Federal Reserve unveils historic monetary policy overhaul

( 2 min )

- Go back to blog home

- Latest

28 August 2020

Matthew Ryan is Ebury’s Global Head of Market Strategy, based in London, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.

The big headline out of financial markets on Thursday undoubtedly came from chair of the Federal Reserve Jerome Powell, who unveiled a very significant shift in the central bank’s policy strategy.

This shift marks one of the biggest changes in the Fed’s policy framework in a number of decades. But what impact will this have on the bank’s monetary policy and the FX market? Historically, when inflation has exceeded the bank’s 2% target, it has generally been followed by a shift to a less accommodative policy – i.e. higher US interest rates. Yet, with the Fed now willing to look through short-term increases in inflation, this is a signal to the market that ultra-low interest rates are here to stay for the foreseeable future and certainly longer than they would have been under the old strategy.

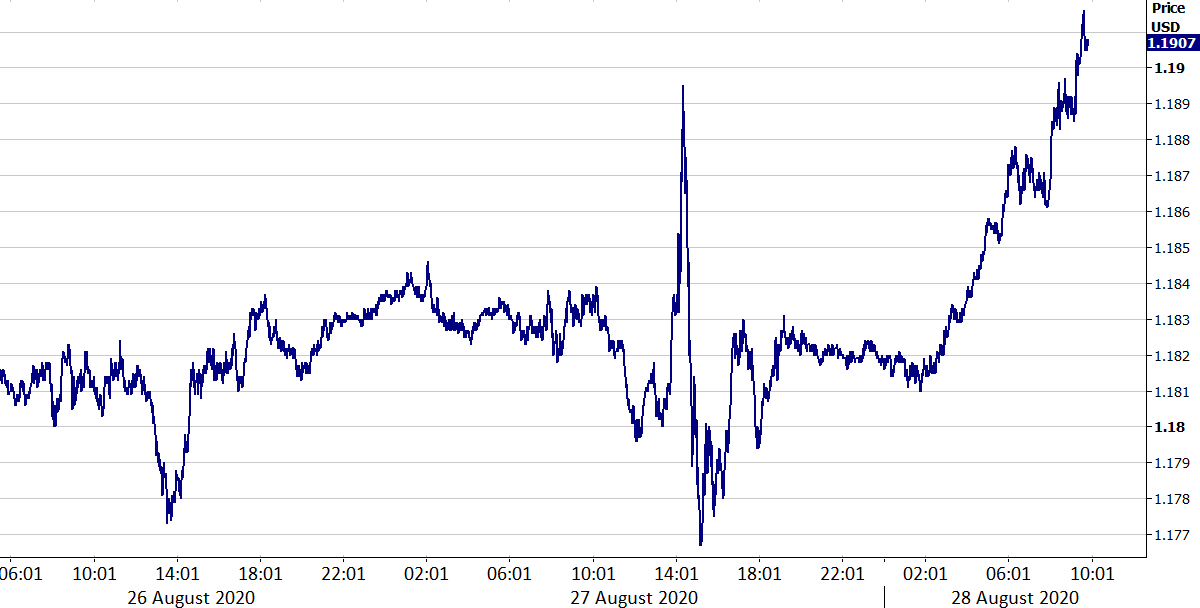

As for the market reaction, stocks unsurprisingly rallied on the prospect of lower rates for longer – the S&P 500 index rose by over one percent for the day. The reaction in the dollar was a more complex one. The dollar initially begun to sell-off before almost immediately regaining its losses.

Figure 1: EUR/USD (26/08 – 29/08)

Source: Refinitiv Datastream Date: 28/08/2020

We think that the immediate U-turn in the dollar following Powell’s statement can be largely attributed to the fact that the announcement was mostly priced in by the market. The promise of ample policy accomodation is also good news for the US economy, while higher asset prices should help entice foreign investors. Longer-term we do, however, think that this is a US dollar negative, particularly should we start seeing other major central banks signal higher rates are on the horizon long before the Federal Reserve. This, we think, has been reflected in the dollar this morning, which has begun selling off again versus its major peers as investors continue to digest yesterday’s announcement.

So the big question is, has this change in strategy been triggered by the COVID-19 pandemic? According to Powell, the announcement is a reflection of both a slowdown in US growth and the diminishing chances of high inflation, which has continuously undershot its target for a number of years. So while this change was likely inevitable anyway, the pandemic would no doubt have sped things along, given the impact it has had on suppressing both growth and inflation. The greater emphasis on supporting the labour market will be a particularly welcome development for those millions of Americans that remain without work due to the ongoing shutdown measures.

SHARE