Dollar falls back as emerging market rally grinds on

- Go back to blog home

- Latest

15 April 2019

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

Perhaps the biggest news of last week was the agreement to postpone Brexit until 31st October. Financial markets did, however, seem to have priced in the outcome entirely, and Sterling did not react strongly to the news.

This week the critical April PMI surveys of business activity for the Eurozone come out on Thursday. With mostly second tier data out of the US and Brexit on temporary hold, we would expect most G10 FX volatility to be seen in reaction to this data.

Major currencies in detail

GBP

Theresa May agreed with the EU to extend the Brexit deadline to the end of October, which would ensure the UK participates in the European Elections in May.

This week, we expect economic data to finally receive some attention now that the Brexit issue is temporarily postponed. Tuesday’s labour report and Wednesday’s inflation data will give us some key, albeit lagged insight into how well the UK economy is navigating the uncertainty surrounding Brexit.

EUR

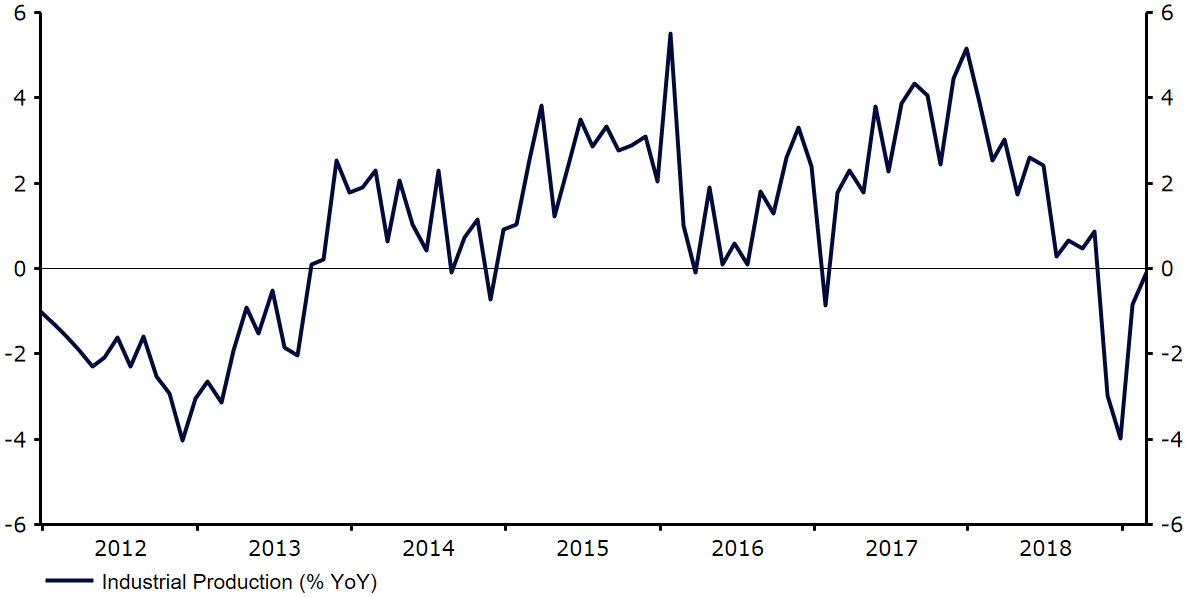

The absence of any meaningful policy announcements at the ECB’s April meeting provided a badly needed boost for the Euro. Although communications from the central bank had a distinctly dovish tilt, it seems that for now, no news out of the Eurozone means good news for the Euro. The common currency also took some comfort from better-than-expected industrial production data, albeit this continued to remain in negative territory year-on-year (Figure 1).

Figure 1: Eurozone Industrial Production (2012 – 2019)

Thursday’s flash PMI data for April seems particularly critical to us. We expect them to surprise to the upside, confirming that the slowdown in industrial production is due mostly to one-off factors that are now clearing up.

USD

The release of the minutes from April’s Federal Reserve meeting did little to explain the sharp dovish turn in Fed thinking since late last year.

Members remain puzzled by quiescent inflation – the modest downward surprise in March CPI numbers published last week will not help them. The Fed remains on hold for the foreseeable future. The combination of steady worldwide growth and low rates in developed countries is a potent mix for an emerging market currency rally.

SHARE