Dollar bounces on higher yield as euro breaks below parity

( 5 min )

- Go back to blog home

- Latest

22 August 2022

Matthew Ryan is Ebury’s Global Head of Market Strategy, based in London, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.

US bond yields have now retraced the fall that followed the positive inflation report from the week prior.

This week, the critical PMI advance indicators of business activity will be released in the US, the UK and Eurozone. Current levels mostly hover around the 50 line that separates expansion from contraction, so these numbers take on added importance. At the end of the week, markets await headlines and speeches from the annual meeting of the world’s central bankers in Jacksonhole, Wyoming. In particular, Chair Powell’s speech on Friday is expected to offer some clarity on the speed of coming hikes and, just as important, his expectations on how high rates will have to go before inflation is brought back under control.

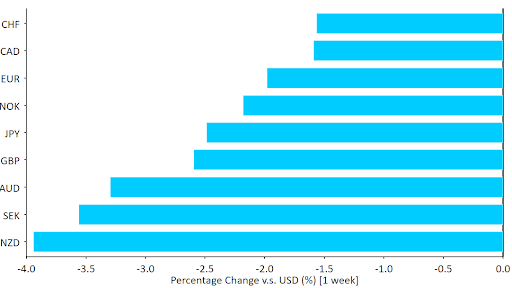

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Source: Refinitiv Datastream Date: 22/08/2022

GBP

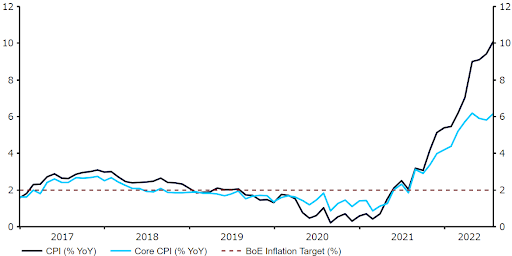

Bank of England policy makers received an unpleasant jolt last week, in the form of a significant upward surprise in the inflation numbers for July. Both the headline and the core rate soared to fresh record highs, the former now in double digits and expected to peak at 13% in the autumn. Markets rushed to price in more hikes from the Bank of England, but the threat of stagflation meant that sterling failed to benefit and fell against both the dollar and the euro.

Figure 2: UK Inflation Rate (2016 – 2022)

Source: Refinitiv Datastream Date: 22/08/2022

The PMIs in the UK have held up better than in the Eurozone, suggesting a more resilient economy than is priced in at current pound levels, but this view will be tested this week when the advance August numbers are released on Tuesday.

EUR

Last week was a typically sluggish summer one in the Eurozone. With little macroeconomic or policy news, the euro mostly traded down as US rates soared and sentiment towards the Eurozone economy deteriorated on soaring energy prices. While macroeconomic news out of the bloc has held up reasonably well so far under the circumstances, the jump in energy prices continues to worsen the outlook, and has helped drive EUR/USD back through parity levels this morning.

As elsewhere, the PMI advance indices on Tuesday will be key. However, given how far behind the curve the ECB is with respect to inflation, we do not think that it can afford to let up on policy normalisation, even if a mild recession materialises.

USD

Strong second tier data and a determined push back form Fed officials against any notion of a ‘dovish pivot’ drove US rates higher last week, and this in turn boosted the dollar. Last week’s FOMC meeting minutes were actually initially seen as dovish, although investors appeared to have a change of heart as focus shifted to the Fed’s comments on inflation, which indicated members saw no let up in price pressures.

This week, the PMIs are released on Tuesday, as elsewhere. However, they typically make less of a splash in the US. Markets will look to the PCE inflation report later in the week to corroborate the good news from the CPI report. Regardless, it is unlikely that the Fed will be deterred from its hiking campaign and the main question for Chair POwell atr Jackson Hole will be whether 50 or 75 bp are coming in September.

CHF

The Swiss franc has rallied to fresh highs against the euro in the past few trading sessions, with the EUR/CHF pair currently trading below the levels seen following the removal of the trading peg in early-2015. Broad euro weakness has dragged the pair lower so far this morning, although the franc is also benefiting from rising risk aversion, as markets brace for a slowdown in global growth between now and year end. Investors continue to favour the franc over its fellow safe-haven, the Japanese yen, in light of the policy divergence between the SNB and Bank of Japan.

Whether this outperformance continues may depend on SNB interventions. The bank actually appears to have been rather active in selling francs in the past few weeks, with total sight deposits, a proxy for interventions, increasing in every week since mid-July. This may be an indication that the EUR/CHF pair may be approaching a near-term low. There will be no major economic data releases out of Switzerland this week, so expect the franc to be driven largely by goings on elsewhere.

AUD

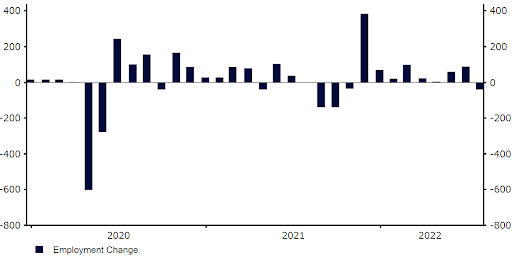

The Australian dollar was one of the worst performing currencies in the G10 last week, falling by almost 3% against the US dollar. Fears of an economic slowdown and a weaker than expected domestic jobs report hurt the Australian currency.

While the unemployment rate fell to a more than 40-year low of 3.4% in July, net employment dropped by 40,900, contrary to what was expected (+25k). This mixed report raises question marks about the magnitude of the next interest rate hike from the Reserve Bank of Australia. Prior to the meeting, markets were pricing in another 50 basis point move in September, although we think that this is now in serious doubt. Markets also appear torn, with swaps indicating a 50/50 chance of such a move.

Figure 3: Australia Net Employment Change(2017 – 2022)

Source: Refinitiv Datastream Date: 22/08/2022

Advanced PMIs for August will be published tomorrow, and are expected to show an improvement on July’s data. Aside from that, AUD will be driven by market risk sentiment and expectations about rate hikes.

CAD

The Canadian dollar depreciated against the US dollar last week, although the sell-off was smaller than that of its G10 peers. In line with expectations, Canada’s inflation rate fell to 7.6% in July, after reaching a near four-decade high in June, mainly due to a fall in gasoline prices. However, core inflation surprised on the upside and remains at very high levels, suggesting that price pressures have broadened across more components.

We believe that the Bank of Canada will continue its aggressive monetary tightening cycle, with a decent chance of a 75 basis point move at the next meeting in September. Markets are currency pricing in around a 50% chance of another bumper move, having seen very little chance of one this time last week. With no major domestic data to be released this week in Canada, we think that oil prices and market sentiment will be the main drivers of the Canadian dollar this week.

CNY

Somewhat uncharacteristically, the yuan underperformed most of its Asia counterparts last week, with the currency slumping to a near two-year low on the broadly stronger US dollar. A rather underwhelming set of macroeconomic figures released at the beginning of last week weighed on the yuan. Industrial production, fixed asset investment and retail sales data for July all fell short of expectations, as the prolonged COVID-19 restrictions in the country continue to worsen the growth outlook and sour sentiment towards Chinese assets.

The ongoing property crisis in China, and policy easing from the People’s Bank of China, are also far from helping the currency’s cause. The PBoC trimmed its one-year loan prime rate, albeit only by 5 basis points, to 3.65% on Monday, while lowering its five-year lending rate by 15 basis points to 4.3%. As long as Chinese authorities continue to staunchly stick by their zero-covid approach, additional rate cuts and sluggish domestic data appear likely. Both present clear downside risks to the yuan in the coming months.

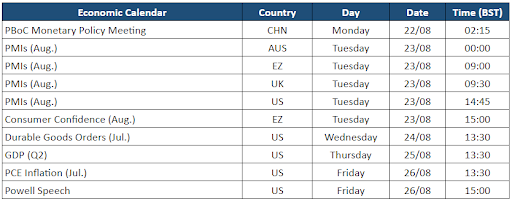

Economic Calendar (22/08/2022 – 26/08/2022)

To stay up to date with our publications, please choose one of the below:

📩 Click here to receive the latest market updates

👉 Our LinkedIn page for the latest news

✍️ Our Blog page for other FX market reports

SHARE