24 August 2020

The recent sharp sell-off that we’ve witnessed in the US dollar against the euro since pretty much the end of May was brought to a screeching halt last week.One of the main rationales for the weaker dollar has, in our view, been the divergence in new virus cases between the US and Europe, and concerns that prolonged shutdown orders could cause the US economic recovery to lag its major counterparts. This was turned on its head slightly last week, with the latest PMI activity data suggesting that the recovery in the Euro Area economy may be stuttering as business owners fear a possible second wave of virus infection in Europe.The minutes of the most recent Federal Reserve meeting also provided the dollar with some support on Wednesday. This helped the greenback snap nine consecutive weeks of losses and end its longest losing streak since 2010. Meanwhile, sterling was buffeted in both directions, first buoyed by a strong set of UK economic data, only to be dragged lower again by some rather troublesome headlines that suggest a post-Brexit trade deal may be off the table.Investors’ view towards the recent spike in new COVID cases in Europe could drive the currency markets this week in the absence of any timely macroeconomic news out of either side of the Atlantic. We will also be paying close attention to comments from central bank heads during the annual Jackson Hole Economic Symposium on Thursday and Friday.

Source: Refinitiv Datastream Date: 24/08/2020With no tier-1 data out of the UK this week, the pound may continue to be driven largely by Brexit headlines in the coming days.

Source: Refinitiv Datastream Date: 24/08/2020With no tier-1 data out of the UK this week, the pound may continue to be driven largely by Brexit headlines in the coming days.

GBP

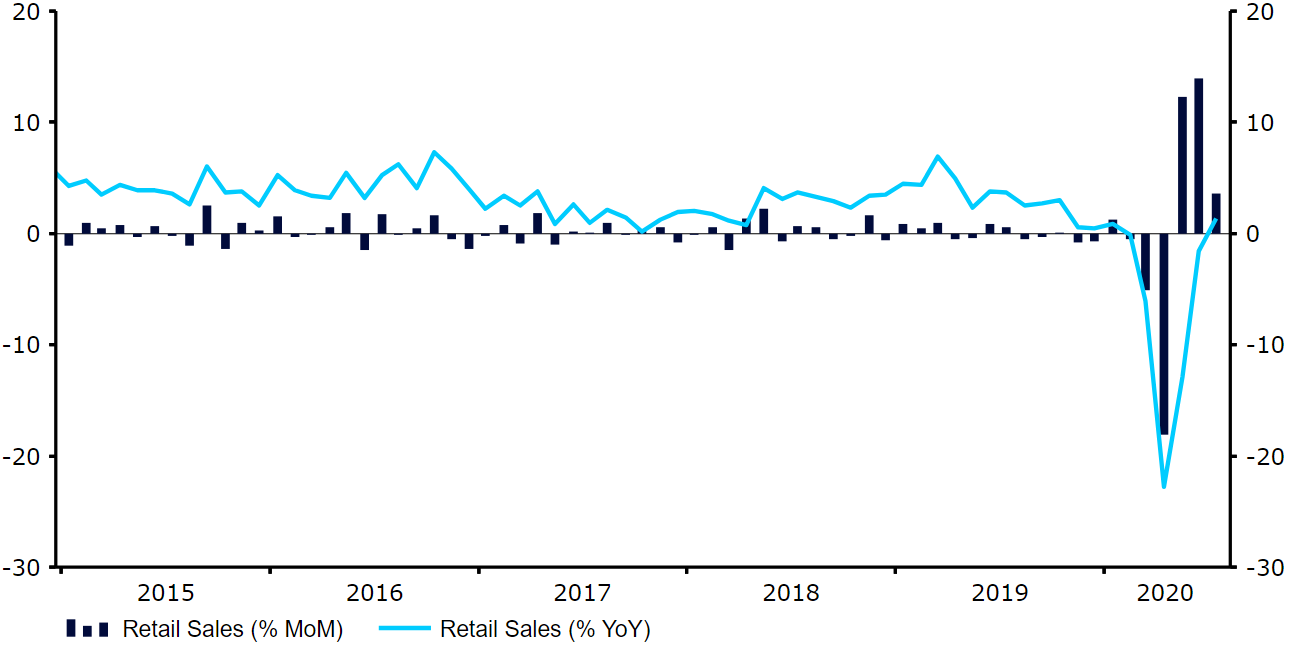

Macroeconomic news out of the UK last week was highly encouraging, albeit overshadowed by Friday’s very downbeat comments from Brexit negotiator Michel Barnier. Retail sales surged back past their pre-pandemic levels in July, with consumer spending activity higher than the same period a year previous. Business activity also appears to be faring well, with the August services PMI leaping to its highest level since 2014. The famous resilience of the British public in the face of a crisis will be tested in earnest in the next few months, particularly once the government's furlough scheme ends in October. There are suggestions that July could therefore mark the peak of the recovery, rather than the sign of things to come, but time will of course tell.With no tier-1 data out of the UK this week, the pound may continue to be driven largely by Brexit headlines in the coming days.Figure 1: UK Retail Sales (2015 - 2020)Source: Refinitiv Datastream Date: 24/08/2020With no tier-1 data out of the UK this week, the pound may continue to be driven largely by Brexit headlines in the coming days.