The enormous volatility in financial markets continues, but at least now it comes in the form of two-way moves, rather than the relentless falls of the previous week.

This week, markets will be driven by three main factors. First, the evolution of the coronavirus infection in the different countries, particularly the US, where the infection is gathering speed. Second, the extent of the damage apparent in the leading economic indicators. Third, the announcement of economic support measures for individuals and businesses from the various affected US states. All in all, we see scope for a continuation of the euro rally, as US news takes a turn for the worse while early signs emerge that the epidemic in Europe is no longer growing exponentially.

GBP

Sterling was the best-performing major currency last week. Somewhat surprisingly, it is now up against the US dollar over the past two weeks. This is partly the result of the general volatility and near-dislocated markets, but also a warm market reception to the economic support programmes for SMEs (from Johnson’s government) and large companies (Bank of England). The Bank of England didn’t announce any fresh stimulus measures at its meeting on Thursday, although it did suggest that it stands ready to act further, should conditions in the market or UK economy warrant.

We’ll get little news that will reflect the impact of the crisis this week, but clearly the drop to record lows of two weeks ago has cleared out most speculative longs and we expect sterling to be relatively resilient in the next couple of weeks.

EUR

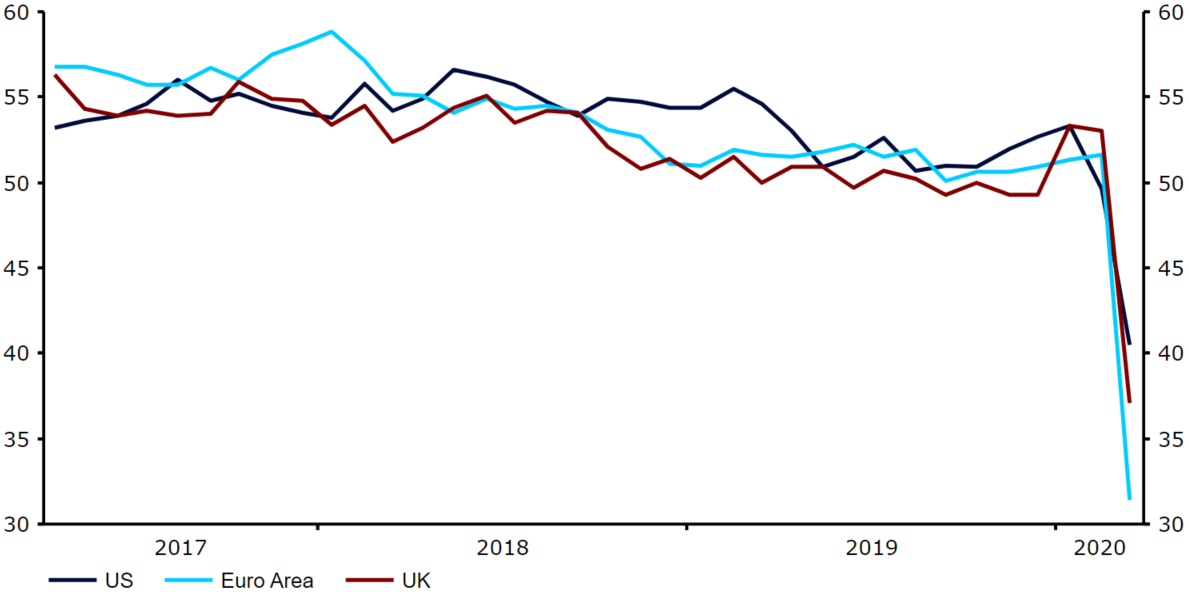

The sharp rebound of the common currency last week owed little to any news from the Eurozone and was mostly a reflection of the general rebound in risk aversion. The economic news we did have out of the Euro Area was unsurprisingly disastrous, with the March PMI numbers falling to record low levels (Figure 1). While this was also the case in both the UK and the US, the Eurozone economy has, so far, appeared the most exposed of the three to the crisis.

Figure 1: US, Euro Area & UK PMIs (2016 – 2020)

Source: Refinitiv Datastream Date: 30/03/2020

This week we will see an important data point that is receiving little attention. The inflation numbers for March will already reflect the impact of the crisis. It will be interesting to see whether the collapse in demand or the contraction of supply brought about by the lockdowns have the largest impact in prices. We will also remain focused on the details of support programs for individuals and SMEs, as these will be key to the shape of any future rebound from the upcoming recession.

USD

The coronavirus crisis has now hit the US with full force. The US is now presenting the largest amount of new cases every day, in spite of still limited testing. The chaotic response by federal and some state authorities has certainly not helped. In addition, the crisis has now spread to the economy, as the lockdowns sent weekly claims for unemployment benefits to its highest ever level by far, well over three million, up from just a couple of hundred thousand two weeks ago.

We are likely to receive another eye-popping number when the number of jobs lost by the economy in March are published in the monthly payroll report this coming Friday. There is a good chance that the relative worsening of the crisis in the US, compared to the tentative stabilisation we are seeing on the new contagion numbers in Europe, will prove a headwind for the US dollar next week.