Evidence continues to accumulate that inflation worldwide is far from tamed, and that increases in rates so far have been inadequate to the task of bringing it back to target.Inflation data is again surprising to the upside, economic growth is rebounding worldwide and labour markets remain very tight. In this context, a 6% handle in terminal rates remains a distinct possibility, and not just in the US. Markets are not taking it well. Bonds and stocks are again falling together, and the dollar is rallying on the back of rising expectations for Federal Reserve rates and its status as a safe-haven. The dollar rallied strongly against all G10 currencies, and most major emerging market ones.This week, attention will be focused on key economic data coming out later in the week, particularly out of the Eurozone. The global PMIs of economic activity will be out on Friday, though this should move little from the preliminary numbers already released. The day before, a critical flash inflation report out of the Eurozone for the month of February. Another upward surprise here may propel market pricing of the Eurozone terminal rate past the 4% level, which we think is still modest considering the task at hand for the ECB. We would expect that to buoy the euro back towards the top of the recent range.Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Sentiment seems so bearish on the pound that it's hard to see who the next seller will be, and there is also some optimism in the air around talks to finalise a Brexit agreement on trade arrangements with Northern Ireland with the European Union. There isn't much on the docket this week in the UK, so expect the pound to trade off events elsewhere.

Sentiment seems so bearish on the pound that it's hard to see who the next seller will be, and there is also some optimism in the air around talks to finalise a Brexit agreement on trade arrangements with Northern Ireland with the European Union. There isn't much on the docket this week in the UK, so expect the pound to trade off events elsewhere. There isn't much on the calendar in the US this week, and markets are focusing on the next critical data point in the week following, the labour market report for February. Therefore, speeches from Federal Reserve officials will be in focus this week. We expect most communications to once again strike a hawkish tone, keeping the door open to at least three more 25bp rate hikes from the FOMC at the next three policy meetings in March, May and June.

There isn't much on the calendar in the US this week, and markets are focusing on the next critical data point in the week following, the labour market report for February. Therefore, speeches from Federal Reserve officials will be in focus this week. We expect most communications to once again strike a hawkish tone, keeping the door open to at least three more 25bp rate hikes from the FOMC at the next three policy meetings in March, May and June.

Markets are currently only pricing in a 25bp move at the next meeting in April, though we suspect that the central bank will place greater emphasis on the inflation implications of the cyclone, rather than growth, and that another 50bp hike is very much on the table.

Markets are currently only pricing in a 25bp move at the next meeting in April, though we suspect that the central bank will place greater emphasis on the inflation implications of the cyclone, rather than growth, and that another 50bp hike is very much on the table.

GBP

Last week’s UK PMIs of business activity provided a strong positive surprise, swinging back squarely towards expansion for the first time in eight months and contradicting directly the recent recession narrative. While sterling lost ground against the US dollar, as did every other G10 currency, it managed to end up near the top of the performance rankings.Figure 2: UK PMIs (2021 - 2023)Sentiment seems so bearish on the pound that it's hard to see who the next seller will be, and there is also some optimism in the air around talks to finalise a Brexit agreement on trade arrangements with Northern Ireland with the European Union. There isn't much on the docket this week in the UK, so expect the pound to trade off events elsewhere.EUR

Data flow out of the Eurozone last week should have put to bed any notions that the European Central Bank is near the end of the hiking cycle. The PMIs of economic activity for February surprised squarely to the upside and effectively ended any possibility of a Eurozone recession, in our view. Further, the inflation report was revised upwards, both in its core and headline components.This week we expect more of the same, with a flash prices report that will show, again, no sign of a downward trend in core inflation. The ECB, as we expected, is flagging increasingly the stickiness of this key inflation sub index as a source of concern and justification for its hawkish rhetoric. We expect this to put a floor under the common currency soon.USD

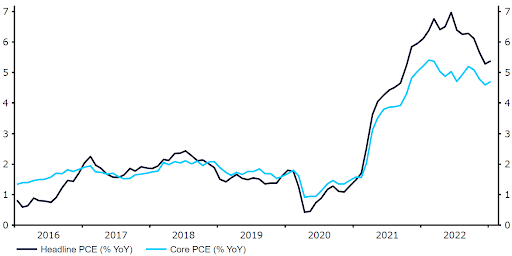

Economic data out of the US confirmed that the economy is still firing on all cylinders. Data on the housing market and business and consumer sentiment all surprised to the upside. More importantly, so did the Federal Reserve's preferred inflation gauge, the PCE index, which has erased any sign of a downward trend and actually appears to be on the rebound.Figure 3: US PCE Index (2016 - 2023)There isn't much on the calendar in the US this week, and markets are focusing on the next critical data point in the week following, the labour market report for February. Therefore, speeches from Federal Reserve officials will be in focus this week. We expect most communications to once again strike a hawkish tone, keeping the door open to at least three more 25bp rate hikes from the FOMC at the next three policy meetings in March, May and June.JPY

The yen was one of the underperformers in the G10 last week. Newly appointed Bank of Japan governor Ueda, who will assume the post in April, struck a rather dovish tone during the Lower House hearings on Friday. There has been intense speculation that the BoJ will begin normalising rates later in the year, though Ueda stressed that policy will remain loose for the time being, while failing to comment on the possibility of higher rates. This lack of a hawkish shift has somewhat alarmed yen bulls, and partly contributed to the recent sell-off in the yen. February inflation data will be released in Japan on Friday, with investors bracing for another fresh multi-dace high in the critical core index.CHF

Despite a good start, the Swiss franc ended last week lower against the euro and underperformed most of its G10 peers. At least part of this underperformance may be due to the widening gap in interest rate expectations between Switzerland and its peers. The market expects higher rates than before, but the extent of recent repricing has been less significant than in the US or the Eurozone.In contrast to the previous rather quiet week, this one promises to be quite interesting in terms of macroeconomic releases from Switzerland. The focus will be on the fourth quarter GDP data (Tuesday) and retail sales and PMI data (Wednesday and Thursday respectively). Solid readings may support the currency, as on the one hand, they could point to a ‘soft landing’, and on the other add the arguments in favour of more aggressive monetary policy tightening.AUD

Risk-sensitive currencies sold off hard against the US dollar last week, led by the Australian dollar in the G10, which sank by around 3%. Last week’s Reserve Bank of Australia meeting minutes were actually rather hawkish. RBA members stressed their view that additional rate hikes would likely be required in the coming months, citing the upside surprises in wages and inflation. The bank even acknowledged that discussions were had on the possibility of a 50bp hike at the last meeting, and that a pause in the tightening cycle was not an option on the table.Investors shrugged off these hawkish remarks in favour of news elsewhere, notably the waning in optimism surrounding China’s economic recovery. Fourth quarter GDP data will be released in Australia on Wednesday, as will the monthly CPI print for January. Upside surprises in either or both of the upcoming growth and inflation readings would reinforce the narrative that the RBA still has some way to go in raising rates, and could provide some respite to the recent move lower in AUD.NZD

The New Zealand dollar held up better than its Australian counterpart last week, in no small part due to the hawkish message from the RBNZ. New Zealand’s central bank raised rates by another 50bps last week, while noting that core inflation remains too high and that near-term inflation expectations were elevated. The bank noted that it was too soon to ascertain the economic implications of the recent cyclone, though the weather disaster is likely to keep price pressures elevated and make it harder to the RBNZ to bring down rates of inflation in a sustainable manner. Figure 4: RBNZ Base Rate [%] (2010 - 2023)Markets are currently only pricing in a 25bp move at the next meeting in April, though we suspect that the central bank will place greater emphasis on the inflation implications of the cyclone, rather than growth, and that another 50bp hike is very much on the table.