The Pound shot around two percent higher against the US Dollar on Wednesday, sent sharply higher after the House of Commons narrowly voted in favour of rejecting a ‘no deal’ Brexit.

Volatility in Sterling has been sky-high so far this week, with the Pound continuing to exhibit traits of an emerging market currency in the past few days. Today will be no exception, with MPs now set to vote on whether to extend Article 50 and delay Brexit this evening. We think that an extension is inevitable at this point.

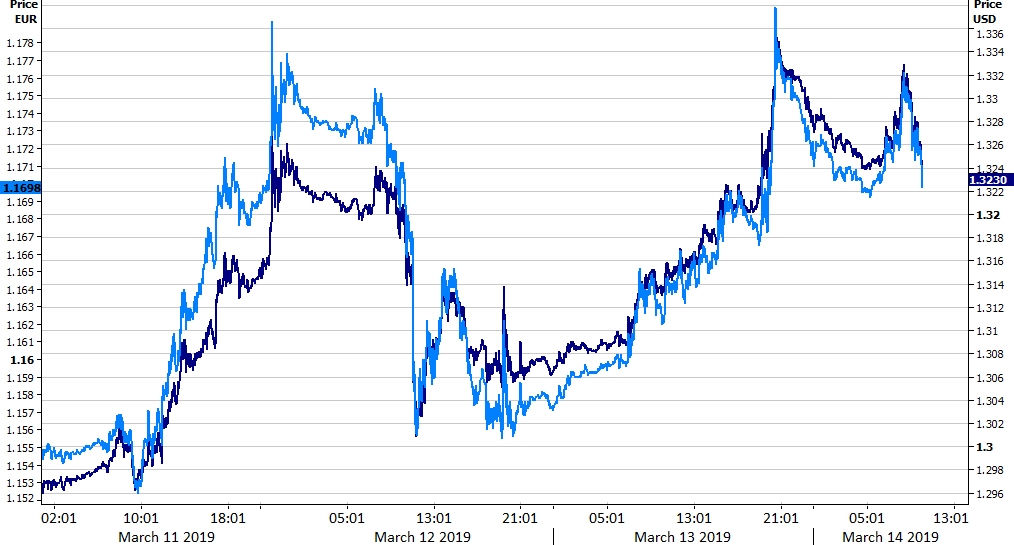

Figure 1: GBP/USD (11/03 – 14/03)

The key to the reaction in the FX markets will be the length of the extension. May is keen for as short a delay as possible, and a two-month extension is possible. This we think, however, would be a disappointment to the market and is actually fairly unlikely given the little time it gives for additional renegotiation. While the EC appears open to a two-year delay, we think the actuality will lie somewhere in between. Confirmation of a delay in excess of two months would be good news for GBP and could cause it to test to 1.35 level against the US Dollar.

It is worth noting that yesterday’s vote to reject a ‘no deal’ is not legally binding, and should MPs surprise the market and reject an A50 delay, leaving without a deal on 29th March remains the default option. Sterling is far from out of the woods yet and wild and unpredictable swings in the currency remain highly likely during the rest of the week.

Brexit relief drags common currency higher

The Euro was a beneficiary of the positive Brexit news, rallying back above the 1.13 mark yesterday to its strongest position in over a week versus the USD. It is worth reiterating that a ‘no deal’ Brexit would also be bad news for the Eurozone, particularly considering the significant portion of EU demand made up by the UK.

Macroeconomic news out on Wednesday was also broadly supportive of the EUR/USD rate. EZ industrial production numbers beat expectations, with output in the sector expanding by a solid 1.4% MoM in January. Across the pond, US producer price data was soft, while durable goods orders where fairly mixed. As we have mentioned in our FOMC preview report, we think that recent soft economic data out of the world’s largest economy could encourage policymakers in the US to signal its interest rate hike cycle is effectively over at its next meeting on Wednesday.

In the interim, we now await tomorrow’s Eurozone inflation numbers. That being said, Brexit continues to dominate and will be the biggest single driver for EUR/USD for the rest of the week.