Shrinking GDP, non-committal Fed sink the US dollar

- Go back to blog home

- Latest

1 August 2022

Chief Risk Officer at Ebury. Committed to mitigating FX risk through tailored strategies, detailed market insight, and FXFC forecasting for Bloomberg.

The US economy now meets the barest technical definition of a recession, and Federal Reserve hikes are now fully dependent on inflation and labour data meeting to meeting.

Now that both the Federal Reserve and the ECB have effectively removed forward guidance, central bank hikes are more data dependent than ever. Therefore, focus will be on Friday’s labour report out of the US. So far, the jobs market there has remained remarkably resilient to the economic slowdown. The Bank of England meeting on Thursday is expected to deliver a 50 basis point rate increase, and it too is likely to downgrade or remove altogether any explicit forward guidance on rates.

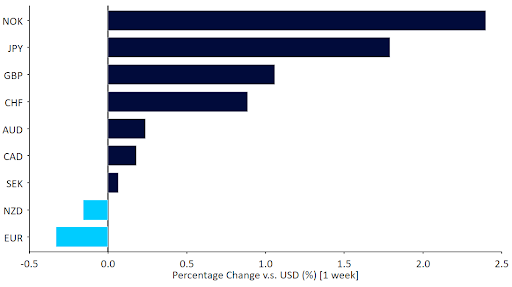

Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

Source: Refinitiv Datastream Date: 01/08/2022

GBP

Sterling continues to move mostly in line with risk assets, and last week’s stock rally buoyed it to the top of the G10 rankings, well ahead of both the dollar and the euro. The Bank of England meeting on Thursday is now front and centre for the pound. As of Friday close, interest rate markets were largely, though not fully, pricing in a 50 basis point move, with some investors betting on a 25bp hike. Therefore, it is a solid bet that Thursday trading will be volatile.

We think it will be difficult for the MPC to buck the hawkish trend among G10 central banks and expect the larger move, with a consequent rally in sterling as a side effect. This rally may, however, be dependent on the voting pattern among policymakers, and the tone of communications in the bank’s latest Inflation Report.

EUR

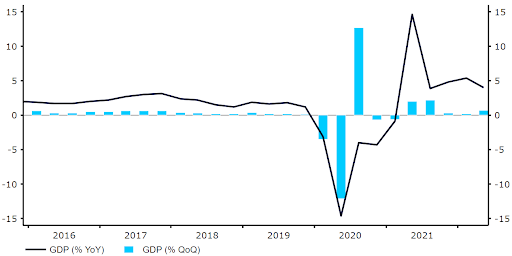

Eurozone inflation once again surprised to the upside, validating our view that ECB interest rate hikes have considerably further to go than interest rate markets seem willing to accept so far. However, the inflation print was overshadowed by the continued reductions in gas flow from Russia, and the announcement of various measures to reduce demand, which understandably are not viewed as euro-positive. Markets mostly overlooked last week’s GDP data, which posted larger-than-expected expansion, in favour of the doom and gloom energy headlines.

Figure 2: Euro Area GDP Growth Rate (2016 – 2022)

Source: Refinitiv Datastream Date: 01/08/2022

This will be a holiday week with limited newsflow, but expect traders to focus on the ECB economic bulletin on Thursday for further clarity regarding the central banks’ plans for further hikes.

USD

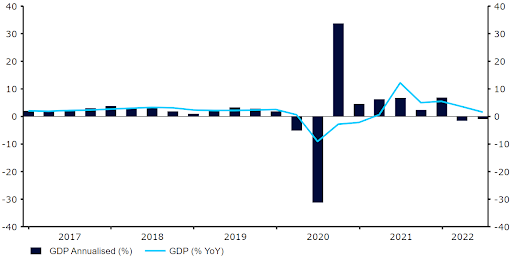

While it is true that the US economy has printed a slight contraction in two consecutive quarters, we would not call the current economic backdrop recessionary. The unusual combination of stalling growth, full employment and very high inflationary pressures prompted the Fed to de facto withdraw all forward guidance at its meeting on Wednesday, and announce that further moves will be data dependent. Friday wage and inflation data showed no sign that inflation is pulling back to desirable levels, and the high ECI employment cost index data bore increasing hints of a developing wage-price spiral. All in all, we think that market expectations of Fed rates peaking just under 3.25% are too optimistic.

Figure 3: US GDP Growth Rate [annualised] (2017 – 2022)

Source: Refinitiv Datastream Date: 01/08/2022

Markets now turn to Friday’s non-farm payrolls report out of the US, expected to show yet another month of healthy job gains in a context of full employment. We will be paying close attention to the wage numbers for confirmation of the above-mentioned feedback between higher prices and higher wages.

CHF

The Swiss franc continued its rally against the euro last week, with the EUR/CHF pair declining to 0.97 – its lowest level since January 2015. Last week’s sentiment data from Switzerland was mixed, although was far from optimistic, as is now generally the case in Europe.

This week we’ll focus on Swiss inflation data, out on Wednesday. Uncertainty about the print is high, particularly after recent surprises in the main economies. With regard to the SNB, we’re increasingly more focused on sight deposits data, as developments there should indicate how comfortable the central bank is with a stronger currency. Due to today’s bank holiday, this week’s numbers will be out tomorrow.

AUD

A combination of worsening headlines out of China and expectations for higher central bank interest rates led to a mixed performance of the Australian dollar last week, though it has managed to post decent gains against the broadly weaker USD. Inflation data came in slightly weaker than expected, but still rose to a more than two decade high 6.1% in Q2 (from 5.1%).

The Reserve Bank of Australia will be meeting on Tuesday, with investors overwhelmingly expecting another 50 basis point interest rate hike, which would be the fourth consecutive rate increase. Swap markets are mostly, but not fully, pricing in a half a percentage point hike, so there is a bit of room for additional upside in AUD in the event of a 50bp hike – we think that a 75bp one is unlikely. Beyond the hike itself, focus will be on the likely pace of future rate increases, particularly in light of heightened global recession concerns. There is a possibility that the RBA could indicate a return to ‘standard’ 25 bp moves from September, which would be a clear bearish signal for AUD. That said, we instead think that the RBA will keep its options open and not pre-commit to the magnitude of additional hikes, which could lead to a relatively quiet response in the FX market.

CAD

The Canadian dollar underperformed most of its major peers last week, barring the US dollar and euro. While there wasn’t necessarily one clear catalyst for this underperformance, CAD is trading at rather elevated levels relative to most currencies, so is perhaps due a bit of a retracement. Macroeconomic news out of Canada last week was actually encouraging, with the May GDP print showing flat growth after economists had braced for a modest contraction.

With more than a month until the next Bank of Canada meeting in September, markets will have plenty of data releases to digest in the meantime, which could sway expectations for the magnitude of the next hike. That begins with Friday’s labour report for July. Following the shock contraction in jobs in the last report, we are expecting a solid rebound in employment creation this time around, although economists don’t anticipate a complete recoup of the jobs shed in June. A modest uptick in the unemployment rate is also expected.

CNY

The Chinese yuan ended last week little changed against the US dollar, despite a broad weakening of the latter. Recent weeks have brought a number of worrisome headlines from China, from the pandemic, through real estate sector issues and rising tensions with the US over Taiwan.

Now the focus turns to economic data, as the business activity readings for the third quarter released so far have surprised to the downside. A weak spot is the manufacturing sector, with the official PMI data showing an unexpected decline to 49.0 in July from 50.2, indicating a contraction in activity. The Caixin PMI also disappointed, with the index hovering barely above the key level of 50 (50.4). This suggests that China’s economic recovery may be more subdued than hoped in Q3. The future path of business activity is likely to depend on global demand and China’s covid situation, as a worsening of both seems to be behind recent weakness in the data. The latest data suggests that this year’s GDP target of ‘around 5.5%’ is almost certain to be missed.

To stay up to date with our publications, please choose one of the below:

📩 Click here to receive the latest market updates

👉 Our LinkedIn page for the latest news

✍️ Our Blog page for other FX market reports

SHARE