Dollar slammed as turmoil engulfs Trump presidency

- Go back to blog home

- Latest

22 May 2017

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Politics have become front and centre once again in FX markets. The steady drip of sensational developments has finally started to impact risk assets in general.

The Brazilian Real was also hammered by a major scandal that appeared to directly implicate President Temer in bribes. The Real fell over 5% after the scandal hit the newswire, with Brazilian stocks and bonds also suffered heavy losses.

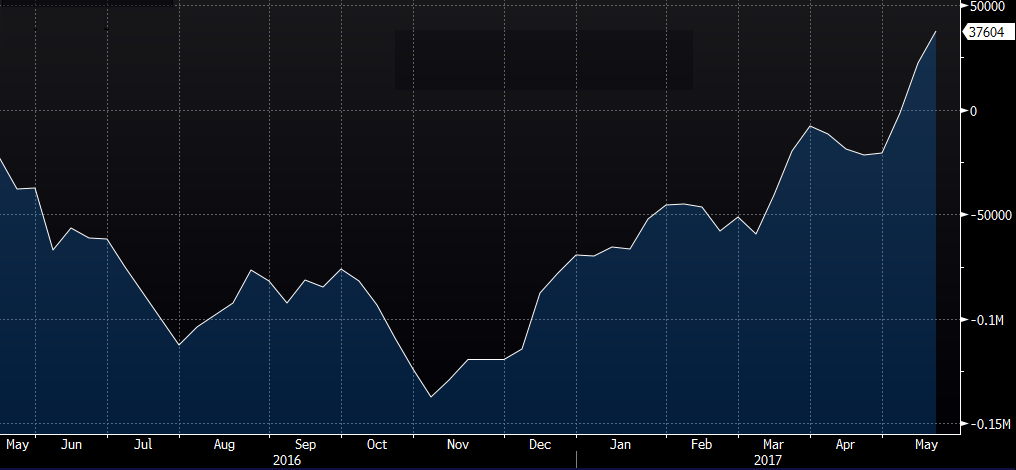

This week is relatively light in terms of major economic data. The Eurozone PMI indices of business activity should confirm that the Eurozone recovery remains on track. Also, traders’ short Euro positions appear to be fully unwound (Figure 1), which is often a useful contrarian indicator. We therefore think that risks on EUR/USD are skewed somewhat to the downside going into the Fed’s April meeting minutes on Wednesday.

Figure 1: Euro Net Positioning (May ‘16 – May ‘17)

Major currencies in detail

GBP

Sterling managed to clear the psychological 1.30 level against the US Dollar, if only barely. We saw mixed economic data, including strong retail sales figures for April, higher inflation, solid employment growth, but lower-than-expected wage growth. It bears noting that since the Brexit referendum, real wage growth has turned sharply negative as inflation outpaces wages.

The data calendar in the UK is quiet this week. Sterling will trade mostly in reaction to events elsewhere, in particular any further political developments regarding the Trump investigation across the Atlantic.

EUR

Political risk appears to have crossed the Atlantic for the time being. Markets received further encouragement on Eurozone political news from the strong polling of President Macron’s new En Marche! party in the upcoming legislative elections, while the scandals surrounding the Trump presidency gather more and more attention.

The PMIs should confirm strong levels of business activity consistent with growth above the 2% level. However, in the absence of any further bombshells from the White House there is some potential from Euro to pull back, as the divergence of monetary policies reasserts itself.

USD

Last week saw a new development in currency markets. Investors are starting to react to the disarray in the Trump White House and the uncertainty about Trump’s future by pricing political risk in the Dollar. The US currency started falling around the announcement of Comey’s firing late on 9th May. It has continued to drop in the days since, in spite of a near complete absence of key macroeconomic data or monetary policy developments. This sort of “risk premium” associated with the Dollar appears to be the obverse of a “political risk premium” that we have so often heard about during the multiple Euro crises’. It is, however, the first time that we see such a development on the other side of the Atlantic.

Whatever the actual outcome of the current Trump crisis, it is clear that it will be very difficult to get any significant fiscal stimulus or infrastructure spending passed through Congress this year, which will weigh on Federal Reserve hikes and the US Dollar. This probably means that, as has been the case in Europe in the past, we need to start paying close attention to political developments in the US in order to explain movements in financial assets and the currency markets.

SHARE