20 April 2020

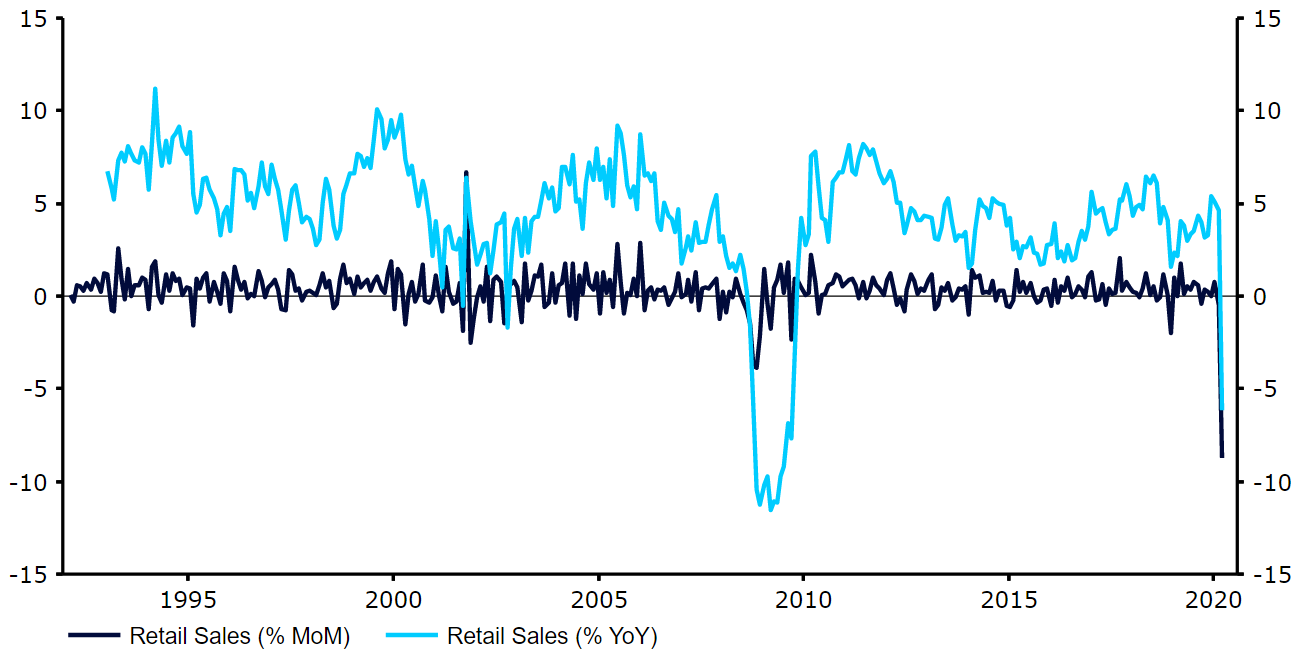

Currency markets have experienced a relatively calm past week, which is a welcome change after the Covid-related convulsions of the past two months.G10 currencies ended up within 1% of where they started the week, with the exception of the Norwegian krone, battered once again by another sell-off in oil prices. The main exceptions were emerging market currencies either exposed to the oil prices (the Colombian and Mexican pesos) or those with particularly fragile fundamentals (the South African rand, Turkish lira).As some countries start to ease up their covid lockdown restrictions, markets will focus on the evolution of contagion data there. The preliminary April PMIs of business activity will be released in the Eurozone, the US and the UK, providing a near-real time read on economic weakness. The numbers are likely to be so low that their usefulness will be limited. More important will be the weekly jobless numbers out of the US, which will shed further light on the damage done to the US labour market.GBPAfter a relatively quiet April thus far, this week may well see some serious volatility in Sterling. We will get the first batch of economic data fully reflecting the damage wreaked by the crisis in the coming days.In addition to the PMIs mentioned above, which are all but certain to tumble to fresh record lows for April, the drop in retail sales data for March, out on Friday, will also get much attention. The numbers for the latter are likely to be dismal given the implementation of the lockdown measures mid-way through the month, although it's worth pointing out that expectations are already very low. Tuesday will also see the release of the latest labour report, although this runs on slightly more of a lag and will therefore only reflect the now largely irrelevant pre-crisis period.EURWhile the April PMIs are certain to be a market focus on Thursday, they are likely to be so low that a few points up or down will not contain that much information.We are seeing some jitters around the Thursday Eurogroup meeting and Friday's review of Italian sovereign rating by S&P. We think concerns about both are overstated. Existing ECB facilities, in particular the newly minted PEPP, are enough to carry Italy and Spain through whatever fiscal stimulus is needed to get over the crisis. We expect S&P to acknowledge this reality and keep Italy's rating unchanged, which will be a clear positive for the common currency going into the following week.USDEconomic data out of the US last week continued to show just how significant of an impact the COVID-19 crisis is having on the world’s largest economy, particularly its labour market. March retail sales were down 8.1%, its largest drop on record, with another 5.25 million jobs lost due to the crisis in the week according to the latest jobless claims figure.Figure 1: US Retail Sales (1991 - 2020) Source: Refinitiv Datastream Date: 20/04/2020We think the scale of labour market damage we are seeing in the US will dwarf similar numbers out of the Eurozone. In this case, more rigid European employment rules and higher difficulty in laying off staff may prove a blessing. On the plus side, the massive enhancement to traditionally stingy US jobless benefits approved by Congress in response to the crisis will mitigate the job destruction to some extent. We continue to see a lower US dollar against European currencies.

Source: Refinitiv Datastream Date: 20/04/2020We think the scale of labour market damage we are seeing in the US will dwarf similar numbers out of the Eurozone. In this case, more rigid European employment rules and higher difficulty in laying off staff may prove a blessing. On the plus side, the massive enhancement to traditionally stingy US jobless benefits approved by Congress in response to the crisis will mitigate the job destruction to some extent. We continue to see a lower US dollar against European currencies.

Source: Refinitiv Datastream Date: 20/04/2020We think the scale of labour market damage we are seeing in the US will dwarf similar numbers out of the Eurozone. In this case, more rigid European employment rules and higher difficulty in laying off staff may prove a blessing. On the plus side, the massive enhancement to traditionally stingy US jobless benefits approved by Congress in response to the crisis will mitigate the job destruction to some extent. We continue to see a lower US dollar against European currencies.