Commodity currencies rally in volatile markets

( 5 min )

- Go back to blog home

- Latest

10 October 2022

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Volatility has returned to financial markets with a vengeance in the post COVID inflationary world.

We will get some absolutely crucial inflation reports in the US this week. The main CPI report on Thursday is expected to show a pullback in the headline index, but an increase in the core one. However, consensus estimates of inflation have proven unusually inaccurate this year and a surprise in either direction will probably have an outsized impact on currency trading. Producer price inflation and inflation expectations the following date should also be key. For now, it is all about US inflation and the extent and speed of Fed hikes needed to tame it.

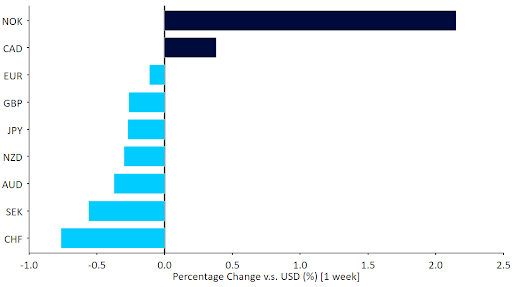

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Source: Refinitiv Datastream Date: 10/10/2022

GBP

The main support to the pound continues to be market hopes that Truss’s planned fiscal deficits will be dialled back. Even the mostly symbolic decision to keep the top tax rate unchanged had a tonic effect on sterling, but the absence of further walkbacks later in the week meant the pound reverted to trading tightly with the euro versus the dollar. The main economic news was a sizable upward revision in the PMIs of business activity, though to a level still consistent with a (shallow) contraction in activity.

Figure 2: UK PMIs (2019 – 2022)

Source: Refinitiv Date: 10/10/2022

This week the somewhat lagging labour market report will be overshadowed by a string of speeches from MPC members, which will be closely watched to gauge the Bank of England’s intended reaction to the recent turmoil in UK financial markets.

EUR

European leading and coincident indicators continue to be consistent with either stagnation or a shallow contraction, but we note that there has been a veritable avalanche of new state spending packages to support households and business throughout the energy crisis. While the long term impact on inflation will not make the ECB happy, iit seems to us that some of the more dire forecasts out there fail to incorporate this fiscal generosity.

For now, the euro continues to trade in line with risk assets focused almost exclusively on Fed hawkishness, and with little news of note out of the Eurozone this week, we expect this pattern will hold up.

USD

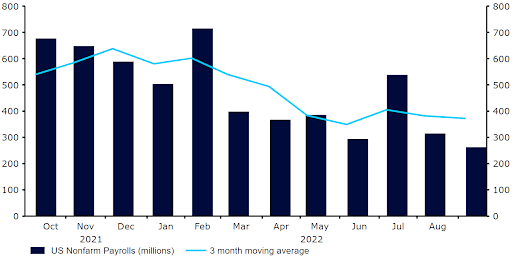

The question of whether the next Federal Reserve interest rate hike would be 50 or 75 basis points was definitively settled by the September nonfarm payrolls data. The labour report showed healthy job creation, record low unemployment, and no signs of easing in spite of the significant tightening of monetary policy so far this year. There was some sign of a deterioration in secondary reports like job openings and weekly jobless claims, but nowhere near enough to stay the Fed’s hand.

This week’s CPI report is expected to show a slight drop in headline inflation on the back of a pull back in energy prices. However, the key will be the core index, where stickier inflation components like shelter are now showing increases in the high single digits and are expected to keep this key index well above 6%.

Figure 3: US Nonfarm Payrolls (2021 – 2022)

Source: Refinitiv Datastream Date: 10/10/2022

CHF

The Swiss franc traded modestly higher against the euro last week as a record plunge in SNB total sight deposits suggested that policymakers remain dedicated to keeping inflation in check by tightening monetary conditions. SNB total sight deposits, generally used as a proxy for FX intervention, have fallen sharply since mid-September, declining to a two-and-a-half year low 639 billion CHF last week, having dropped at a record pace in the week to 4th October (around 77.5 billion CHF). While this would ordinarily indicate massive FX intervention, and a much stronger CHF, most of this decline appears to be due to liquidity absorbing operations and repos designed to guide market interest rates towards the SNB’s policy rate.

We are in the middle of a relatively quiet period of macroeconomic news out of Switzerland, with no major data releases on the docket for this week. A speech by SNB chairman Jordan on Tuesday will, however, be closely watched by market participants.

AUD

The smaller-than-expected interest rate hike from the Reserve Bank of Australia hurt the AUD/USD pair last week, pushing it to around the 0.63 level, its lowest level since April 2020. Investors had expected the RBA to raise rates by 50 basis points at its meeting last week. However, as we had anticipated, the central bank only delivered a 25 basis point hike, which was a disappointment for markets.

In justifying its decision, Governor Philip Lowe said that the cash rate had been ‘increased substantially in a short period of time’, with policymakers seemingly taking a more balanced approach between supporting inflation and controlling the growth outlook. Lowe added that the board expects to continue raising rates at upcoming meetings, but outsized hikes now appear behind us. We think that additional 25 basis point rate hikes are very likely at the November and December meetings, but with other major central banks still in aggressive tightening mode, this could present a downside risk to AUD. With no domestic data out this week, we think that risk sentiment will be the main driver of the dollar.

CAD

The Canadian dollar ended last week as one of the best-performers in the G10, in line with commodity-related currencies that were buoyed by the jump in oil prices. Friday’s stronger-than-expected September employment report also supported CAD at the end of the week. The unemployment rate decreased more than expected to 5.2% in September, signalling that the Canadian labour market remains tight. In addition, the economy added 21,100 jobs last month, slightly above the 20,000 consensus and the first increase in net employment since May.

The strong employment report has raised expectations for rate hikes by the Bank of Canada, with markets now fully pricing in another 50 basis point hike in October, up from the 40 basis points priced in before the data. With no major releases expected from Canada this week, CAD will likely trade off commodity price movements and news elsewhere.

CNY

A week long national holiday in China meant that trading in the onshore yuan was closed last week. In the offshore market (CNH), the currency edged lower, although this was mostly in line with the moves witnessed in the US dollar. As trading opened this morning, the onshore yuan was slightly weaker, perhaps partly in response to some soft business activity data released over the weekend. The Caixin services PMI fell back into contractionary territory in August (49.3 from 55.0), as fresh outbreaks of the COVID-19 virus led to a first drop in new orders in four months. This is another worrying sign of the economic ramifications of the country’s controversial zero-covid approach, which looks likely to continuing weighing on activity as China enters into its winter period.

A dump of consumer and producer inflation figures on Friday will be the main data releases in China this week. Markets are bracing for a modest uptick in headline CPI inflation, which could break to its highest level since the start of the pandemic.

Economic Calendar (10/10/2022 – 14/10/2022)

To stay up to date with our publications, please choose one of the below:

📩 Click here to receive the latest market updates

👉 Our LinkedIn page for the latest news

✍️ Our Blog page for other FX market reports

🔊 Stay up to date with our podcast FXTalk

SHARE