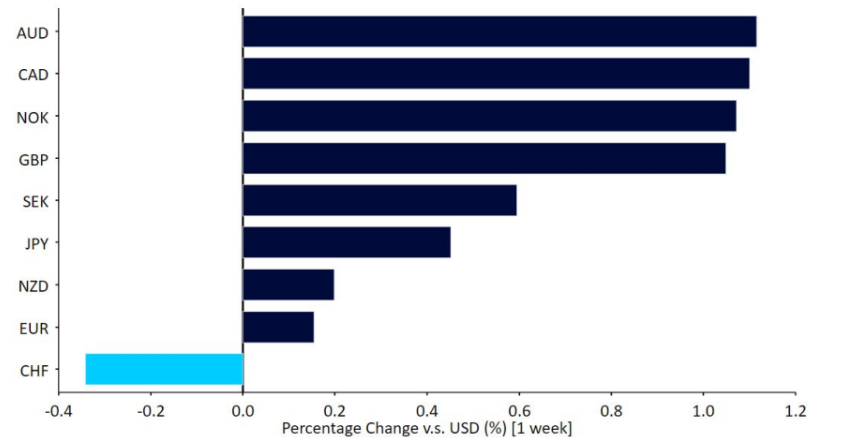

While the euro, dollar and sterling fail to move much against one another, emerging market currencies once again took the spotlight last week.

Latin American currencies in particular built further on their torrid performance so far in 2023, buoyed by the return of risk appetite to financial markets, which is lifting risky assets generally. News over the weekend that Saudi Arabia plans to cut oil production should be expected to reinforce the positive trend in commodity prices and provide further support for commodity currencies. The losers of the week were the Swiss franc, as appetite for safe-havens diminishes, and the Turkish lira, which is spiralling down in response to Erdogan's electoral triumph and the fading prospects for a return to financial sanity.

This week will be unusually quiet, with little macroeconomic or policy news likely to move markets in any of the major economic areas. A handful of speeches by central bank officials will provide some focus for traders. The most important of these will be ECB President Lagarde and FOMC voting member Mester.

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

GBP

The nasty CPI surprise from two weeks ago continues to support sterling, as Bank of England rate expectations get ratcheted up. Swap markets are now pricing in almost 100bps of additional UK rate hikes in 2023, with investors not eyeing a first rate cut until May next year. Concerns over the state of Britain’s housing market continue to linger in the background (house prices are now falling at their fastest annual rate since the Global Financial Crisis according to Nationwide), although fears over entrenched inflation are dominant.

This upward trend in the pound is particularly strong against the euro, as sterling broke to fresh year highs last week against the common currency. With little market moving news or central banker speeches on tap this week, sterling should mostly trade off news elsewhere.

EUR

Preliminary inflation numbers for May in the Eurozone contain the first significant piece of good news on this front in many months. Both the headline number and the core subindex fell considerably more than expected. The key core number fell from 5.6% to 5.3% on the year, the first significant pullback from record highs, and rose by only 0.2% on the month, well below the +0.8% expected.

With rates at 3.25%, far below core, the ECB still has plenty of work to do, and inflation levels in the Eurozone remain unacceptably high, albeit it seems like there is at least light at the end of the tunnel. The euro shrugged off the number and the consequent drop in ECB rate expectations, in a sign that the common currency may be nearing some sort of a bottom.

USD

The May payrolls report out of the US was strong in all the right ways. Job creation continues to run high and the US remains at full employment. ANother 339k net jobs were added to the US nonfarm sector last month, once again above expectations - the fourteenth consecutive month that the preliminary estimate has beaten economists’ estimates. This strength is drawing workers into the labour pool, however, and wage gains seem to be slowly moderating.

At the margin, this report reduces the pressure on the Fed to hike again at its June meeting, which is now only roughly 30% priced in by futures markets, though a bad inflation number next week would upend all expectations again. However, expectations of cuts continue to recede into the future. All in all, the Fed seems to be closer to achieving the immaculate soft landing than it seemed just a few weeks back.

JPY

The yen broke back above the 140 level on the dollar late-last week, despite verbal intervention in the market from Japan’s vice Finance Minister earlier in the week. Speaking on Tuesday, Masato Kanda noted that authorities in Japan will ‘closely watch currency market moves and respond appropriately as needed’. With the yen trading just shy of its lowest level since November, we suspect that authorities may well dip into the FX reserves pool should we see a move towards the 145 level in USD/JPY, as this could bide time before the BoJ is forced to raise rates. Following some disappointing data on April industrial production and retail sales last week, markets now only see a 25% chance that the bank hikes by its September meeting. Revised Q1 GDP data (Thursday) is unlikely to shift these expectations, so the yen may take its cue from news elsewhere.

CNY

USD/CNY rose through the 7.1 level last week, and the yuan was one of the worst-performing currencies that we cover during that period. Concerns surrounding China’s economic recovery remained front and centre, particularly given another disappointing PMI print from NBS. The Caixin PMI data, both the manufacturing index released on Thursday and today’s services index did, however, turn out better than expected. Both increased relative to the previous month, with the manufacturing PMI unexpectedly moved back into expansionary territory. This breaks the pattern of weak publications we have witnessed in recent weeks, and may help calm market nerves about the recovery.

So far, however, the yuan has not benefited prominently, as the USD/CNY pair has begun the week rising back above the 7.1 level, after a temporary respite on Friday. We will likely need more than one-off releases for investors’ pessimism about China to subside. This week, investors will focus primarily on Chinese trade (Tuesday) and inflation data (Thursday) for May. Price pressures are set to remain effectively absent and PPI inflation is expected to deepen its decline into negative territory.

To stay up to date with our publications, please choose one of the below:

📩 Click

here to receive the latest market updates

👉 Our

LinkedIn page for the latest news

✍️ Our

Blog page for other FX market reports

🔊

Stay up to date with our podcast FXTalk