24 March 2021

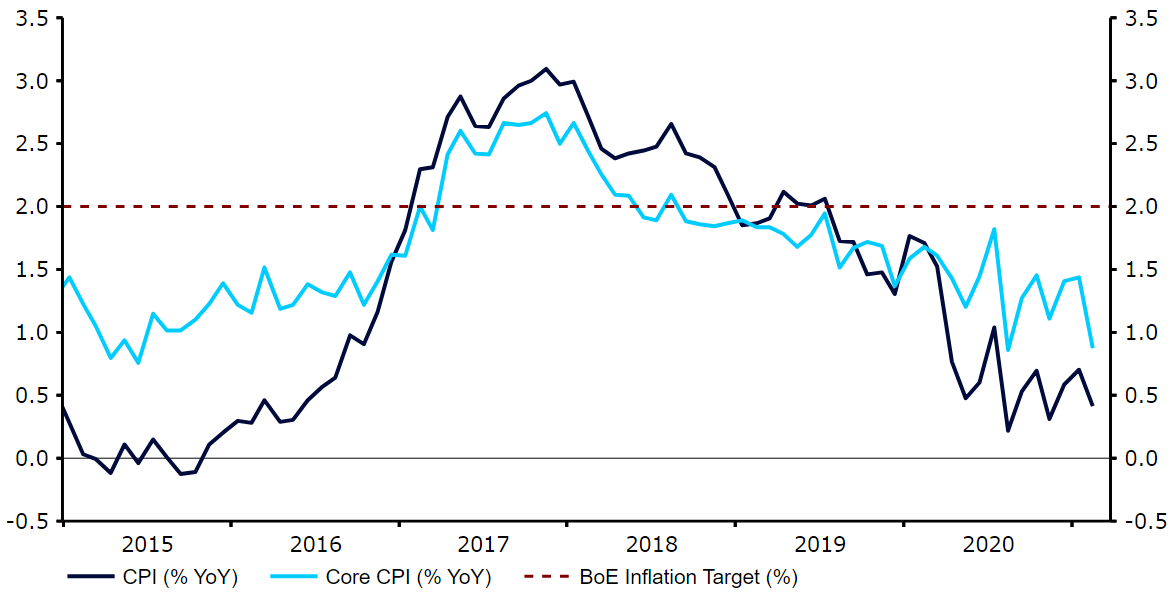

The US dollar continued to advance against its major peers on Tuesday, rising to its strongest position in four months, as investors sought the safety of the currency amid concerns over rising virus cases in Europe. Sterling has been among the currencies to bear the brunt of the sell-off in major risk assets, with the pound briefly collapsing below the 1.37 level this morning - down more than 1% for the week so far. Tensions surrounding the EU’s threat to block vaccine shipment to the UK has slightly soured sentiment towards sterling. The topic of vaccines will be high on the agenda at this Thursday’s European Council meeting. While we see an export ban as unlikely, the threat of one, combined with the news that vaccine supply is set to drop in April, has been enough for the pound to lose its mantle as the best performing G10 currency in 2021. This week is a very data heavy one in the UK. A larger than expected drop in the unemployment rate to 5% from 5.2% provided little assistance to the pound yesterday. A sharp decline in February inflation data out this morning has also weighed on the currency, which is currently trading around its weakest position since the first week of February on the dollar. The headline rate of consumer price growth slipped to just 0.4% year-on-year last month, well short of the 0.8% expected. This will likely quash any lingering thoughts that the Bank of England might be in a position to raise interest rates in the UK any time soon. Figure 1: UK Inflation Rate (2015 - 2021) Source: Refinitiv Datastream Date: 24/03/2021Having said that, the March PMI numbers, also out this morning, provided reason for optimism, with both the manufacturing and services indices coming in much higher than consensus. The jump in the services PMI to a comfortably expansionary 56.8 from 49.5 is a particularly welcome development and suggests that the downturn in activity in the first quarter may not be as bad as first feared.

Source: Refinitiv Datastream Date: 24/03/2021Having said that, the March PMI numbers, also out this morning, provided reason for optimism, with both the manufacturing and services indices coming in much higher than consensus. The jump in the services PMI to a comfortably expansionary 56.8 from 49.5 is a particularly welcome development and suggests that the downturn in activity in the first quarter may not be as bad as first feared.

Source: Refinitiv Datastream Date: 24/03/2021Having said that, the March PMI numbers, also out this morning, provided reason for optimism, with both the manufacturing and services indices coming in much higher than consensus. The jump in the services PMI to a comfortably expansionary 56.8 from 49.5 is a particularly welcome development and suggests that the downturn in activity in the first quarter may not be as bad as first feared.