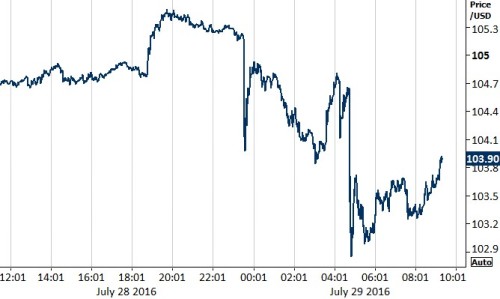

The Japanese Yen soared this morning after the Bank of Japan (BoJ) stunned financial markets by falling well short of expectations at their much hyped monetary policy meeting.

This sent the Yen almost 2% higher against the US Dollar overnight to its strongest position in over two weeks (Figure 1).

Figure 1: USD/JPY (28/07/16 – 29/07/16)

On Thursday Sterling fell during the London session, with the announcement that Lloyds Bank plans to axe 3,000 jobs in the UK amplifying concerns that the domestic economic outlook could deteriorate in the coming months following the Brexit vote.

Attention among traders in the UK now turns to next Thursday’s Bank of England monetary policy meeting. The UK central bank is heavily expected to announce its first interest rate cut since the depths of the financial crisis in 2009.

Friday bodes to be a particularly busy day in the currency markets. The preliminary second quarter growth figures for the US at 13:30 UK time are expected to show a noticeable improvement on the first three months of the year.

Of key importance to the Euro could also be this evening’s stress test results from the European Banking Authority, which will announce its assessment of the 51 largest Euro-area banks at 21:00 UK time. We will pay particular attention to the need for capital injection into the increasingly fragile Italian banking system, the result of which could raise serious concerns about the Eurozone’s financial stability.

Major currencies in detail:

GBP

The Pound declined 0.4% versus the US Dollar yesterday, with investors growing increasingly concerned that the Bank of England will lower its benchmark interest rate next week.

Financial markets are now placing practically 100% implied probability of a rate cut on Thursday. Former BoE policymaker David Blanchflower yesterday added to the growing number voices warning that rates offered by UK banks could even turn negative in the coming months.

Consumer confidence also plunged this morning, with the index from Gfk suffering its largest decline since 1990.

Mortgage approvals and net lending figures are unlikely to rock the boat this morning. We instead look ahead to events next week, primarily the BoE meeting. Next week’s revised PMIs will also be under the microscope.

EUR

The Euro rose a modest 0.1% on Thursday on a raft of positive economic data in the Eurozone.

Unemployment and inflation figures for Germany both impressed in July. The jobless rate fell again in real terms by 7,000, while headline consumer price growth rose unexpectedly to 0.4% in the year to July from 0.3%.

Consumer confidence data in the Eurozone also brushed aside concerns stemming from last month’s Brexit vote. The European Commission’s consumer confidence index was unchanged this month at -7.9, while the economic sentiment index actually increased to 104.6 from 104.4.

Second quarter GDP growth in the Eurozone this morning is expected to slow. The latest inflation and unemployment figures are both also worth noting.

USD

Dimming expectations for a September interest rate hike by the Federal Reserve sent the US Dollar lower across the board during London trading. The Dollar was dealt a further blow overnight following the BoJ decision, with the USD index declining by 0.25%.

An underwhelming set of economic data points also weighed on sentiment towards the greenback yesterday. Initial claims for jobless benefits increased more than expected to 266,000. The trade balance for goods also fell further into negative territory, with the deficit growing to $63.3 billion.

Economic growth data will be the main focal point in the US today. The economy is forecast to have grown by 2.6% annualised and by 1.8% in the quarter, which would mark a significant improvement since the beginning of the year.

Receive these market updates via email