27 July 2020

The main theme in currency markets continues to be general US dollar weakness. The greenback dropped against all of its major peers last week. The move was notable because it took place in the absence of typical dollar-bearish trends elsewhere. Risk assets generally fell, and interest rate differentials between the US and elsewhere were for the most part unchanged. Strategists seem to be ascribing this weakness to the euphoria surrounding the agreement over the approval of the EU recovery fund, but that does not explain dollar falls against other currencies, including emerging market ones. We maintain the view that concerns over governance and state capacity in the US, highlighted by the poor response to the COVID pandemic, are at least partly to blame. Either way, the euro rose to its highest levels vs. the dollar since September 2018. As this is written, it is rallying sharply again during early morning Asian trading.This week is packed with news on both the economic and policy front. The Federal Reserve meeting on Wednesday and the rhetoric emanating therefrom will be key for the US dollar. Friday will be a packed data day from the Eurozone, as second quarter GDP data and flash July inflation are released simultaneously. The former, in particular, will provide the first comprehensive gauge of the damage wrought by the pandemic on the economy of the Eurozone.

Source: Refinitiv Datastream Date: 27/07/2020This week, the UK calendar for macroeconomic data looks pretty thin, in contrast with those across the Channel or the Atlantic. Therefore, we expect sterling to largely track the euro's move against the US dollar.

Source: Refinitiv Datastream Date: 27/07/2020This week, the UK calendar for macroeconomic data looks pretty thin, in contrast with those across the Channel or the Atlantic. Therefore, we expect sterling to largely track the euro's move against the US dollar.

GBP

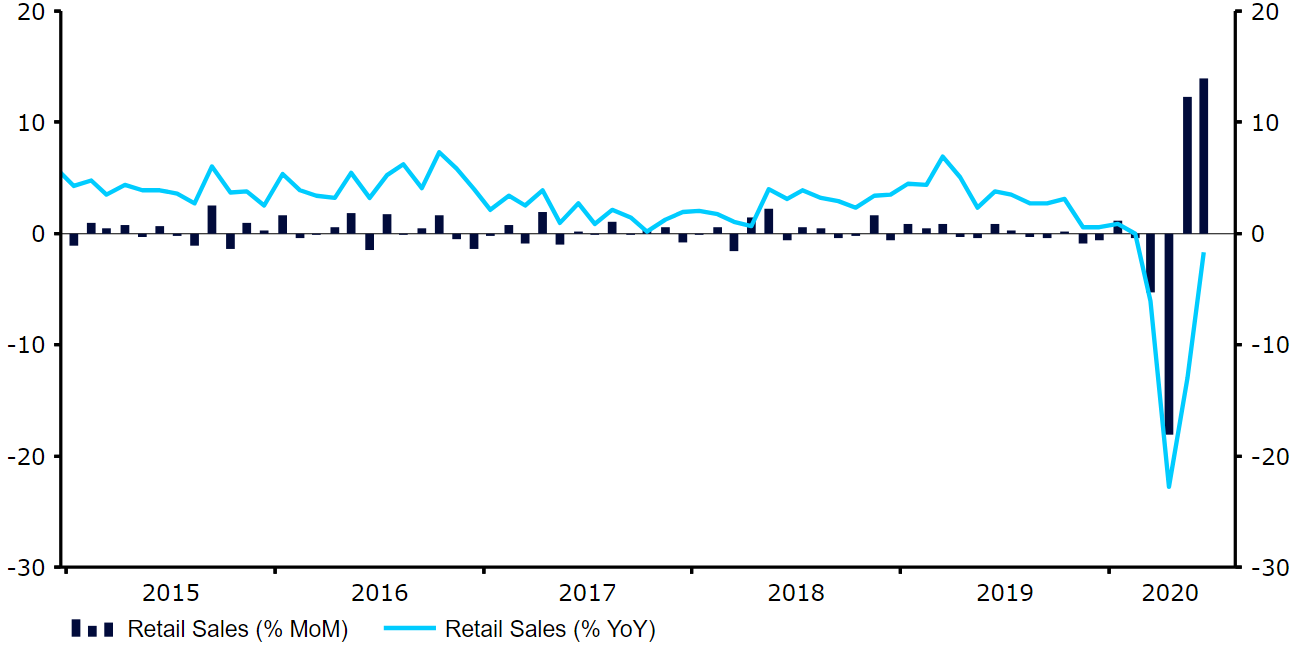

Macroeconomic news that we had out of the UK last week was broadly encouraging. Most notable was Friday’s retail sales figures, which posted a significantly sharper-than-expected rebound in June (Figure 1), lifting sales back up to where they were prior to the lockdown. In spite of good economic news, the absence of signs of progress in the Brexit negotiations with the EU prevented the pound from keeping up with the euro’s rally, though it did manage to post significant gains against the US dollar. Figure 1: UK Retail Sales (2015 - 2020)Source: Refinitiv Datastream Date: 27/07/2020This week, the UK calendar for macroeconomic data looks pretty thin, in contrast with those across the Channel or the Atlantic. Therefore, we expect sterling to largely track the euro's move against the US dollar.