A few years back, we didn't even know that there was an alternative to calling a taxi company, with the person on the other end of the phone saying 'maybe 40 minutes'.

But fast forward to today, you now expect your socks to arrive the same day thanks to Amazon, your taxi arrives in minutes thanks to Uber, and you get cheap instant access to Oscar winners on your couch thanks to Netflix. These are problems you didn't know you had until a great company solved them. It feels like magic.

The same expectation applies to international transfers. Imagine getting a payment from your client, but you need to wait two days each time they pay you. It wouldn't be unfair to call it friction, especially in a digital economy.

So, what is the way out? This brings us to the role of local collections when doing cross-border transactions. In this article, we will decode the significance of local collections when making cross-border transfers. We will cover what this means, how they benefit you, and how Ebury makes international trade easier for our clients through local collection accounts. Let's jump in.

But why do local collections even matter?

Local collections are all about convenience – for you, and for your global customers. With local collections, you can expect cross-border payments to land on the same day without any deductions.

For example, say a Spanish company looking to do business in the UK would traditionally look to do one of the following to collect funds:

- Set up a bank account in the UK - this is time-consuming and often requires a local entity to set up.

- Set up a GBP account in Spain - not many traditional providers offer this service, and even when they do, there will be deductions and delays due to the nature of cross-border wires.

- Ask their client to pay in EUR - then there is a burden on the client to convert, and it will impact how much they are willing to pay.

- Allow the client to pay in GBP - then funds are automatically converted by your traditional provider, who may often charge up to 3%.

None of these options are great and win-win for a Spanish company and their client, and that is where the role of local collection accounts comes into play.

Now, you may ask why should my business collect locally?

Local collections are a gateway to doing business ‘like a local’. Let’s say that when buying your socks online, you tend to buy them from a British store rather than import them from Brazil. The reason for this is convenience. You want them to ship faster and cheaper, you want to pay in the same currency you receive your salary in, and you want to be sure that they don’t get a strange tax put on top of them.

B2B trade is no different. Giving your customers the option to pay via local payment rails gives them a sense of confidence and security. On top of this, you avoid unnecessary deductions that can come with wires.

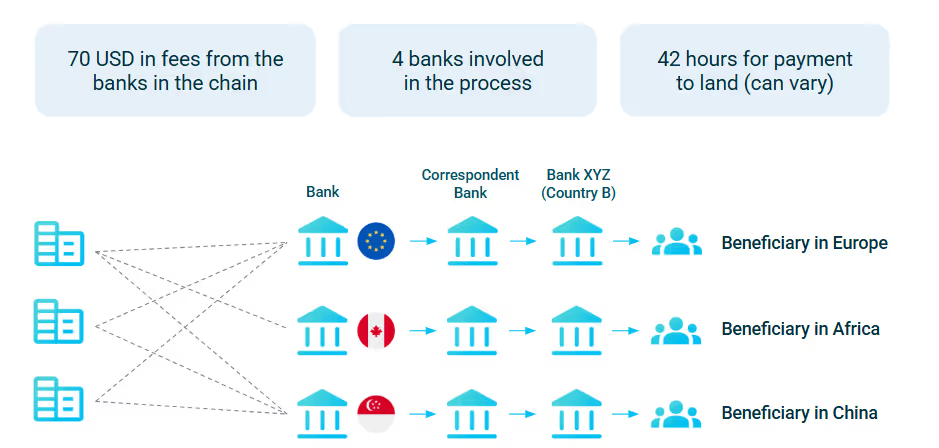

Let’s take a fictional example of a case where a German business sends €485,000 to the USA via traditional wire routing, where 4 financial institutions and $70 are taken out of a transaction that also takes 2 days to arrive.

The challenge here: With the traditional approach, businesses often have to open accounts with different providers for different regional capabilities, leading to high costs, paperwork and friction in the process for both buyers and sellers.

And, there has to be a better way - Enter Ebury's local collection accounts.

Introducing Ebury’s Local Collection Accounts

Ebury has a unique proposition when it comes to local collection accounts, which leads us to two key benefits of our local accounts.

Number 1, with Ebury, you can open one account and get access to your own local collection accounts in 11+ currencies.

With Ebury’s local account, you can access our globally connected, locally embedded network by opening an account with us in just one market. This means reduced costs, and more control over your global transactions.

Secondly, you can reduce the unwanted volatility when dealing in multiple currencies and improve your profit margins with bespoke risk management solutions.

For example, If you are a UK business selling services to a New Zealand business, you are selling your services in USD. This is 'convenient' because USD is easily understood and accepted by you and your client as the currency of global trade. However, if you dig deeper, USD is not useful for you or your client, who pays all their expenses in GBP and NZD, respectively.

Bottom line

With Ebury, you can now send your customers your own local account details in 11+ currencies and receive payments on the same day as any local transfer.

This means zero fees to get paid, no local address or bank account needed – meaning less hassle, less admin cost and more time to focus on your business. Plus, you can minimise your currency risk with our bespoke hedging solutions.

Learn how Ebury's global business account can help you access a world of infinite opportunities >

Disclaimer

- The information provided herein is general in nature and should not be construed as financial or investment advice. The information provided here is not legally binding.

- The information, data or views expressed here is for the exclusive use of the recipient and is subject to changes without any notice. You may ask the support team or your dedicated relationship manager to provide additional information regardingEbury Partners UK Ltd products.

- For more details, please refer to ourlegalandprivacy notice.