Nothing matters more in the financial markets right now than the coronavirus, which has continued to pull equity and FX markets one way and then the next.

Should it become clear in the next few weeks that the virus is having a bigger-than-expected negative impact on the Chinese economy then we may see risk assets back under pressure again. But for now, the market is in a much more upbeat mood and central bankers around the world will not be jumping to ease policy just yet.

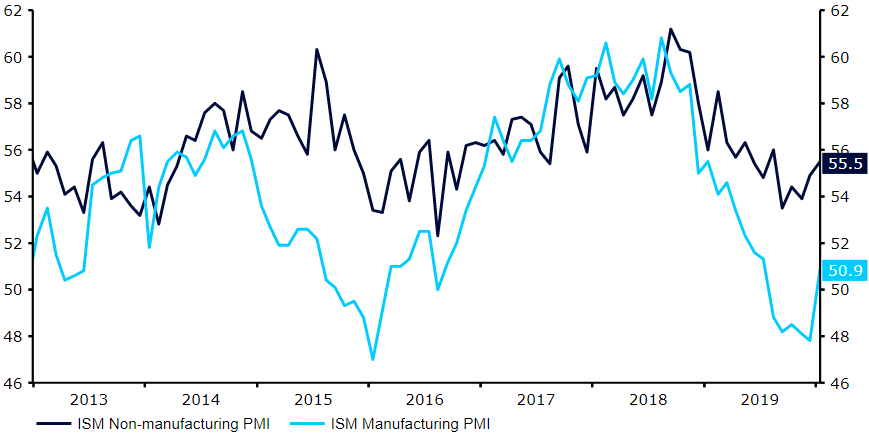

US non-manufacturing activity beats expectations

The US dollar has benefitted from some fairly solid economic data in the past couple of days.

Yesterday’s ADP employment change number was impressive, which would ordinarily bode well for this Friday’s more critical nonfarm payrolls figure, although the link between the two has proved unreliable in the past few months. Job creation in the US public sector jumped to 291,000 in January, much greater than the 156k consensus. We also had an impressive ISM non-manufacturing PMI number, which rose to a comfortably expansionary 55.5. The strength of the data out of the US of late gives further weight to our argument that the Federal Reserve will unlikely even consider cutting interest rates this year.

Figure 1: US ISM Non-manufacturing PMI (2013 – 2020)

Next up for the greenback will, as mentioned, be Friday payrolls report at 13:30 GMT (14:30 CET).

ECB’s Lagarde warns of coronavirus threat

The strong PMI data that we saw out of the Euro Area yesterday morning was offset by some fairly dour retail sales numbers. Sales contracted more than expected in December, falling by 1.6% month-on-month.

To make matters worse for the euro, ECB President Christine Lagarde struck a dovish tone during her speech yesterday. Lagarde stated that Euro Area growth had shown signs of stabilisation, although she did warn over the impact of the coronavirus, stating that it was a ‘renewed source of concern’. She also added that the bank was running out of room to protect the economy from global downside risks.

Wednesday’s soft retail sales data, combined with Lagarde’s comments, was enough to send EUR/USD back to around the 1.10 – just above its lowest level since the beginning of December.

Pound falls on EU negotiation headlines

Sterling, meanwhile, had another volatile ride of it during London trading yesterday. The currency jumped by around 30 pips versus the dollar following the release of the revised January services PMI, which came in at a much better-than-expected 53.9. It did, however, shed the entirety of these gains during the course of trading on the news that the European Union was planning on imposing tougher restrictions on the City of London after the UK’s Brexit transition period.

With no economic data of note out of the UK during the rest of the week, attention among traders will remain on news headlines regarding the EU negotiations.