Latin American currencies rally in spite stock sell off

( 5 min )

- Go back to blog home

- Latest

23 May 2022

Matthew Ryan is Ebury’s Global Head of Market Strategy, based in London, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.

Last week saw some strange market action. Financial headlines were dominated by the relentless sell-off in world equity markets that left the S&P 500 index flirting with the semi-official bear market line of 20% below its record high.

This week the focus will be on any spillovers from the volatility in stock markets to the FX market, on one hand, and the PMIs of business activity on the other. The Eurozone and UK indices are all expected to print well above 55.nWe think that these levels belie the fears of recession that appear to be gripping asset markets. It is difficult to reconcile still massively negative real rates, huge government deficits and economies at full employment with any sustained economic pullback.

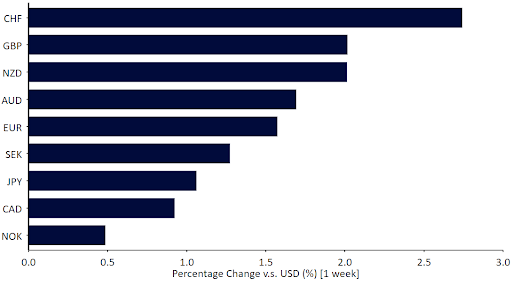

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Source: Refinitiv Datastream Date: 23/05/2022

GBP

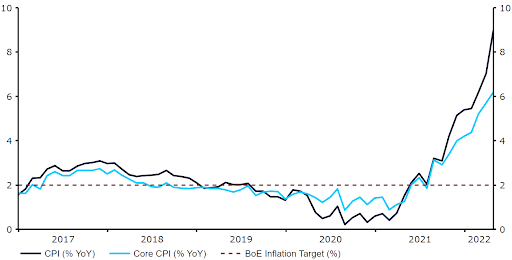

Data out of the UK continued to suggest a dichotomy between sentiment and reality. Consumer sentiment was dismal, but jobs data came out very strong, as did retail sales. Inflation in April was sky high, as expected. Sterling bounced back in line with the general dollar selloff and managed some gains against the euro as well.

We think there is little to suggest a recession is likely, and this week’s PMI data should be further evidence. It seems that the Bank of England’s apparent willingness to tolerate inflation due to the risks to growth is misplaced. In the short-term, Bank of England dovishness may weigh on the pound, but after the recent sell-off we think that the currency is quite cheap and offers a solid opportunity over the longer term.

Figure 2: UK Inflation Rate (2017 – 2022)

Source: Refinitiv Datastream Date: 23/05/2022

EUR

The retreat of the ECB doves in the face of inflationary reality accelerated last week, as the hawkish Dutch member of the council suggested that not only is a July hike a near certainty, but a 50 bp hike could be on the cards. This is happening at the same time US short term rates are having trouble pushing higher, partially because so much is priced in on the part of the Federal Reserve. As a result, interest rate differentials across the Atlantic have shrunk and are no higher now than in March. This trend should be supportive for the euro and we may have already seen the bottom.

This week’s PMIs should be strong and partially assuage recession fears in the US, enabling the ECB to continue its policy turnaround and focus squarely on containing inflation.

USD

Strong retail sales last week confirmed that so far there is little sign that higher prices are doing much to deter the US consumer. However, it is a volatile indicator and one cannot extract a lot of information from a single print. US yields fell in sympathy with stocks, and for now the US dollar seems to have recoupled to rate differentials with the rest of the world, so it fell as well.

On tap for this week is the publication of the minutes for the last meeting of the Federal Reserve, which we expect to reiterate that the next two hikes are likely to be “doubles”, i.e., 50 bp. However, all of this is already priced in by markets, and it will be difficult for US short term rates to price in any more. We think the dollar is vulnerable to a sustained pullback here.

CHF

The Swiss franc outperformed all other G10 currencies by a significant margin last week, rallying by close to 3% against the US dollar on growing speculation about monetary policy tightening in Switzerland.

SNB president Jordan suggested on Wednesday that the bank was ready to act should an inflation threat materialise. Investors might have been further encouraged to bet on a shift in the SNB’s approach by a hawkish ECB, which looks ready to kick-start its rate hike cycle in July. We think that the market is perhaps a bit too aggressive, and think that the SNB would likely prefer to increase currency interventions in the near-term, before thinking about rate increases. While interventions have been relatively limited, suggesting a degree of acceptance of the currency’s strength in light of elevated inflation, the bank still seems determined to not allow the franc to appreciate too much.

We believe the scale of the franc’s recent rally has been excessive and think it may give up some of its gains, particularly if global sentiment improves. That will be the focus for the franc this week, namely the PMI prints from the main economies, news from China, and behaviour of global equity and bond markets.

AUD

A broadly weaker US dollar, the easing of restrictions in China and expectations of a more rapid pace of tightening by the RBA boosted the Australian currency last week. The Australian dollar was one of the best performing currencies in the G10, briefly rallying through the 0.71 level against the US dollar this morning.

The Reserve Bank of Australia’s May meeting minutes showed that the board is prepared to raise rates by larger increments at upcoming meetings in order to tame inflation. The minutes also showed that inflation is expected to increase further in the near-term, which has raised expectations in favour of more aggressive tightening. The latest economic data supports these expectations, with Australia’s unemployment rate falling to 3.9% in April, the lowest since August 1974.

The most important event for AUD this week will likely be the release of the May preliminary PMIs on Tuesday, which are expected to remain in expansionary territory. On Friday, April retail sales will be published.

CAD

The Canadian dollar ended the week modestly higher against the US dollar as Canadian inflation reached a three-decade high, although the currency underperformed most of its G10 peers.

Canada’s April inflation surprised to the upside, reaching a 31-year high of 6.8%. The rise in commodity prices, mainly due to the war between Russia and Ukraine, continues to pressure inflation higher. But this is not the only reason and it seems that price pressure is spreading to more components, as core inflation rose to a record high of 5.8%. This data reinforced expectations of another 50 basis point hike at the Bank of Canada’s June meeting, which has continued to provide a bit of support for the Canadian dollar.

On Thursday, March retail sales will be published. Aside from that, CAD is likely to be driven by events elsewhere.

CNY

Last week was a turning point for the yuan, with the USD/CNY pair returning to early-May levels amid a weaker US dollar and improving headlines out of China. News on the Covid front has taken a turn for the better. Shanghai has begun lifting some of its restrictions, with the city set to exit lockdown at the start of next month. Beijing has also continued to resist calls for a lockdown, despite another increase in virus caseloads.

Last week’s 15 basis point cut to the PBoC’s 5-year loan prime rate, a reference rate for mortgages, has also raised hopes of an economic revival. The scale of the rate adjustment was larger than expected, and suggests China is serious in its efforts to support the struggling housing sector. Sentiment toward China received an additional boost from President Biden’s suggestions that the US may lift some of the Trump-era tariffs. The noises in that regard have been getting louder in the past few weeks, but the decision itself is not an easy one considering the geopolitical landscape in Asia and doubts about benefits to Americans from such a change.

This week we’ll focus primarily on news from China’s Covid front as well as any headlines from president Biden’s trip to Asia, a first since he took office.

To stay up to date with our publications, please choose one of the below:

📩 Click here to receive the latest market updates

👉 Our LinkedIn page for the latest news

✍️ Our Blog page for other FX market reports

SHARE