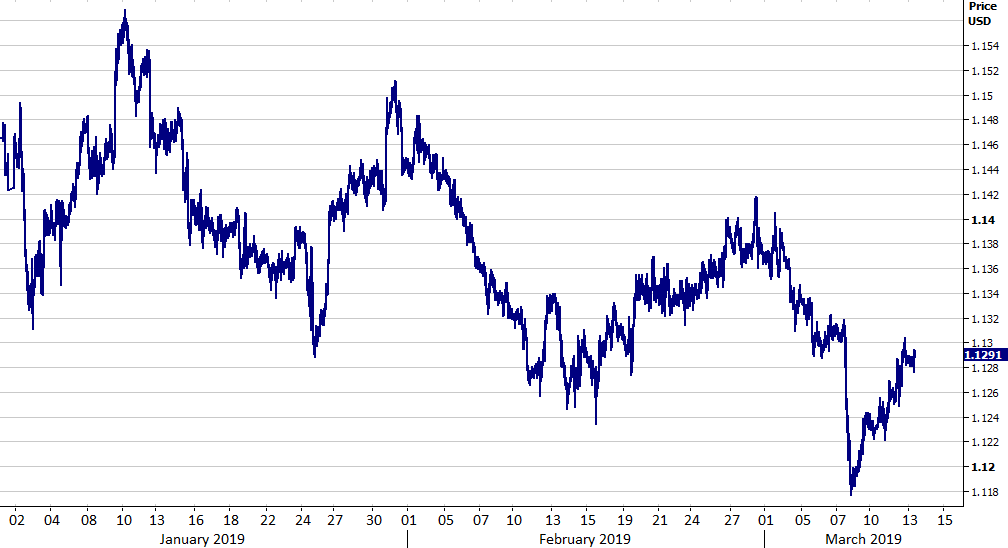

Currency traders have, however, largely overlooked Fed dovishness so far in 2019. Investors have instead sold the Euro hard on the generally downbeat set of data out of the Eurozone and the subsequent dovish turn from the European Central Bank at its March meeting. The common currency recently fell to its weakest position in twenty-one months, albeit has begun to recoup some of these losses (Figure 3).

Figure 3: EUR/USD (January ‘19 – March ‘19)

, We think that a confirmation from the Fed at next Wednesday’s meeting that its rate hike cycle is effectively at an end, accompanied with similarly dovish comments from Jerome Powell, could trigger an extended reversal in the recent downward move in the EUR/USD rate. This, we believe, could send EUR/USD back towards our 1.15 end of quarter, and indeed end of year, forecast in the coming few weeks.

The very low expectations for additional hikes does, however, mean that any downward move in the US Dollar off the back of any Fed dovishness is unlikely to be knee-jerk and could be relatively gradual and of a potentially limited extent.

SHARE