Dollar retreat continues amid inflation optimism

( 10min )

- Go back to blog home

- Latest

16 January 2023

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

The US inflation report confirmed the downward trend in price pressures and sent financial markets worldwide soaring on the hope that Fed hikes will soon stop.

This week is relatively light in data. A critical Bank of Japan meeting looms on Wednesday, given hints that the Bank of Japan is ready to ditch its position as a dovish outlier among the major central banks. The key question will be whether the trends in place so far for 2023, i.e. rallying risk assets, diminishing worries about the inflation outlook and a falling dollar, stay in place as markets digest the positive inflation news from last week. Traders’ attention will be focused on the numerous speeches by the world’s central bankers at the Davos economic forum later in the week. We expect diverging content and tone from ECB and Fed speakers, given the developing gap between the trends in core inflation in the Eurozone (still rising) and the US (slowly falling).

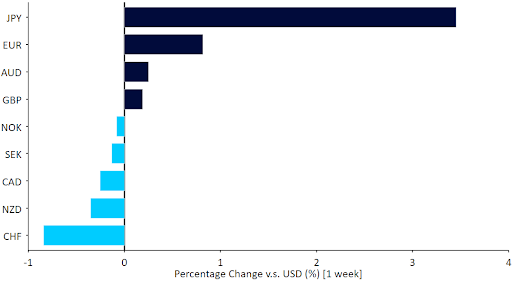

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Source: Refinitiv Datastream Date: 16/01/2023

GBP

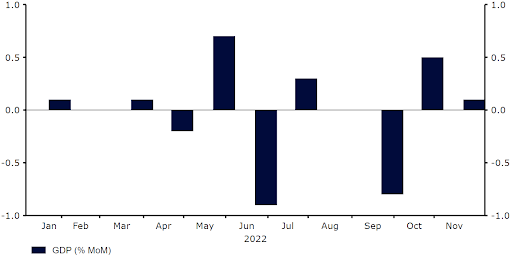

The UK economy continues to outperform gloomy expectations. It managed to eke out 0.1% growth in the month of November, defying expectations for a mild contraction and casting doubt on calls that the UK is already in recession. Sterling did not react much to the news, and it largely tracked the euro in its rally against the dollar.

Figure 2: UK GDP [% MoM] (2021 – 2022)

Source: Refinitiv Datastream Date: 16/01/2023

The UK will provide a couple of the few major data points in the coming week, with the publication of the latest labour report on Tuesday, and the December inflation data on Wednesday. We will be paying particularly close attention to the core index. So far, as is the case in Europe, we have not seen this key indicator exhibit the kind of welcome downward trend we are witnessing in the US.

EUR

The main news of the week out of the Eurozone was the large upward surprise in industrial production for November. While the number is old by now, it makes it quite unlikely that the Eurozone entered recession in the winter of 2022, in line with our views and contrary to the gloomy sentiment. The continued fall in energy prices is further buoying sentiment on the Eurozone economy, and the common currency outperformed every G10 currency last week, save the yen.

We will pay close attention to ECB President Lagarde’s speech at the Davos forum in the coming days. The need for Eurozone rates to catch up with those in the US, and the further upside to the bloc’s economy from China’s reopening, remain the pillars of the bullish case for the euro.

USD

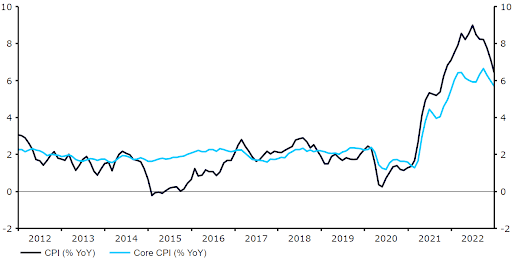

Last week’s US inflation report came in almost exactly as expected, and that was good news for markets. The monthly headline number fell for the first time since May 2020, while the key core inflation index, more persistent and a better predictor of future inflation than the headline, rose by only 0.3%. The latter has been on a clear, albeit gentle, downward path since last summer, though it is still at levels far above the Fed targets.

It now seems likely that overnight rates in the US will not rise above 5% before the Fed adopts a wait and see attitude, with financial markets eyeing two additional 25bp hikes in February and March before the FOMC ends its tightening cycle. That said, we still think that the prospect of rate cuts lies far into the future, certainly not before 2024.

Figure 3: US Inflation Rate (2012 – 2022)

Source: Refinitiv Datastream Date: 16/01/2023

JPY

The yen was by far the best performer in the G10 last week, extending its recent rally and advancing to its strongest position on the US dollar since May. Investors are continuing to favour the yen in light of the hawkish policy shift from the Bank of Japan, which tweaked its yield curve control strategy in December. Speculation is rife that the BoJ could further adjust its YCC policy at its meeting this coming Wednesday. With indicators of both consumer and producer inflation on the rise, we think there is a possibility that it could scap it altogether, which would be a significant bullish signal for the yen. While we don’t expect the BoJ to open the door to raising its base rate just yet, we still see further room to run in the currency from current levels, and go into Wednesday’s meetings seeing risks to the yen as skewed firmly to the upside.

CHF

Last week marked a milestone for the EUR/CHF pair, as it rallied back above the parity level for the first time since July. This can be attributed to an improvement in market optimism, with risk sentiment supported by a further easing in US inflation. Indeed, the Swiss franc was one of the worst performers in the G10 last week. The recent move in the pair is in line with our view and we expect a continued, albeit gradual, depreciation of the franc against the euro in the coming quarters.

Similar to the previous one, this week’s domestic economic calendar is rather light. Instead, we’ll be focusing on central bank communications, notably from Swiss National Bank governor Jordan, who will be speaking at the Davos conference on Friday.

AUD

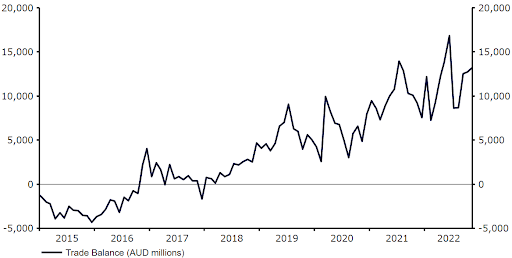

Once again, the Australian dollar was one of the outperformers last week, with the currency continuing to take advantage of China’s reopening – a key stimulus to the Australian economy. Macroeconomic news out last week was also rather encouraging, raising the possibility of additional tightening from the Reserve Bank of Australia, potentially at its next meeting in early-February. November retail sales beat expectations, the trade balance swelled greater into surplus, while inflation data continued to trend higher, with the monthly print rising to 7.3% in November.

Figure 4: Australia Trade Balance (2015 – 2022)

Source: Refinitiv Datastream Date: 16/01/2023

As things stand, markets are torn as to whether the RBA will stand pat or deliver another 25bp hike next month. Upcoming data will be critical in guiding these expectations, starting with Thursday’s labour report for December. An easing in the pace of net job creation is expected, though this number has tended to surprise to the upside in the past few months.

NZD

The New Zealand dollar extended its recent underperformance against its Australian counterpart last week, perhaps partly a consequence of a previous strong rally and the lack of any major domestic developments. The Reserve Bank of New Zealand is expected to be one of, the not the most, active central bank in the G10 this year, but this already appears largely priced into NZD, which is limiting further upside in the currency.

Activity should pick up modestly this week, with business confidence (Monday) and PMI data (Thursday) to be closely watched by market participants. We think that the latter may be particularly important – this key indicator has been on a downward trend for the past few months and a drop below 50 in the composite index isn’t out of the question.

CAD

CAD was one of the underperformers last week, which can perhaps be linked to the currency’s close tie with the US dollar more than anything else. This week looks set to be a far more eventful one. The December inflation report (Tuesday) could be a highly important one for the Canadian dollar. So far, we’ve seen signs of a very gradual downward trend in the headline inflation number, but economists are pencilling in a sharp drop to 6.3%, which would be the lowest level since February.

Of greater importance for CAD will be the core inflation print. The lack of any clear signs that this has peaked could ramp up expectations for another 25bp rate hike from the Bank of Canada at its policy meeting next week (currently 70% priced in). Retail sales on Friday could also be a market mover, although this data is for November so will likely have a limited impact on the USD/CAD exchange rate.

SEK

Inflation data released in Sweden last week confirmed our view that the Riksbank still has some way to go in its fight against inflation. Even off the back of the data, and the general improvement in risk sentiment, the krona failed to benefit and ended the week lower against a broadly stronger euro.

In contrast to other major economic areas, particularly the US, price pressure continues to rise in Sweden. Sweden’s inflation rate increased more than expected to 12.3% in December, its highest rate since 1991. The CPIF, the measure of inflation tracked by the Riksbank, also increased to 10.2%, reaching double digits for the first time in more than thirty years. In our view, an additional 50 basis point rate hike by the Riksbank is warranted in February. This could provide some support for the krona, particularly as most other central banks are slowing their tightening cycles.

NOK

In line with its Swedish counterpart, the Norwegian krone ended the week lower against the euro, with the EUR/NOK pair trading around the 10.7 level. We attribute this modest underperformance to the downward surprise in the Norwegian inflation data for December, released last week. Norway’s inflation rate decreased more than expected to 5.9% in December, its lowest level in seven months. However, the core inflation rate, more important for future monetary policy in our view given it strips out volatile components, increased slightly to 5.8%.

Norges Bank will meet this coming Thursday, and looks likely to again raise rates by another 25 basis points, in its attempt to curb inflation. Markets are pricing a total of only 25bps of hikes for the next two meetings though, in our view, another 25bps rate hike in March cannot be ruled out, given high inflation and the resilience of the domestic economy.

CNY

The Chinese yuan continued rallying last week, rising to its strongest position against the US dollar since July this morning. The move in USD/CNY does, however, appear to be largely a consequence of the weaker US dollar, as the CFETS RMB index ended last week only a tad higher. Last week’s inflation data from China did not rock the boat. As expected, the headline rate ticked up slightly in December, although at 1.8% it remains far below the 3% target and is not expected to reach this level anytime soon. The inflation numbers, including PPI printing in negative territory, continue to point to weak demand.

This week’s economic calendar is packed with data. Tuesday is set to be especially busy as we’ll receive key hard data prints for December and the GDP data for the fourth quarter. Moreover, loan prime rates are set to be announced on Friday. The PBoC kept the rate on its one-year medium-term lending facility (MLF) unchanged today. It also injected 79 billion yuan in fresh loans on top of the 700 billion yuan rollover. The base case is for no change in the loan prime rates (LPRs), albeit a change in the 5-year rate, which serves as a reference for mortgage rates, would not be a major surprise.

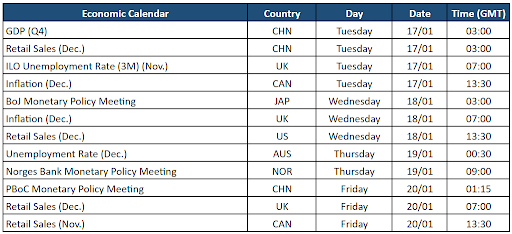

Economic Calendar (16/01/2023 – 20/01/2023)

SHARE