31 January 2023

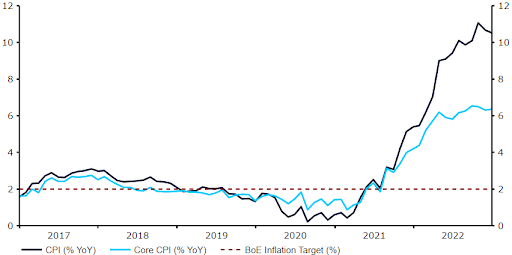

This Thursday’s Bank of England monetary policy announcement is a typically tough one to call, given the recent lack of consensus among committee members.The MPC once again delivered mixed messages in December - a common theme throughout 2022. Rates were raised by another 50bps to 3.5%, the tenth consecutive hike, though the three-way split vote indicated that members were once again divided over the extent of additional tightening required. Two of the nine members, doves Tenreyro and Dhingra, surprisingly voted in favour of no change in rates, arguing that the bank rate was ‘more than sufficient’ to bring inflation back to target. The line from the November statement, which had pushed back against market pricing for UK rates was, however, omitted, in another apparent change of heart from the majority of the committee.  Since the December meeting, we think that macroeconomic news out of the UK has mixed ramifications for monetary policy though, on balance, we are pencilling in another 50bp rate increase this week. The focus among committee members clearly remains on inflation and, as of yet, we are yet to see clear evidence of a downward trend in either the headline or core CPI measures. One could argue that the surprise to the downside in the December UK inflation report has slightly taken the pressure off the MPC this week. In our view, this will not be enough to materially shift the hawks off course. Core inflation has remained particularly sticky, and has printed above 6% in each of the past six months.Figure 1: UK Inflation Rate (2017 - 2022)

Since the December meeting, we think that macroeconomic news out of the UK has mixed ramifications for monetary policy though, on balance, we are pencilling in another 50bp rate increase this week. The focus among committee members clearly remains on inflation and, as of yet, we are yet to see clear evidence of a downward trend in either the headline or core CPI measures. One could argue that the surprise to the downside in the December UK inflation report has slightly taken the pressure off the MPC this week. In our view, this will not be enough to materially shift the hawks off course. Core inflation has remained particularly sticky, and has printed above 6% in each of the past six months.Figure 1: UK Inflation Rate (2017 - 2022) We suspect that the hawks among the committee will argue that this is not compelling enough evidence to begin winding down the hiking cycle, and that more needs to be done to ensure a return to the bank’s 2% inflation target. In our view, the BoE is not yet in the same boat as the Federal Reserve, which both tightened policy more aggressively than the MPC in 2022 (425bp vs. 325bps), and has witnessed clearer signs of a downtrend in domestic inflation. A likely point of contention and discussion among policymakers will perhaps be the recent signs of a deterioration in UK economic activity, most notably signs of weakness in retail sales and the services sector. This could lead to a few more dovish dissents among members, although again we do not believe that this will be enough to tip the balance in favour of a smaller hike, particularly as overall growth is proving rather resilient. Figure 2: UK Key Macroeconomic Data [since 15/12/2022]

We suspect that the hawks among the committee will argue that this is not compelling enough evidence to begin winding down the hiking cycle, and that more needs to be done to ensure a return to the bank’s 2% inflation target. In our view, the BoE is not yet in the same boat as the Federal Reserve, which both tightened policy more aggressively than the MPC in 2022 (425bp vs. 325bps), and has witnessed clearer signs of a downtrend in domestic inflation. A likely point of contention and discussion among policymakers will perhaps be the recent signs of a deterioration in UK economic activity, most notably signs of weakness in retail sales and the services sector. This could lead to a few more dovish dissents among members, although again we do not believe that this will be enough to tip the balance in favour of a smaller hike, particularly as overall growth is proving rather resilient. Figure 2: UK Key Macroeconomic Data [since 15/12/2022]  By contrast to the December meeting, financial markets are not yet fully accounting for a 50bp hike ahead of Thursday’s announcement. Another 50bp move is now around 80% priced in according to swap valuations, which we believe may perhaps be a consequence of interest rate repricing globally and the dovish vote and muddled communications among committee members in December. In the event of a half a percentage point move we do, therefore, see scope for a small rally in the pound, depending on the tone of the bank’s communications. A 25bp hike would be a fairly significant surprise for markets and, in our view, would likely trigger a rather sharp sell-off in the pound, regardless of how this is dressed up in the bank’s accompanying rhetoric.

By contrast to the December meeting, financial markets are not yet fully accounting for a 50bp hike ahead of Thursday’s announcement. Another 50bp move is now around 80% priced in according to swap valuations, which we believe may perhaps be a consequence of interest rate repricing globally and the dovish vote and muddled communications among committee members in December. In the event of a half a percentage point move we do, therefore, see scope for a small rally in the pound, depending on the tone of the bank’s communications. A 25bp hike would be a fairly significant surprise for markets and, in our view, would likely trigger a rather sharp sell-off in the pound, regardless of how this is dressed up in the bank’s accompanying rhetoric.

Since the December meeting, we think that macroeconomic news out of the UK has mixed ramifications for monetary policy though, on balance, we are pencilling in another 50bp rate increase this week. The focus among committee members clearly remains on inflation and, as of yet, we are yet to see clear evidence of a downward trend in either the headline or core CPI measures. One could argue that the surprise to the downside in the December UK inflation report has slightly taken the pressure off the MPC this week. In our view, this will not be enough to materially shift the hawks off course. Core inflation has remained particularly sticky, and has printed above 6% in each of the past six months.Figure 1: UK Inflation Rate (2017 - 2022)We suspect that the hawks among the committee will argue that this is not compelling enough evidence to begin winding down the hiking cycle, and that more needs to be done to ensure a return to the bank’s 2% inflation target. In our view, the BoE is not yet in the same boat as the Federal Reserve, which both tightened policy more aggressively than the MPC in 2022 (425bp vs. 325bps), and has witnessed clearer signs of a downtrend in domestic inflation. A likely point of contention and discussion among policymakers will perhaps be the recent signs of a deterioration in UK economic activity, most notably signs of weakness in retail sales and the services sector. This could lead to a few more dovish dissents among members, although again we do not believe that this will be enough to tip the balance in favour of a smaller hike, particularly as overall growth is proving rather resilient. Figure 2: UK Key Macroeconomic Data [since 15/12/2022] By contrast to the December meeting, financial markets are not yet fully accounting for a 50bp hike ahead of Thursday’s announcement. Another 50bp move is now around 80% priced in according to swap valuations, which we believe may perhaps be a consequence of interest rate repricing globally and the dovish vote and muddled communications among committee members in December. In the event of a half a percentage point move we do, therefore, see scope for a small rally in the pound, depending on the tone of the bank’s communications. A 25bp hike would be a fairly significant surprise for markets and, in our view, would likely trigger a rather sharp sell-off in the pound, regardless of how this is dressed up in the bank’s accompanying rhetoric.