Thursday’s announcement from the ECB indicated a significant adjustment to asset purchases, as expected. More surprising were hawkish signals from the central bank that pushed the EUR/USD to the strongest level in about two weeks.

The December meeting brought some important revisions to the ECB macroeconomic projections. The changes to growth forecasts were overall rather modest, with the ECB forecasting slightly stronger growth in 2021 (5.1% vs 5.0%) and stronger growth in 2023 (2.9% vs 2.1%), but slower growth in 2022 (4.2% vs 4.6%). All in all, the Eurozone economy is expected to grow by approximately 0.5% more at the end of this horizon. Growth in 2024, however, is set to slow quite considerably, to 1.6%.

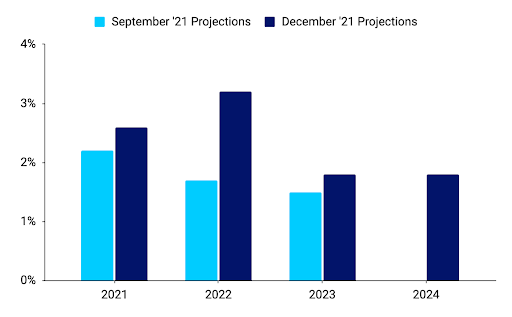

Inflation projections were much more important as they were revised sharply higher, particularly for 2022. An upward revision for that year was expected, but 1.5 percentage points increase from one quarterly projection to another is something unheard of. The ECB now sees HICP inflation of 2.6% in 2021, 3.2% in 2022 and 1.8% in 2023 compared to previous forecasts of 2.2%, 1.7% and 1.5% respectively. In 2024 ECB expects inflation at 1.8% (Figure 1).

Figure 1: ECB HICP Inflation Projections [December]

We view Lagarde’s press conference as mixed-to-hawkish. She mentioned continued recovery of the Eurozone economy and improving labour market, but insisted that ‘monetary accommodation is still needed’. She also touched on the worsening of the pandemic, Omicron variant, bottlenecks and energy prices, but the risks to the economic outlook were still described as ‘broadly balanced’. One of the more hawkish elements of her speech was the assessment that ‘if price pressures feed through into higher than anticipated wage rises or the economy returns more quickly to full capacity, inflation could turn out to be higher’. This could indicate that even though inflation projections have overall been revised up quite substantially, the risks in regard to price growth could be skewed to the upside.

Both the statement and Lagarde mentioned ‘flexibility’, stressing the importance of flexible approach particularly in the face of stress. This could both be seen as a justification for confirming that principal payments from maturing securities under PEPP can be reinvested into Greek bonds, as well as a suggestion that the ECB is not on the autopilot, and that its commitment to not raising rates in 2022 could be revised.

There were also signs of dissent. Although Lagarde said that an overall package of new measures was supported by a ‘very large majority’ it means that some policymakers were not fully happy with it. Not long after the press conference, Reuters published a story mentioning that according to its sources ECB hawks disagreed with parts of the package, not favouring extending PEPP reinvestment to 2024. Moreover, they were also said to stress upside risks to the inflation forecast.

The initial reaction of the euro to the news from the ECB has been positive, with the common currency rising by approximately 0.4% against the US dollar, to the strongest level in about two weeks during Lagarde’s press conference. We attribute it in large part to the low expectations of the FX market going into the meeting. The EUR/USD paired some gains later, but continues to trade above the 1.13 level (Figure 2).

Figure 2: EUR/USD (16/12/2021 – 17/12/2021)

We were quite surprised by the scale of the revision to the inflation forecasts and by the unambiguous language with regards to asset purchases beyond mid-2022. An announcement of scaling back purchases was widely expected, but a plan to cut down buying further in the second half of 2022 and to just €20 billion from October was somewhat on the hawkish side of market expectations. Coupled with a mention of potentially higher inflation it reinforces our view that the ECB will not wait beyond 2023 to start raising rates.