Dollar softens as FOMC holds rates; US Presidential Election now in focus

- Go back to blog home

- Latest

26 September 2016

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

The Federal Reserve declined to hike US interest rates last week.

The two major exceptions to the US Dollar sell-off last week the Mexican Peso and Sterling. The former continues to suffer on news that Trump is closing the gap with Clinton in the US Presidential Election polls, whereas the latter sold-off again, somewhat puzzlingly, on little news. The Pound now edges perilously close to a fresh three decade low against the Dollar.

The US Presidential Election finally becomes the focus of currency markets. This week we will see the first of three debates between Hillary Clinton and Donald Trump. With most major central bank meetings out of the way for now, the outcome of the debate and the reaction in currency markets will provide critical information as to the trends that are likely to drive currencies in the weeks leading up to the election in November.

Major currencies in detail:

GBP

In a week almost completely lacking in significant data releases or policy announcements, Sterling continued its somewhat befuddling underperformance against all of its major peers.

Sterling received little help from Bank of England policymaker Kristin Forbes, despite suggesting that she’s unlikely to vote in favour of further economic stimulus at the coming MPC meetings.

This week is likewise very light in terms of new information and we expect Sterling to trade mostly in response to events elsewhere. Nevertheless, we think that the recent sell-off of the Pound is excessive and we wouldn’t be surprised to see a short term rebound.

EUR

Economic news out of the Eurozone was fairly thin on the ground last week, with the Euro largely driven by events in the US.

The preliminary business sentiment PMI’s for September were both fairly underwhelming. The services and manufacturing PMIs both slowed to 52.1 and 52.6 respectively, with the composite index dipping to 52.6 from 52.9. We think this heaps further pressure on the European Central Bank to increase its stimulus programme at its forthcoming meetings.

The key flash Eurozone September inflation release on Friday is the event to watch for the common currency this week.The headline numbers is likely to bounce back from the 0.4% YoY levels of the previous month, on the back of higher energy prices. The more relevant core number, however, is likely to remain at 0.8%, far below ECB targets.

Before Friday, however, we expect the Euro to look to the US Presidential Election post-debate polls for direction.

USD

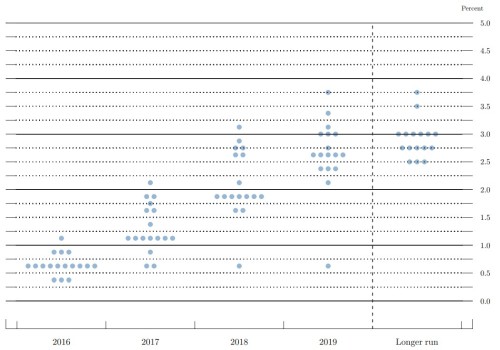

The September FOMC meeting had something for everyone.

Rates were left unchanged but both the statement and Yellen’s press conference both strongly hinted at a December hike, with November left open as a possibility. Also, three out of the ten members dissented in favor of an immediate hike, a very unusual development.

However, the ‘dot plot’ showed yet another fall in FOMC members’ expectations for the long term path of Fed policy rates.

Figure 1: Federal Reserve September ‘Dot Plot’

After an initial hesitation, traders appear to give somewhat more weight to the latter dovish development and the US Dollar traded modestly lower against most major currencies over the rest of the week.

All focus now shifts to the first Presidential debate tonight. In our view, the narrowing of the poll gap by Trump in recent weeks has been somewhat exaggerated by both poll analysts and the media and Hillary Clinton remains by far the favorite to win the election.

In addition to her admittedly narrow lead in the polls, the Electoral College system, whereby the winner of a state captures all of its delegates, slightly favors the Democratic incumbent.

Receive these market updates via email

SHARE