Dollar sell-off continues on US soft data, easing Fed bets

( 3 min )

- Go back to blog home

- Latest

27 May 2022

Matthew Ryan is Ebury’s Global Head of Market Strategy, based in London, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.

The main theme in the FX market this week has continued to be one of a broadly weaker US dollar.

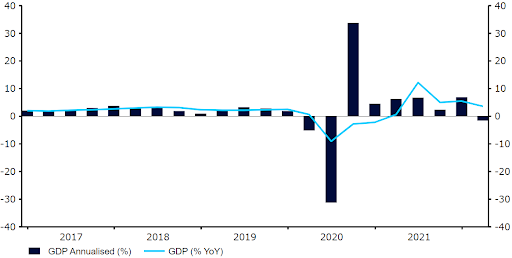

A slight deterioration in US macroeconomic data this week has partly contributed to the easing in market pricing for Fed hikes. Earlier in the week, US new home sales collapsed by 16.6% month-on-month in April to their lowest level since near the start of the pandemic in April 2020 (591,000), in a sign that rising costs have made housing even more unaffordable. Wednesday’s durable goods order data similarly missed its mark (+0.4% in April versus +0.6% consensus), while data yesterday showed that the US economy contracted more than previously believed in the first quarter of the year (1.5% annualised versus the 1.4% initial estimate).

Figure 1: US GDP Growth Annualised (2017 – 2022)

Source: Refinitiv Datastream Date: 26/05/2022

The result has been a sell-off in the dollar against every major currency, and most emerging market ones as well. There has not necessarily been a clear pattern in FX, although the commodity dependent currencies in Latin America continue to outperform, while the likes of the Polish zloty and Czech koruna in Central and Eastern Europe have also rebounded nicely.

The euro and sterling have traded roughly in the middle of the pack of G10 currencies this week. In line with our forecasts, the common currency has rebounded above the 1.07 mark in the past few days, helped by hawkish comments earlier in the week from ECB President Lagarde, who opened the door to 25 basis point rate hikes at the bank’s July and September meetings. Data out of the Eurozone economy this week has been slightly underwhelming, notably the undershoot in the composite PMI for May (54.9 vs. 55.3 expected). The measure did, however, hold up better than those released in both the US (53.8 vs. 55.5), and the UK (51.8 vs. 56.5), and thats provided at latest some reason for optimism over the Euro Area growth outlook.

Sterling has recovered well following the sell-off on Tuesday induced by the dismal PMI figures for May. The collapse in the UK’s services PMI, which fell to just 51.8 this month from the 58.9 reading in March, has raised a few alarm bells. News that UK energy prices are set to increase by another £800 on average in October raised fresh concerns that rising inflation could weigh on UK consumer spending activity in the second half of the year. Investors have, however, reacted positively to the unveiling of the government’s more generous-than-expected support plan on Thursday. The support package includes £15 billion in financial assistance, and a 25% windfall tax on oil and gas producer profits. While this only goes part of the way in alleviating the ongoing cost of living crisis, we are optimistic that the government’s targeted fiscal measures will ease at least some of the downside stemming from the recent boom in inflation. This appears to be supporting sterling, which looks likely to post its second consecutive week of gains against the dollar.

To stay up to date with our publications, please choose one of the below:

📩 Click here to receive the latest market updates

👉 Our LinkedIn page for the latest news

✍️ Our Blog page for other FX market reports

🔊 Stay up to date with our podcast FXTalk

SHARE