Fed cuts rates 50 basis points in emergency response to coronavirus outbreak

- Go back to blog home

- Latest

4 March 2020

Senior Market Analyst at Ebury. Providing expert currency analysis so small and mid-sized businesses can effectively navigate international markets.

As the number of confirmed cases outside of China continues to rise, investors’ attention has turned to what kind of policy response markets can expect from central banks and governments around the world.

While the magnitude of such a move this month was largely priced in by the market, the timing of the rate cut caught the market wrong-footed, given that the FOMC was not due to announce its latest rate decision until after its next scheduled meeting on 18th March. The last time the bank made such an unscheduled rate cut was during the height of the financial crisis in October 2008. This highlights the severity of the risk that the COVID-19 virus poses to the global economy. The Fed is clearly keen to get ahead of the curve and act sooner rather than later in order to protect the US economy.

In an accompanying statement, the central bank noted that the coronavirus poses ‘evolving risks to economic activity’, stating that additional stimulus was required in order to achieve the bank’s goals of maximum employment and price stability. FOMC Chair Jerome Powell’s press conference following the announcement was relatively brief, although he did voice confidence that the cut would provide a meaningful boost to the economy. He also stated that the bank would continue to use all its available tools, a nod to additional Fed cuts down the line, and that formal coordination from G7 monetary authorities was possible.

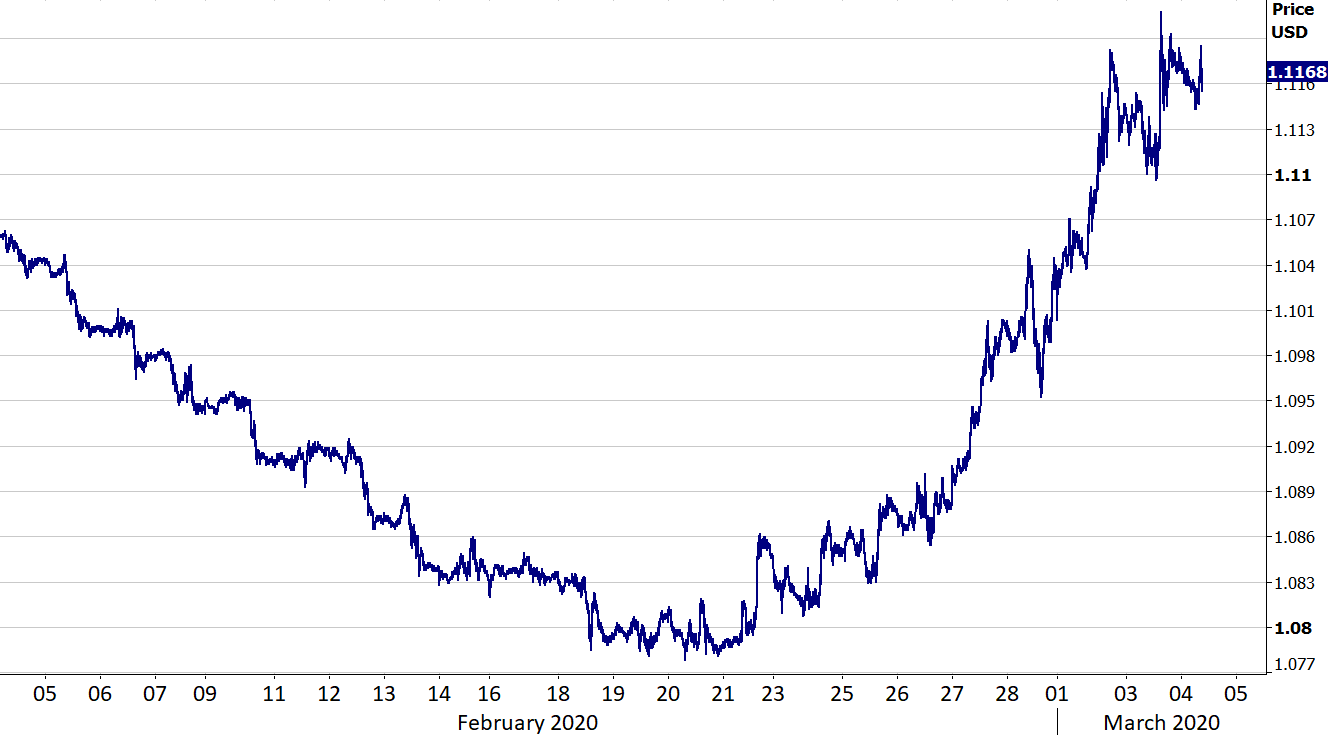

Unsurprisingly, the dollar fell across the board in the immediate aftermath of the surprise announcement. EUR/USD briefly rose back above the 1.12 level (Figure 1), although the move was relatively minor and indeed the euro retraced much of its gains soon after. Against the pound, the dollar was barely changed, with the moves in the FX market on the whole relatively contained. We think that this is, in part, due to the already high expectations for Fed stimulus prior to the announcement.

Figure 1: EUR/USD (February ‘20 – March ‘20)

The reaction in equity markets tells a story in itself. Stocks initially staged a relief rally, although by the end of the New York session the Dow Jones index was trading around 800 points lower, approximately 3% (Figure 2). The real concern for the market is that monetary easing can only partly aid to soften the economic blow caused by the virus, and can do nothing to solve the health crisis itself – central banks can’t print a vaccine. While it may help boost consumer demand, it’s likely that the rate cut will have very little effect on the supply-shock triggered by the virus. Recent data has shown that US companies are already beginning to run out of goods sourced from China, a direct consequence of the widespread shutdowns in Asia’s largest economy. Lower interest rates will do very little to solve this. Instead of assuring investors, all that the rate cut has done, both its magnitude and indeed timing, is highlight to investors the extent of the Federal Reserve’s concern.

Figure 2: S&P 500 and Dow Jones Index (January ‘20 – March ‘20)

We think that the Fed’s rate cut, and indeed the statement released by G7 central bankers and finance ministers, is a precursor to more stimulus from other major central banks around the world. The Reserve Bank of Australia (RBA) has already cut rates, lowering its benchmark policy rate by 25 basis points on Tuesday, while hinting at the possibility of more. We now expect the Bank of Canada to ease policy on Wednesday, with a rate cut there all but certain if market pricing is anything to go by. We think that the Bank of England will follow suit when it next meets on 26th March.

The European Central Bank (ECB) is also set to meet next Thursday. We think that a 10 basis point cut in the bank’s deposit rate is now highly likely, with increased loans as part of its TLTRO programme and a ramping up in its quantitative easing programme also possible. The issue for the ECB is that with Euro Area rates already in negative territory, there is very little room for manoeuvre. This goes back to our long-held view that there is simply more room for policymakers at the Federal Reserve, and indeed most other G10 central banks, to cut interest rates than there is at the ECB.

The G7 statement also makes it clear to us that governments around the world are standing ready to ramp up spending should the uncertainty translate into a significant slowdown in global growth. This does, of course, include Germany, which has long resisted calls for a fiscal response in the face of weak European growth. The lack of room for ECB cuts, combined with the growing likelihood of more Fed cuts and some much needed fiscal stimulus from the German government, should be supportive of our view for a stronger euro this year.

Enrique Diaz-Alvarez, our Chief Risk Officer, has been collaborating with Bloomberg since 2012 and thanks to him and our Market Analysts, Ebury has ranked as #1 USD/CNY forecaster on Bloomberg in the first quarter of last year and as #2 in the second quarter. Yesterday he joined Bloomberg Daybreak Asia radio programme to speak on how coronavirus and Fed cuts are affecting the currency markets.

SHARE