How will tonight’s Fed rate cut impact the US dollar?

- Go back to blog home

- Latest

31 July 2019

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The Federal Reserve is overwhelmingly expected to cut interest rates at its monetary policy meeting tonight, the first time it has done so since 2008. But what impact will the impending rate cut have on the US dollar?

The key to the reaction in the currency markets will therefore not be the rate cut itself, but the Fed’s view on the need for additional policy easing. Should the Fed indicate that tonight’s cut is a ‘one and done’ policy decision, we would likely see a sharp knee jerk rally in the dollar. By contrast, a scenario where the vote to cut is unanimous with Chair Jerome Powell indicating that additional 25 basis point rate reductions are likely would see the dollar sell-off sharply.

We think that the reality will lie somewhere in between. At the June FOMC meeting, the Fed made it clear that future policy action would be data dependent. Macro data since the last meeting has been slightly better-than-expected, with a rebound in nonfarm payrolls and retail sales numbers suggesting that the US economy is riding out the storm created by US-China trade tensions. We therefore think that Powell is likely to keep the door ajar to additional policy action if required, albeit stress that this will be entirely driven by upcoming economic data.

Pound holds firm following violent sell-off

With no major news on the Brexit front out yesterday, the Pound was able to trade sideways against its major peers, pausing for breath after a violent sell-off that has seen it fall to more than two year lows against its US counterpart. The sell-off witnessed in sterling in July has been aggressive, with the UK currency losing over 4% of its value versus the dollar and around 2.5% on the common currency.

As we have already mentioned this week, the path of least resistance for the pound in the coming weeks is lower until we get some positive news on the Brexit front that alleviates the heightened possibility of a ‘no deal’. Following Boris Johnson’s rather forthright comments on the possibility of a ‘no deal’ last week, some bookmakers are now placing a close to 45% implied probability of such an outcome.

Eurozone growth and inflation fall to new lows

Ahead of tonight’s Fed meeting, the EUR/USD rate has edged modestly higher in the past 24 hours despite some relatively downbeat macroeconomic news out of the Eurozone.

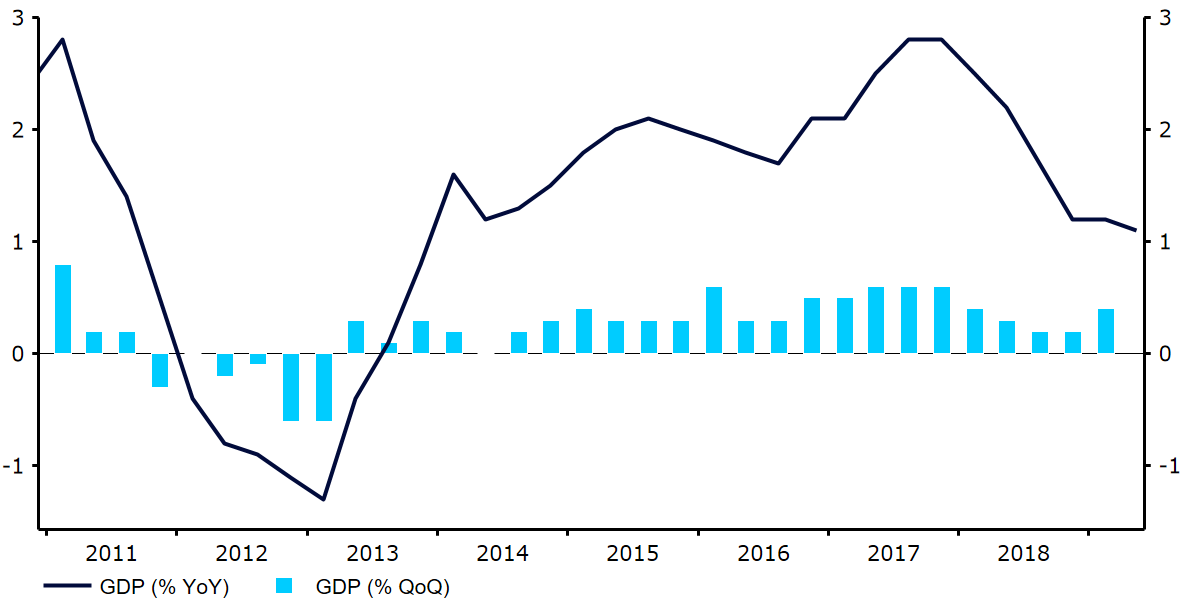

This morning’s preliminary growth data for the second quarter confirmed suspicions that the Eurozone economy expanded by a fairly meagre 0.2% in the three months to June and by just 1.1% year-on-year. Remarkably this is the bloc’s slowest pace of yearly expansion since the final quarter of 2013. Euro Area inflation also came in at an underwhelming 1.1% in July, well short of the 2% target and its joint lowest level since February 2018.

This near negligible level of expansion and lack of inflationary pressure will be a significant cause for concern for the European Central Bank and further fuels the argument that policy makers in the bloc will announce easing measures aimed at stimulating the economy at its next meeting in September.

Figure 1: Eurozone Annual GDP Growth Rate (2011 – 2019)

SHARE