Dollar reverses gains amid concerns over US economy

- Go back to blog home

- Latest

3 October 2019

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

Concerns over the health of the US economy caused the US dollar to slip to its lowest level in a week against both the euro and the yen on Thursday morning.

To make matters worse, the US yesterday won approval to slap additional tariffs on imported European goods. The tariffs, set to take effect on 18th October, will include 10% import taxes on Airbus planes and 25% duties on French, Irish and Scottish wine amongst others. With no end in sight for US protectionism, investors continue to favour the safe-havens and are ramping up bets for more Fed rate cuts, with the next one heavily expected to come in December.

Investors will, of course, now have one eye on tomorrow’s all-important nonfarm payrolls report, which will give us a better indication as to how the US labour market is performing going into the final quarter of the year. We’ll be looking primarily at whether the moving average job creation levels are continuing to decline and, arguably more importantly, whether we’re seeing upward pressure on wages from multi-decade low unemployment. In the meantime, this afternoon’s ISM non-manufacturing PMI will be worth keeping tabs on. Following Tuesday’s dire manufacturing index, investors are bracing for another downside surprise to today’s number.

Pound recovers after UK construction PMI miss

Sterling briefly fell towards a fresh one month low on the dollar yesterday morning, before recovering as the day progressed to end the London session higher against the greenback.

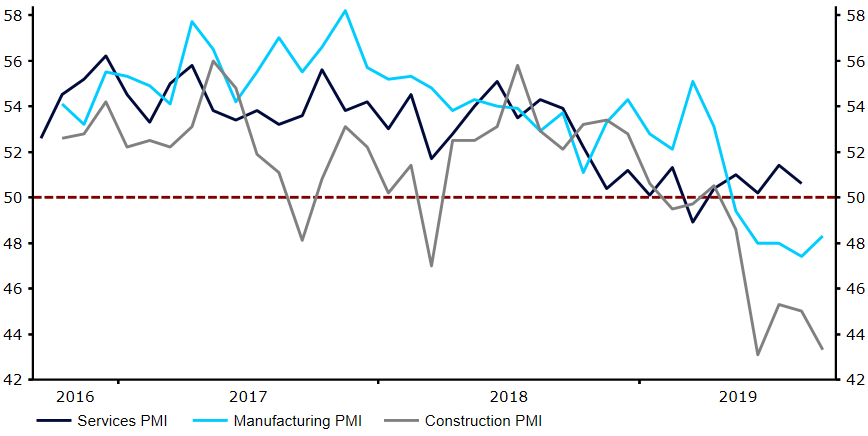

Much of Wednesday morning’s weakness in the pound can be attributed to another dismal PMI reading. The construction index massively undershot expectations, causing investors to fret about the state of the UK economy. The index unexpectedly fell to 43.3 in September (Figure 1), short of the 45.0 that investors had priced in. While not quite as low as June’s ten year low, it does mark the fifth straight month that the measure has been below the level of 50 that denotes contraction.

Investors didn’t get too carried away, largely due to the fact that the sector only accounts for around 7% of overall UK output. A similarly poor number from this morning’s service PMI would almost certainly trigger a much larger sell-off in the UK currency.

Figure 1: UK PMIs (2016 – 2019)

Sterling did, however, recover during the course of the day following Boris Johnson’s speech at the Conservative Party conference, at which he proposed creating an all-island regulatory zone in Ireland to break the NI border impasse. Volatility in the pound is likely to ramp up in the coming weeks ahead of the end of month Brexit deadline. Any signs that we could be heading towards either a last minute deal or, more likely, another delay, could provide room for a decent rally in the UK currency.

SHARE