9 December 2020

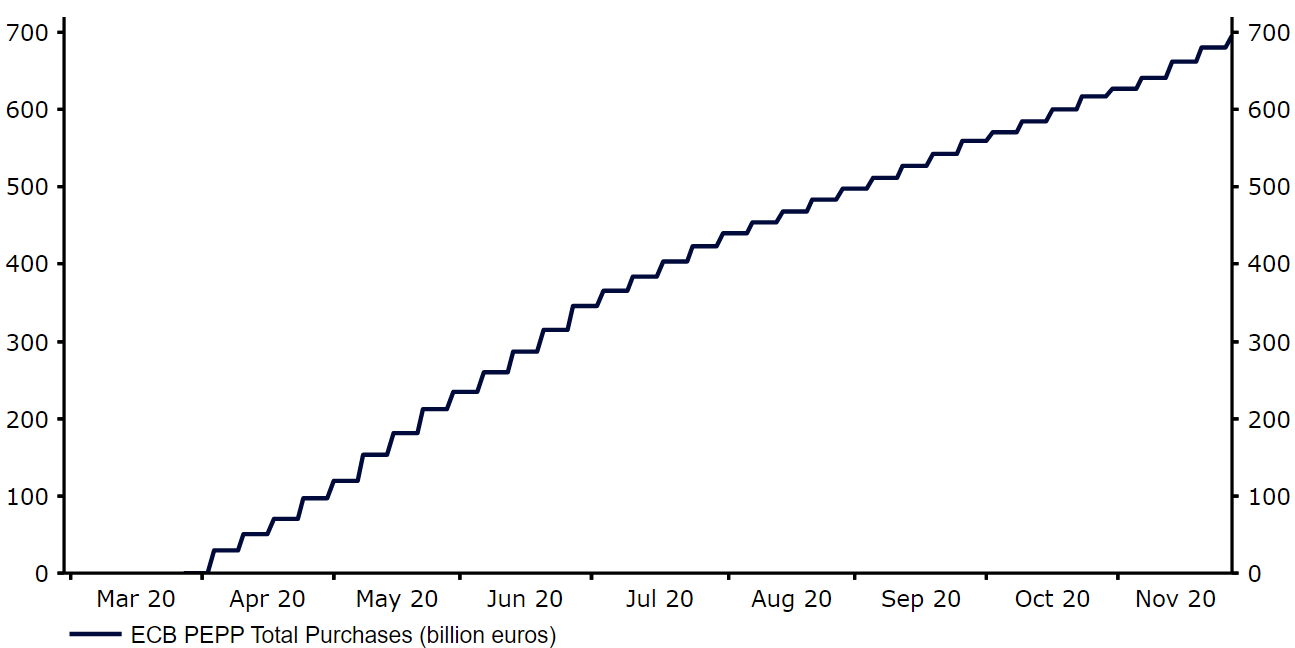

The second wave of the COVID-19 pandemic presents a significant downside risk to the Euro Area economy. New cases of the virus began increasing sharply in the bloc in early-October, leading to the re-introduction of a number of containment measures from earlier in the year. France and Germany both imposed national lockdowns, with many other countries in the bloc enforcing a range of measures such as tiered systems, nighttime curfews and the early closure of hospitality venues. The imposition of these measures has raised concerns over a fresh slump in Eurozone economic activity and caused investors to double down on bets on additional policy easing from the European Central Bank at its 10th December meeting.Throughout the crisis the ECB has had little room to cut its already negative interest rates, instead pledging to inject stimulus into the economy via asset purchase programmes. The bank’s new scheme, the Pandemic Emergency Purchase Programme (PEPP), was expanded in June, with the ECB committing to purchasing a total envelope of assets worth €1.35 trillion through at least the end of June 2021. At its last meeting in October, the Governing Council gave a clear indication that another increase in the programme was likely. President Lagarde noted that there had been a ‘clear deterioration’ in the near-term outlook following the announcement of fresh lockdowns, and that the bank would respond promptly to address the situation. Since then, a number of ECB officials have talked up the possibility of action this month, most recently members Shnabel, Kazaks and chief economist Philip Lane. Investors are now expecting a fresh round of stimulus from the ECB on Thursday. We think that the bank will again choose to ramp up its emergency asset purchase programme, possibly by another 500 billion euros, taking the total amount of purchases up to €1.85 trillion. The end date of the programme is also likely to be pushed further and we are pencilling in another six month extension to the PEPP through at least the end of 2021. This would allow purchases to continue at approximately the average rate that they have done during the course of the programme (Figure 1) through to the end of December next year. Figure 1: ECB PEPP Total Purchases [billion euros] (March ‘20 - Dec ‘20)

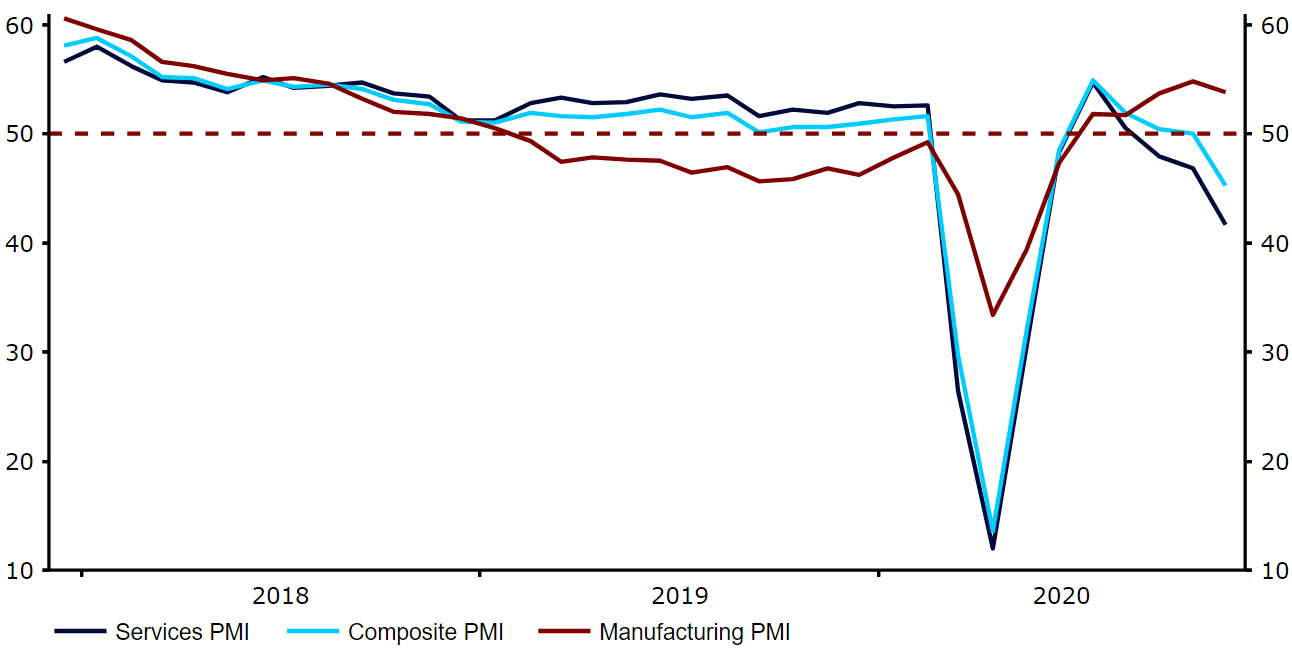

Investors are now expecting a fresh round of stimulus from the ECB on Thursday. We think that the bank will again choose to ramp up its emergency asset purchase programme, possibly by another 500 billion euros, taking the total amount of purchases up to €1.85 trillion. The end date of the programme is also likely to be pushed further and we are pencilling in another six month extension to the PEPP through at least the end of 2021. This would allow purchases to continue at approximately the average rate that they have done during the course of the programme (Figure 1) through to the end of December next year. Figure 1: ECB PEPP Total Purchases [billion euros] (March ‘20 - Dec ‘20)  Source: Refinitiv Datastream Date: 07/12/2020There is also speculation that the ECB will extend its generous targeted longer-term refinancing operations (TLTROs) and expand its tiering facility to Euro Area banks. These would, however, be largely technical changes that, in our view, are unlikely to have any real bearing on the market reaction. Aside from any policy changes, investors will be paying close attention to the bank’s updated economic projections on both growth and inflation. We think that the GDP forecast for 2020 is certain to be revised lower. The Q4 projection from September (+3.1% QoQ) fails to take into account the latest round of virus containment measures and is therefore both outdated and entirely too optimistic. While we’ve not had any major hard indicators of economic activity out that cover this period of tighter restrictions, the business activity composite PMI fell into a deep contractionary 45.3 in November, its lowest level since May (Figure 2). Figure 2: Euro Area PMIs (2017 - 2020)

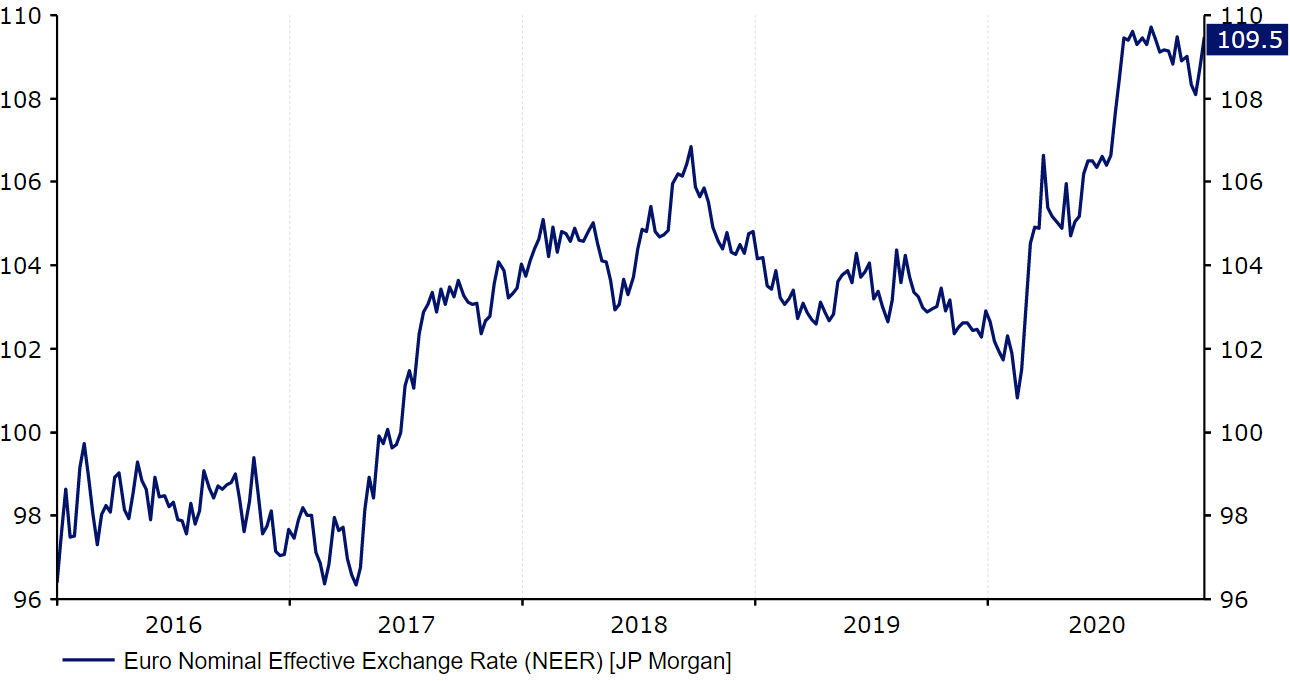

Source: Refinitiv Datastream Date: 07/12/2020There is also speculation that the ECB will extend its generous targeted longer-term refinancing operations (TLTROs) and expand its tiering facility to Euro Area banks. These would, however, be largely technical changes that, in our view, are unlikely to have any real bearing on the market reaction. Aside from any policy changes, investors will be paying close attention to the bank’s updated economic projections on both growth and inflation. We think that the GDP forecast for 2020 is certain to be revised lower. The Q4 projection from September (+3.1% QoQ) fails to take into account the latest round of virus containment measures and is therefore both outdated and entirely too optimistic. While we’ve not had any major hard indicators of economic activity out that cover this period of tighter restrictions, the business activity composite PMI fell into a deep contractionary 45.3 in November, its lowest level since May (Figure 2). Figure 2: Euro Area PMIs (2017 - 2020) Source: Refinitiv Datastream Date: 07/12/2020The ECB may, however, strike an optimistic note towards the outlook for 2021, given that multiple vaccines are now close to being rolled out earlier than had been previously expected. On inflation, we don’t envisage any major forecast changes at this week’s meeting, although their projection for 2021 may be lowered slightly. We will, however, be paying close attention to whether the bank changes its view towards the strength of the euro. There is a possibility that Lagarde could raise concerns over the impact of a strong currency on suppressing both growth and inflation in the coming months. In nominal effective exchange rate terms (NEER), the euro is currently around its strongest position since November 2009 according to JP Morgan (Figure 3).Figure 3: Euro Nominal Effective Exchange Rate [JP Morgan] (2016 - 2020)

Source: Refinitiv Datastream Date: 07/12/2020The ECB may, however, strike an optimistic note towards the outlook for 2021, given that multiple vaccines are now close to being rolled out earlier than had been previously expected. On inflation, we don’t envisage any major forecast changes at this week’s meeting, although their projection for 2021 may be lowered slightly. We will, however, be paying close attention to whether the bank changes its view towards the strength of the euro. There is a possibility that Lagarde could raise concerns over the impact of a strong currency on suppressing both growth and inflation in the coming months. In nominal effective exchange rate terms (NEER), the euro is currently around its strongest position since November 2009 according to JP Morgan (Figure 3).Figure 3: Euro Nominal Effective Exchange Rate [JP Morgan] (2016 - 2020) Source: Refinitiv Datastream Date: 07/12/2020Overall, we expect Lagarde and the ECB’s accompanying communications to show a hint of optimism towards vaccine progress and the outlook for the Euro Area economy in 2021. That being said, we think that the bank will strike a dovish tone towards the near-term outlook on Thursday, stating that additional accommodation is required in order to help the economy through the second wave of virus infection. As noted, we expect a 500 billion euro increase in the PEPP, with the measures to be extended until the end of next year. This, we believe, is already almost entirely priced in by the market, so we wouldn’t expect any real downside in the euro to such an announcement. A smaller increase in the programme of anything less than around 400 billion euros would be a surprise to investors and would likely trigger an immediate move higher in the common currency on Thursday. By contrast, a more aggressive batch of new measures, combined with large downward revisions to GDP and rhetoric from Lagarde that tempers vaccine optimsm and/or raises concerns over a stronger currency would, we believe, weigh on the euro. We think that any comments on the euro’s strength could be the biggest risk to the common currency on Thursday. Given how stretched the euro’s relentless rally has become, there is potential for a meaningful retracement if that turns out to be the case.The ECB’s policy decision will be announced at 12:45 GMT (13:45 CET) this Thursday, with the press conference to follow 45 minutes later.

Source: Refinitiv Datastream Date: 07/12/2020Overall, we expect Lagarde and the ECB’s accompanying communications to show a hint of optimism towards vaccine progress and the outlook for the Euro Area economy in 2021. That being said, we think that the bank will strike a dovish tone towards the near-term outlook on Thursday, stating that additional accommodation is required in order to help the economy through the second wave of virus infection. As noted, we expect a 500 billion euro increase in the PEPP, with the measures to be extended until the end of next year. This, we believe, is already almost entirely priced in by the market, so we wouldn’t expect any real downside in the euro to such an announcement. A smaller increase in the programme of anything less than around 400 billion euros would be a surprise to investors and would likely trigger an immediate move higher in the common currency on Thursday. By contrast, a more aggressive batch of new measures, combined with large downward revisions to GDP and rhetoric from Lagarde that tempers vaccine optimsm and/or raises concerns over a stronger currency would, we believe, weigh on the euro. We think that any comments on the euro’s strength could be the biggest risk to the common currency on Thursday. Given how stretched the euro’s relentless rally has become, there is potential for a meaningful retracement if that turns out to be the case.The ECB’s policy decision will be announced at 12:45 GMT (13:45 CET) this Thursday, with the press conference to follow 45 minutes later.

Investors are now expecting a fresh round of stimulus from the ECB on Thursday. We think that the bank will again choose to ramp up its emergency asset purchase programme, possibly by another 500 billion euros, taking the total amount of purchases up to €1.85 trillion. The end date of the programme is also likely to be pushed further and we are pencilling in another six month extension to the PEPP through at least the end of 2021. This would allow purchases to continue at approximately the average rate that they have done during the course of the programme (Figure 1) through to the end of December next year. Figure 1: ECB PEPP Total Purchases [billion euros] (March ‘20 - Dec ‘20) Source: Refinitiv Datastream Date: 07/12/2020There is also speculation that the ECB will extend its generous targeted longer-term refinancing operations (TLTROs) and expand its tiering facility to Euro Area banks. These would, however, be largely technical changes that, in our view, are unlikely to have any real bearing on the market reaction. Aside from any policy changes, investors will be paying close attention to the bank’s updated economic projections on both growth and inflation. We think that the GDP forecast for 2020 is certain to be revised lower. The Q4 projection from September (+3.1% QoQ) fails to take into account the latest round of virus containment measures and is therefore both outdated and entirely too optimistic. While we’ve not had any major hard indicators of economic activity out that cover this period of tighter restrictions, the business activity composite PMI fell into a deep contractionary 45.3 in November, its lowest level since May (Figure 2). Figure 2: Euro Area PMIs (2017 - 2020)Source: Refinitiv Datastream Date: 07/12/2020The ECB may, however, strike an optimistic note towards the outlook for 2021, given that multiple vaccines are now close to being rolled out earlier than had been previously expected. On inflation, we don’t envisage any major forecast changes at this week’s meeting, although their projection for 2021 may be lowered slightly. We will, however, be paying close attention to whether the bank changes its view towards the strength of the euro. There is a possibility that Lagarde could raise concerns over the impact of a strong currency on suppressing both growth and inflation in the coming months. In nominal effective exchange rate terms (NEER), the euro is currently around its strongest position since November 2009 according to JP Morgan (Figure 3).Figure 3: Euro Nominal Effective Exchange Rate [JP Morgan] (2016 - 2020)Source: Refinitiv Datastream Date: 07/12/2020Overall, we expect Lagarde and the ECB’s accompanying communications to show a hint of optimism towards vaccine progress and the outlook for the Euro Area economy in 2021. That being said, we think that the bank will strike a dovish tone towards the near-term outlook on Thursday, stating that additional accommodation is required in order to help the economy through the second wave of virus infection. As noted, we expect a 500 billion euro increase in the PEPP, with the measures to be extended until the end of next year. This, we believe, is already almost entirely priced in by the market, so we wouldn’t expect any real downside in the euro to such an announcement. A smaller increase in the programme of anything less than around 400 billion euros would be a surprise to investors and would likely trigger an immediate move higher in the common currency on Thursday. By contrast, a more aggressive batch of new measures, combined with large downward revisions to GDP and rhetoric from Lagarde that tempers vaccine optimsm and/or raises concerns over a stronger currency would, we believe, weigh on the euro. We think that any comments on the euro’s strength could be the biggest risk to the common currency on Thursday. Given how stretched the euro’s relentless rally has become, there is potential for a meaningful retracement if that turns out to be the case.The ECB’s policy decision will be announced at 12:45 GMT (13:45 CET) this Thursday, with the press conference to follow 45 minutes later.