29 April 2020

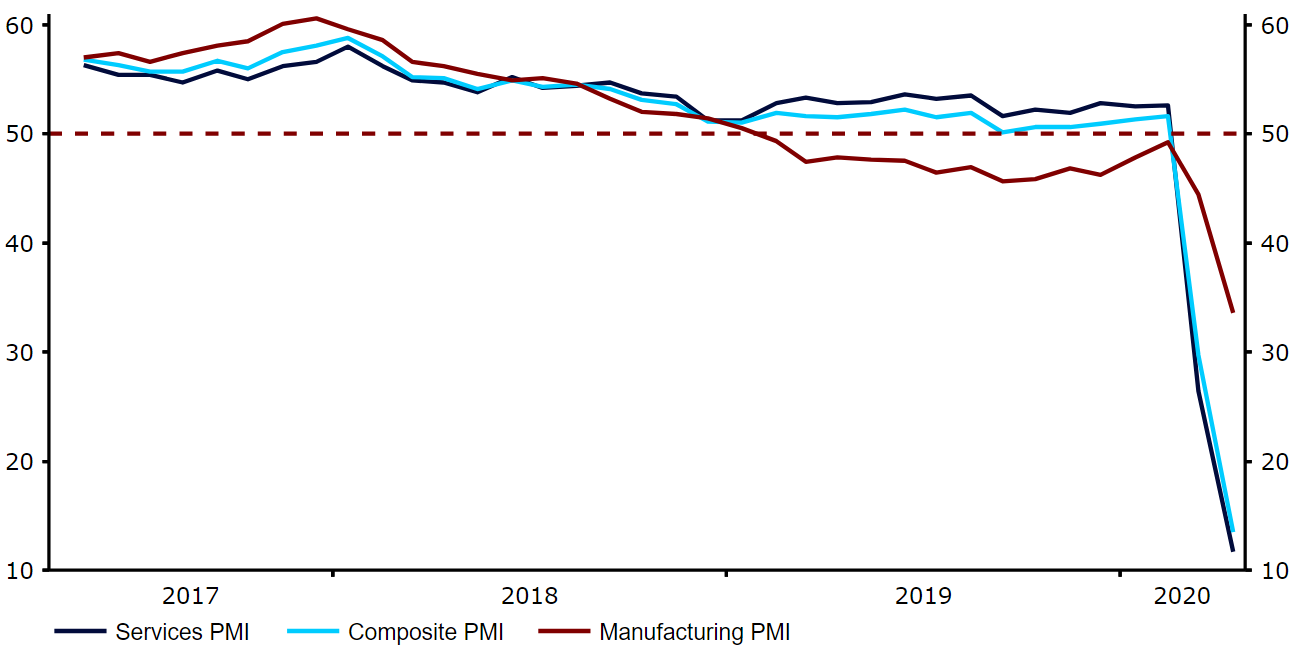

The COVID-19 pandemic is continuing to cause devastation to the global economy and force central banks and governments around the world to unveil massive and unprecedented stimulus measures.The European Central Bank has been no exception, announcing a host of initiatives since the beginning of the crisis aimed at supporting the Euro Area economy. While the ECB currently has little room to cut interest rates, it has unveiled a range of more unorthodox measures, including ramping up its quantitative easing programme by a total of 120 billion euros. It has also introduced its large-scale Pandemic Emergency Purchase Programme (PEPP), which will see the bank buy an overall envelope of 750 billion euros by the end of 2020. Other actions to combat the crisis have included the introduction of more favourable lending terms for commercial banks and temporary collateral easing measures.Under normal circumstances the bank would, at this juncture, stand pat on policy and await the impact of its recent stimulus measures on macroeconomic data. We are, however, in unprecedented times, and the announcement of further easing measures at the ECB’s Governing Council meeting this coming Thursday is now very much a possibility, in our view. At the very least, we expect the ECB to provide forward guidance that would indicate its readiness and willingness to do more if needed at upcoming meetings, particularly regarding an expansion of the PEPP.The latest contagion numbers out of Europe have been encouraging, suggesting that the worst of the virus may now be over. It is clear, however, that the pace of an unwinding in the containment measures will be gradual and their economic impact severe. Since the bank’s previous meeting in March, we have begun to see evidence of this fallout in the latest Euro Area macroeconomic data. The business activity PMIs, in particular, have collapsed, with the composite index dropping to a fresh record low 13.5 in April (Figure 1).Figure 1: Euro Area PMIs (2017 - 2020) Source: Refinitiv Datastream Date: 28/04/2020Employment in both the manufacturing and services sectors has declined rapidly, although there are at least some signs that the bloc’s labour market is holding up better than in the US. We think this is due to the much stronger job retention schemes currently in place in the common bloc than across the Atlantic. Regardless, the pending recession in the bloc this year looks set to be a very severe one, with President Lagarde herself warned earlier this month that the Euro Area economy could contract by as much as 15% this year. We think that the ECB will acknowledge the severity of the downturn by striking a very dovish tone during its accompanying communications.

Source: Refinitiv Datastream Date: 28/04/2020Employment in both the manufacturing and services sectors has declined rapidly, although there are at least some signs that the bloc’s labour market is holding up better than in the US. We think this is due to the much stronger job retention schemes currently in place in the common bloc than across the Atlantic. Regardless, the pending recession in the bloc this year looks set to be a very severe one, with President Lagarde herself warned earlier this month that the Euro Area economy could contract by as much as 15% this year. We think that the ECB will acknowledge the severity of the downturn by striking a very dovish tone during its accompanying communications.

Source: Refinitiv Datastream Date: 28/04/2020Employment in both the manufacturing and services sectors has declined rapidly, although there are at least some signs that the bloc’s labour market is holding up better than in the US. We think this is due to the much stronger job retention schemes currently in place in the common bloc than across the Atlantic. Regardless, the pending recession in the bloc this year looks set to be a very severe one, with President Lagarde herself warned earlier this month that the Euro Area economy could contract by as much as 15% this year. We think that the ECB will acknowledge the severity of the downturn by striking a very dovish tone during its accompanying communications.