Euro hits July lows amid fears of fresh virus restrictions

( 5 min. )

- Go back to blog home

- Latest

24 September 2020

Matthew Ryan is Ebury’s Global Head of Market Strategy, based in London, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.

The euro was on the defensive once again on Wednesday, falling to its weakest position since July amid concerns over the rising number of COVID-19 cases in Europe.

Spain and France appear to have emerged as the two main hotspots of the second wave, with both registering record high daily case numbers in the past few days. While much more comprehensive levels of testing means that the situation is still nowhere near as bad as it was during the initial peak, the fear is that it may merely be a matter of time before it is. Fresh containment measures are clearly on the way – France has already announced restrictions on gatherings and early closing times in some of the worst affected areas.

As of yet, none of the major nations in the Euro Area appear willing to consider the reintroduction of full national lockdowns, which really would curtail the economic recovery and weigh heavily on the common currency. Even the threat of more restrictions is already beginning to be reflected in weaker sentiment and soft activity data. Yesterday’s PMI numbers almost all undershot consensus, as did this morning’s business confidence indices from IFO.

Sterling edges higher ahead of Chancellor Sunak announcement

Despite a rough 25% jump in new daily virus numbers yesterday alone, and the tightening of restrictions from the UK government earlier in the week, sterling actually ended London trading higher on Wednesday.

We think that the resilience shown in the pound on Wednesday can be attributed to optimsm surrounding an extension to the government’s job retention measures. The UK’s furlough scheme is set to expire at the end of October. While this is not expected to be extended in its current form, politicians have been preparing alternate programmes that may involve the government simply topping up salaries, similar to schemes introduced in France and Germany. Whether these measures will have any meaningful impact on protecting jobs remains to be seen, but investors view on their effectiveness may determine whether the pound is able to hold onto its gains during the rest of the week.

Chancellor Rishi Sunak is expected to announce the aforementioned emergency measures at 11:30 UK time today. Aside from that, investors will have one eye on a speech from Bank of England governor Bailey later on this afternoon.

Dollar rally continues versus almost all major peers

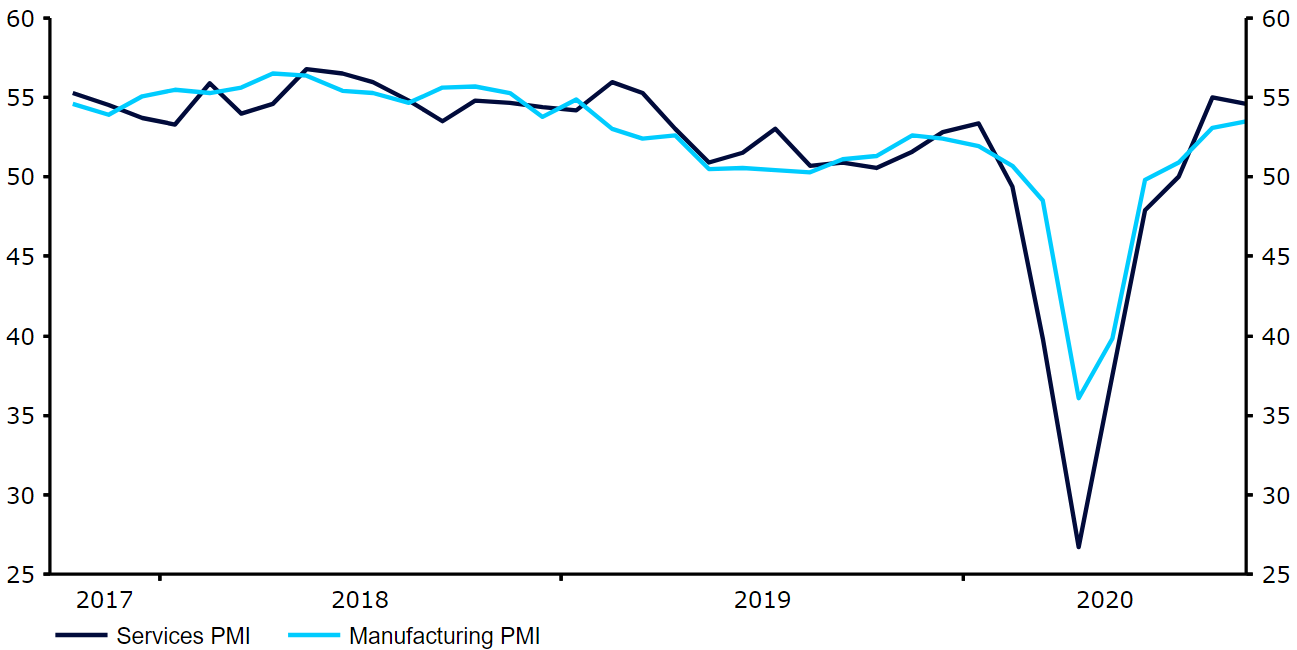

With investors choosing to steer clear of high risk assets this week, the US dollar continues to be king. The greenback appreciated against every other G10 currency on Wednesday, with the exception of sterling. Macroeconomic data out of the US yesterday was largely as expected, with the services PMI from Markit coming in at a pretty healthy 54.6 (Figure 1), just below the 54.7 expected. Weekly jobless claims out this afternoon remains closely watched by investors, while Friday’s durable goods order data will also likely receive some attention this week.

Figure 1: US Services PMI (2017 – 2020)

Source: Refinitiv Datastream Date: 24/09/2020

The main draw for currency traders will, however, be central bank speakers, with FOMC chair Powell to continue his semi-annual testimony to Congress today. His comments yesterday didn’t add too much new information, although a handful of other Fed members voiced their contrasting views on the US economy. Most noteworthy was probably that of Fed member Rosengren, who voiced fears over a second wave of virus infection, while noting that the US would be lucky to see inflation exceed 2% in the next three years. Despite these dovish remarks, the dollar continues to remain well bid in light of the general ‘risk off’ mode we are witnessing in financial markets.

SHARE