ECB June Meeting Reaction: ECB raises growth, inflation projections

( 2 min )

- Go back to blog home

- Latest

11 June 2021

Head of Market Strategy at Ebury Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

Yesterday’s ECB announcement delivered an unsurprisingly non-committal message from President Lagarde, although the meeting itself was far from a non-event.

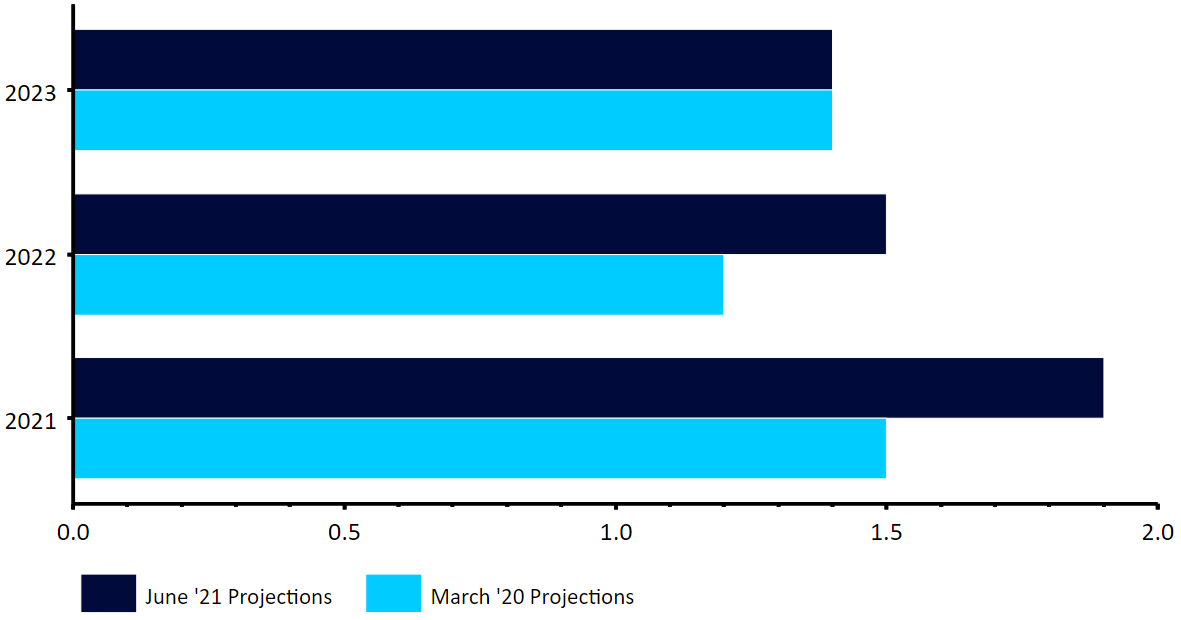

Figure 1: ECB Inflation Projections [June 2021]

Source: Refinitiv Datastream Date: 10/06/2021

Lagarde did, however, seem relatively upbeat about the risk of a spillover in US inflation, which we believe is perhaps a slight underestimation on the ECB’s part. This is particularly the case given the scorchingly hot inflation numbers out across the Atlantic on Thursday afternoon, which showed that US headline inflation jumped by 5% in the year to May.

Despite its upbeat assessment on the outlook, the ECB remained committed to its accelerated pace of asset purchases announced earlier in the year. Investors were also left none the wiser as to whether the bank believes that a tapering in asset purchases will soon be required, and there was no word on whether the PEPP may need to be extended beyond March 2022. We think that decisions on both are being punted to the September meeting, when the ECB will release its next set of macroeconomic projections. At this stage, the ECB should have a much clearer idea as to the state of the health crisis and, more specifically, its impact on Euro Area inflation. Given our expectations that inflation will continue to surprise to the upside, we expect the September meeting to be key. The hawks in the Council will not remain quiescent for long.

As far as the FX reaction is concerned, we’ve not seen too much volatility in the euro on the back of today’s announcement. We think that this is in light of the fact that there were no major surprises from the ECB today – the upgrade to the growth and inflation forecasts were largely expected and there very few in the market bracing for any immediate news on a possible tapering of asset purchases.

SHARE