Dollar pullback continues amid emerging market volatility

( 3 min )

- Go back to blog home

- Latest

26 April 2021

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

The US dollar continued its recent trend lower last week, falling modestly against every G10 currency save the Australian dollar.

This week focus will be squarely on the Federal Reserve April meeting on Wednesday, although markets are not expecting any significant changes either in policy or communications from the Fed. US GDP growth (Thursday) and PCE inflation (Friday) are also key, as will be the Euozone flash inflation report for April and Q1 GDP data, both released Friday.

Sterling largely looked past last week’s strong data out of the UK, which saw higher rates of inflation, house prices and positive surprises in the April PMI indices of business activity and March retail sales. The latter, in particular, came in much stronger-than-expected, which bodes very well for growth in the second quarter of the year.

The pound’s rally has been cut short for now by jitters over the upcoming Scottish parliament elections and the potential for a second independence referendum there. Little news of any note this week means that sterling will probably take its trading cues from elsewhere, notably the Federal Reserve meeting on Wednesday.

EUR

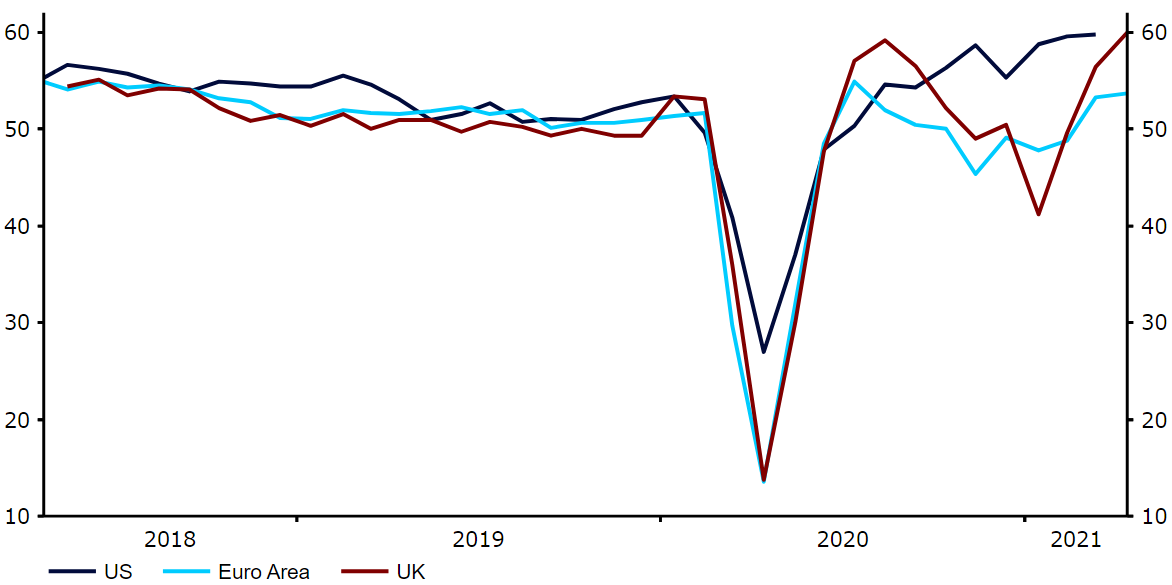

The improving tone in Eurozone economic data was confirmed last week by a very strong PMI report for the month of April and continued improvement in vaccination rates. The ECB also stayed out of the way of the euro rally by adding little new information in its April meeting.

Figure 1: G3 PMIs (2018 – 2021)

Source: Refinitiv Datastream Date: 23/04/2021

Overall, we think that the string of very positive economic surprises that we have seen in the US will now have its counterpart in the Eurozone, as lockdowns are progressively lifted and consumer pent up demand is felt, particularly in the services sector. Consequently, we think that the euro rally has a way to go yet.

USD

Wednesday’s meeting of the FOMC should be a non-event, with no changes to monetary policy settings and little in the way of fresh communications from the Fed, particularly given that there will be no updated economic or interest rate projections.

Far more interesting should be the two inflation-related data points this week. On Thursday, the GDP deflator for the first quarter, and then on Friday the personal consumer expenditure deflator for March. We expect both to continue the recent string of upward surprises in inflation data, which should start the next leg up in Treasury yields. What will be the immediate dollar reaction to inflation surprises is less clear, however.

📩 Click here to subscribe to our latest market insight and updates to help you navigate the ever-changing global currency markets.

🎙 Don’t miss our latest FX Talk episode to get your 20-minute financial update on Spotify, Google Podcast, Apple Podcast or simply choose your favourite podcast app here.

SHARE