Summary:

- Euro Area PMIs beat expectations, easing concerns over a possible recession in the bloc.

- Sterling underperforms as data shows UK services sector posts weakest activity in two years.

- USD remains pinned around its lowest level in nine months against peers amid Fed expectations, mixed macroeconomic news. US Q4 growth data (Thursday) eyed by investors.

Arguably one of the most noteworthy moves in currencies in the past week or so has been the rally in the euro, which has risen to fresh multi-month highs on the broadly weaker US dollar.

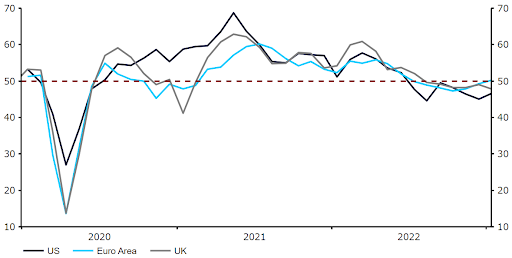

Since the euro last traded below parity on the dollar in November, concerns surrounding a possible recession in the Euro Area have eased significantly, particularly in light of an improvement in the European energy situation. These concerns faded further on Tuesday following a strong set of business activity prints. The monthly composite PMI, which represents a weighted metric of activity in the services and manufacturing sectors, rose to 50.2 in January, comfortably above the 49.8 expected by economists. For the first time in seven months, this key indicator, which we view as the most timely and important gauge of economic activity in the bloc, has risen back above the level of 50 and into expansionary territory.

The common currency was actually little moved off the back of the news, ending London trading just shy of the $1.09 level. While this is a bit of a surprise, we think this is perhaps a reflection that investors view the data as having limited impact on next week’s European Central Bank decision. Attention among ECB members remains firmly fixated on inflation, particularly the core index, which thus far has shown no signs of abating. Communications from ECB members in the past few days have been undeniably hawkish. Members Knot and Kazimir have both thrown their support behind at least two additional 25bps hikes in February and March, while President Lagarde reaffirmed that the bank would need to ‘stay the course’ until policy had move into suitably restrictive territory.

Unfortunately for sterling bulls, macroeconomic news out of the UK yesterday was far less impressive. The UK’s composite PMI slipped further into contractionary territory in January, easing to 47.8 from 49.0, well below consensus. While manufacturing activity remained soft, this was driven largely by a downturn in Britain’s dominant services industry. The pound traded sharply lower on the news, down around 1% on the dollar at one stage, before recovering some of its losses. While optimism for the year ahead among business owners rose to its highest level since May, the data remains consistent with a downturn, and recession fears are likely to linger for a little while yet, which could keep sterling rallies in check.

Meanwhile, mixed data and growing expectations that the Federal Reserve may hint at an end to its tightening cycle at its FOMC meeting next week are keeping the US dollar under pressure, and pinned around its lowest level in nine months. Completing the set on Tuesday were the US PMI prints for January that, while better than expected, remained well below the level of 50 – the composite index came in at just 46.6 this month. Thursday’s Q4 GDP data will likely be a big test for the greenback. Solid growth in the region of 3% annualised is expected by economists, which would be roughly in line with the Q2 number. Any downside surprise here could cement the aforementioned Fed expectations and further weigh on the dollar towards the end of the week.

Figure 1: G3 Composite PMIs (2020 – 2023)