15 September 2020

Since the FOMC’s last official meeting in late-July, the Federal Reserve has unveiled one of the most significant changes to its monetary policy strategy in the last few decades. Speaking during the annual Jackson Hole Symposium on 27th August, FOMC chair Jerome Powell announced that the central bank would be taking a more relaxed view towards its inflation target. The bank will now strive to keep price growth around 2% on average over time in order to make up for the recent prolonged period of below target inflation witnessed in the US. This policy tweak allows for greater emphasis to be placed on supporting the US labour market, notably those in low income employment. As we mentioned at the time, the Fed’s willingness to look through short-term increases in inflation raises the bar for future hikes and is a clear signal to the market that ultra-low interest rates are here for the foreseeable future.With such a significant overhaul already unveiled prior to this week’s meeting, we don’t expect any major shifts in policy from the FOMC on Wednesday. We also don’t expect to see any meaningful changes in forward guidance given the acute uncertainty still surrounding the virus and its impact on the US economy. The Fed will likely continue to stress that interest rates will remain at record low levels for the foreseeable future. Currency traders will therefore instead be paying close attention to the Fed’s accompanying rhetoric on the state of the US recovery and the bank’s revised economic projections.We outline below the key aspects of the Fed’s communications to look out for this week: We think that a rather sharp downward revision to the Fed’s unemployment forecasts is also on the way this week. At 8.4%, the US jobless rate has already undershot the Fed’s 9.3% end of year projection from June. Baring another meaningful tightening in shutdown measures, we think that the jobless rate is likely to continue trending lower in the coming months as industries return to more normal levels of capacity.Arguably of greatest interest to currency markets will be the FOMC participants' revised interest rate expectations (the bank’s ‘dot plot’). We think that the median path for 2022 will remain unchanged at the effective lower bound (Figure 2). The bank will also be forecasting rates through 2023 for the first time this week. While we think that a handful of participants will forecast hikes, we think that the adoption of the Fed’s average inflation target will ensure that the medium dot will also remain at the 0-0.25% range for 2023. This would be in line with market pricing, which has pushed the timing of the next hike all the way out to 2024. At any rate, the FOMC’s view on the potential evolution of rates in 2023 will be the most important single data point to merge from the meeting, in our view.Figure 2: FOMC Dot Plot [June 2020]

We think that a rather sharp downward revision to the Fed’s unemployment forecasts is also on the way this week. At 8.4%, the US jobless rate has already undershot the Fed’s 9.3% end of year projection from June. Baring another meaningful tightening in shutdown measures, we think that the jobless rate is likely to continue trending lower in the coming months as industries return to more normal levels of capacity.Arguably of greatest interest to currency markets will be the FOMC participants' revised interest rate expectations (the bank’s ‘dot plot’). We think that the median path for 2022 will remain unchanged at the effective lower bound (Figure 2). The bank will also be forecasting rates through 2023 for the first time this week. While we think that a handful of participants will forecast hikes, we think that the adoption of the Fed’s average inflation target will ensure that the medium dot will also remain at the 0-0.25% range for 2023. This would be in line with market pricing, which has pushed the timing of the next hike all the way out to 2024. At any rate, the FOMC’s view on the potential evolution of rates in 2023 will be the most important single data point to merge from the meeting, in our view.Figure 2: FOMC Dot Plot [June 2020]

Updated macroeconomic projections

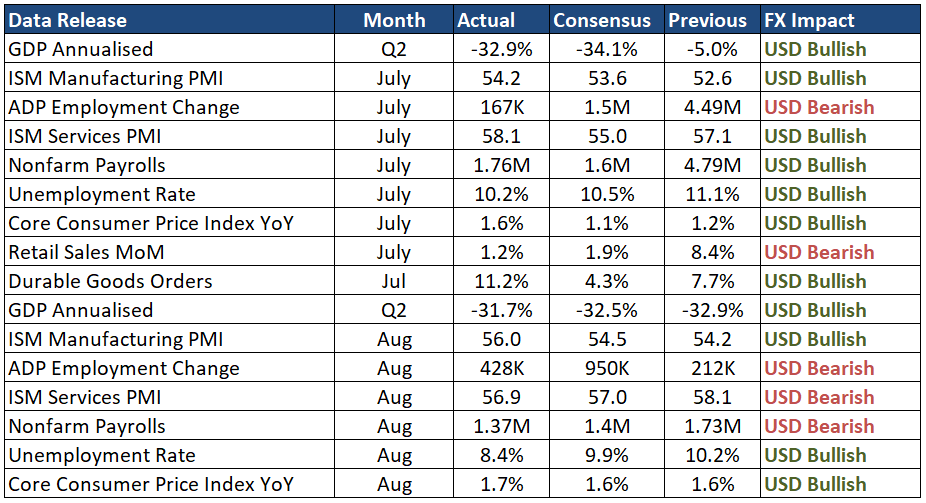

As is customary following every other FOMC meeting, the Fed will be releasing its updated macroeconomic and interest rates projections on Wednesday. Regarding the former, we think that an upward revision to the outlook is likely. At the June meeting, the Fed stated that it expected the US economy to contract by 6.5% this year, with positive growth of 5% to follow in 2021. Since then, the recovery in the global economy has taken place at a generally quicker pace than central bankers had anticipated during the height of the downturn. Notably, the key indicators of business activity, retail sales and employment have all bounced back reasonably strongly following the unwinding of lockdown measures across most US states (Figure 1). We expect the language in the statement to be marginally more upbeat versus July, albeit Chair Powell will acknowledge that their outlook remains highly dependent on the pandemic.Figure 1: Key US Economic Data Releases (since FOMC’s July meeting)We think that a rather sharp downward revision to the Fed’s unemployment forecasts is also on the way this week. At 8.4%, the US jobless rate has already undershot the Fed’s 9.3% end of year projection from June. Baring another meaningful tightening in shutdown measures, we think that the jobless rate is likely to continue trending lower in the coming months as industries return to more normal levels of capacity.Arguably of greatest interest to currency markets will be the FOMC participants' revised interest rate expectations (the bank’s ‘dot plot’). We think that the median path for 2022 will remain unchanged at the effective lower bound (Figure 2). The bank will also be forecasting rates through 2023 for the first time this week. While we think that a handful of participants will forecast hikes, we think that the adoption of the Fed’s average inflation target will ensure that the medium dot will also remain at the 0-0.25% range for 2023. This would be in line with market pricing, which has pushed the timing of the next hike all the way out to 2024. At any rate, the FOMC’s view on the potential evolution of rates in 2023 will be the most important single data point to merge from the meeting, in our view.Figure 2: FOMC Dot Plot [June 2020]