17 July 2020

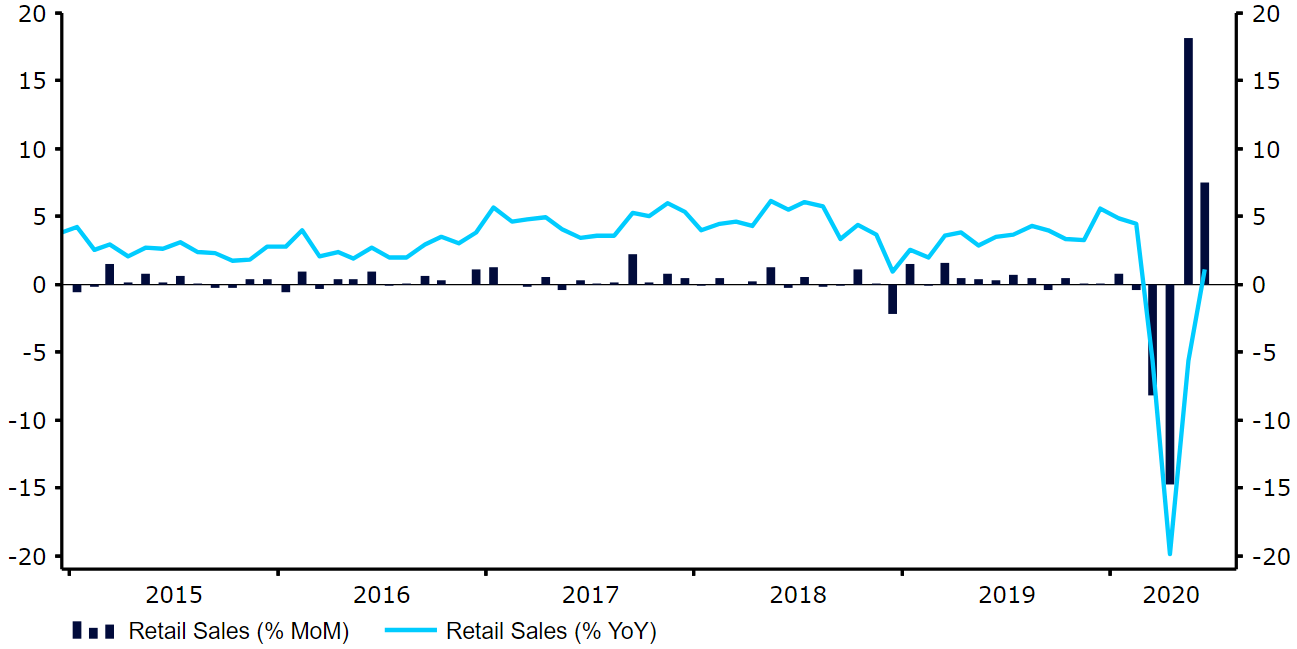

In what we billed to be one of the more eventful days in the currency markets for a number of weeks, ended with most major currencies stuck within relatively narrow ranges.As expected, Thursday’s European Central Bank announcement was a very low-key one, with not much in the way of new information offered by President Christine Lagarde. Policy was kept unchanged, with no alteration to interest rates or the bank’s asset purchase programmes. On the topic of its PEPP programme, Lagarde stated that it was working well and that the ECB would use the full allocation of purchases unless there was a ‘significant upside surprise’. A handful of senior policymakers have noted that the full 1.35bn euros allocation of purchases may not be required given the recent improvements in Euro Area data.Lagarde did, however, stop short of talking up the economy too much, instead keeping a relatively measured approach that noted the still significant downside risks facing the economy. The euro briefly eked out some gains following her comments, although the move was only very minor and short-lived. Attention now shifts to the two-day meeting of EU leaders, which begins today. We think that news of a passing in the EU’s 750bn euro fiscal rescue package could send the euro higher in the coming trading sessions. US retail sales rise again, but virus uncertainty lingersThe US dollar managed to end London trading yesterday slightly stronger versus the euro and more-or-less unmoved versus sterling - the latter receiving very little assistance from yesterday’s stronger-than-expected UK labour report.The greenback received only minor support from Thursday's much stronger-than-expected US retail sales data, which bode well for the strength of the economy’s recovery. Sales in retail sales jumped by 7.5% month-on-month in June, larger than the 5% increase that the market had priced in. While this marks a moderation on the previous months’ revised 18.2% increase, no one expected another reading anywhere remotely as strong given the very low base that the May data was working off. Figure 1: US Retail Sales (2015 - 2020)

US retail sales rise again, but virus uncertainty lingersThe US dollar managed to end London trading yesterday slightly stronger versus the euro and more-or-less unmoved versus sterling - the latter receiving very little assistance from yesterday’s stronger-than-expected UK labour report.The greenback received only minor support from Thursday's much stronger-than-expected US retail sales data, which bode well for the strength of the economy’s recovery. Sales in retail sales jumped by 7.5% month-on-month in June, larger than the 5% increase that the market had priced in. While this marks a moderation on the previous months’ revised 18.2% increase, no one expected another reading anywhere remotely as strong given the very low base that the May data was working off. Figure 1: US Retail Sales (2015 - 2020) Perhaps the lack of a more meaningful rally in the dollar can be attributed to the uncertainty about what’s to come for the US economy. Another daily record high number of COVID cases were recorded in the US yesterday - now more than 70,000. Infections are continuing to rise in the majority of US states, with a handful reporting record high death tolls. With containment measures being rolled back to prevent the spread of the virus, it is likely that this strong recovery so far witnessed in US economic data may prove short-lived.European inflation and US housing data will both be released today. Aside from any significant surprises here, we think that the major currencies could be driven more by shifts in general market sentiment.

Perhaps the lack of a more meaningful rally in the dollar can be attributed to the uncertainty about what’s to come for the US economy. Another daily record high number of COVID cases were recorded in the US yesterday - now more than 70,000. Infections are continuing to rise in the majority of US states, with a handful reporting record high death tolls. With containment measures being rolled back to prevent the spread of the virus, it is likely that this strong recovery so far witnessed in US economic data may prove short-lived.European inflation and US housing data will both be released today. Aside from any significant surprises here, we think that the major currencies could be driven more by shifts in general market sentiment.

US retail sales rise again, but virus uncertainty lingersThe US dollar managed to end London trading yesterday slightly stronger versus the euro and more-or-less unmoved versus sterling - the latter receiving very little assistance from yesterday’s stronger-than-expected UK labour report.The greenback received only minor support from Thursday's much stronger-than-expected US retail sales data, which bode well for the strength of the economy’s recovery. Sales in retail sales jumped by 7.5% month-on-month in June, larger than the 5% increase that the market had priced in. While this marks a moderation on the previous months’ revised 18.2% increase, no one expected another reading anywhere remotely as strong given the very low base that the May data was working off. Figure 1: US Retail Sales (2015 - 2020)Perhaps the lack of a more meaningful rally in the dollar can be attributed to the uncertainty about what’s to come for the US economy. Another daily record high number of COVID cases were recorded in the US yesterday - now more than 70,000. Infections are continuing to rise in the majority of US states, with a handful reporting record high death tolls. With containment measures being rolled back to prevent the spread of the virus, it is likely that this strong recovery so far witnessed in US economic data may prove short-lived.European inflation and US housing data will both be released today. Aside from any significant surprises here, we think that the major currencies could be driven more by shifts in general market sentiment.