Markets rattled after Trump imposes fresh Chinese tariffs

- Go back to blog home

- Latest

2 August 2019

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

Financial markets were rattled yesterday evening by the surprise announcement that US President Donald Trump had slapped additional tariffs on a further $300 billion worth of Chinese goods, effective 1st September.

Unsurprisingly, the safe-haven Japanese yen rallied hard on the news, appreciating by around 2% against the US dollar to its strongest position in over a month. The reaction in EUR/USD was fairly limited considering the extent of the tariffs and its potential impact on US monetary policy. Expectations for additional easing from the Federal Reserve have been ramped up in the past 24 hours, with the market now pricing in around a 95% chance of another rate cut in September versus approximately 70% prior to Trump’s announcement.

An escalation of the trade conflict was one of the primary reasons why the Fed cut interest rates for the first time in over a decade earlier this week and may well force the central bank to act again later in the year.

Bank of England slashes UK growth forecasts

Thursday’s policy announcement from the Bank of England largely went under the radar, as we had anticipated, with the reaction in the pound pretty limited.

The BoE kept rates unchanged, continuing to reiterate that it would await more concrete news on Brexit before it decides on its next policy move. Policymakers reiterated their assumption that the UK would leave the EU with a deal in place, although a ‘no deal’ would force the bank to cut interest rates from current levels. Amid the growing uncertainty from Brexit, the BoE downgraded its outlook for the UK economy, lowering its growth forecast for this year to 1.3% from 1.5% and to 1.3% for 2020 from 1.6%.

It is clear that future policy from the BoE rests entirely with Brexit. We think that policymakers are unlikely to even signal the next move until it gets more concrete details on the manor of the UK’s exit from the bloc.

Eurozone manufacturing activity ticks upwards

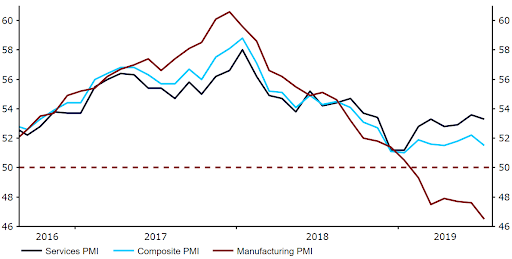

Over in the Eurozone, yesterday’s PMIs from Markit were relatively encouraging, with manufacturing activity picking up modestly in July from a month previous. The index for July rose to 46.5 from 46.4 in June (Figure 1). While a slight improvement, this remains deep in contractionary territory and the reaction in EUR/USD was therefore rather limited.

Figure 1: Eurozone PMIs (2016 – 2019)

Next up will be this morning’s Euro Area retail sales data. A downside surprise here would ramp up bets that the European Central Bank is on course to cut interest rates at its next meeting in September in a bid to stimulus the domestic economy.

SHARE