Trump’s White House return buoys markets

( 3 min )

- Go back to blog home

- Latest

6 October 2020

Matthew Ryan is Ebury’s Global Head of Market Strategy, based in London, where he has been part of the strategy team since 2014. He provides fundamental FX analysis for a wide range of G10 and emerging market currencies.

Optimism surrounding the possibility of more fiscal stimulus in the US lifted risk assets on Monday, while sending the safe-havens lower, including the dollar.

News that President Trump had left hospital yesterday also buoyed the markets, with investors relieved that he has been spared a more prolonged battle with the virus that would have kept him out of action for longer. Trump’s illness couldn’t have come at a much worse time for the President, with less than a month to go until Americans go to the polls in this year’s election. This disruption in the Republican campaign trail has been reflected in both a widening in the recent opinion polls and a narrowing in the bookmaker odds for a Biden victory. Not only would a comfortable Biden victory increase the chances of more US stimulus, but it would also lessen the possibility of a contested election – an outcome that we believe is the biggest risk to the market going into next month’s vote.

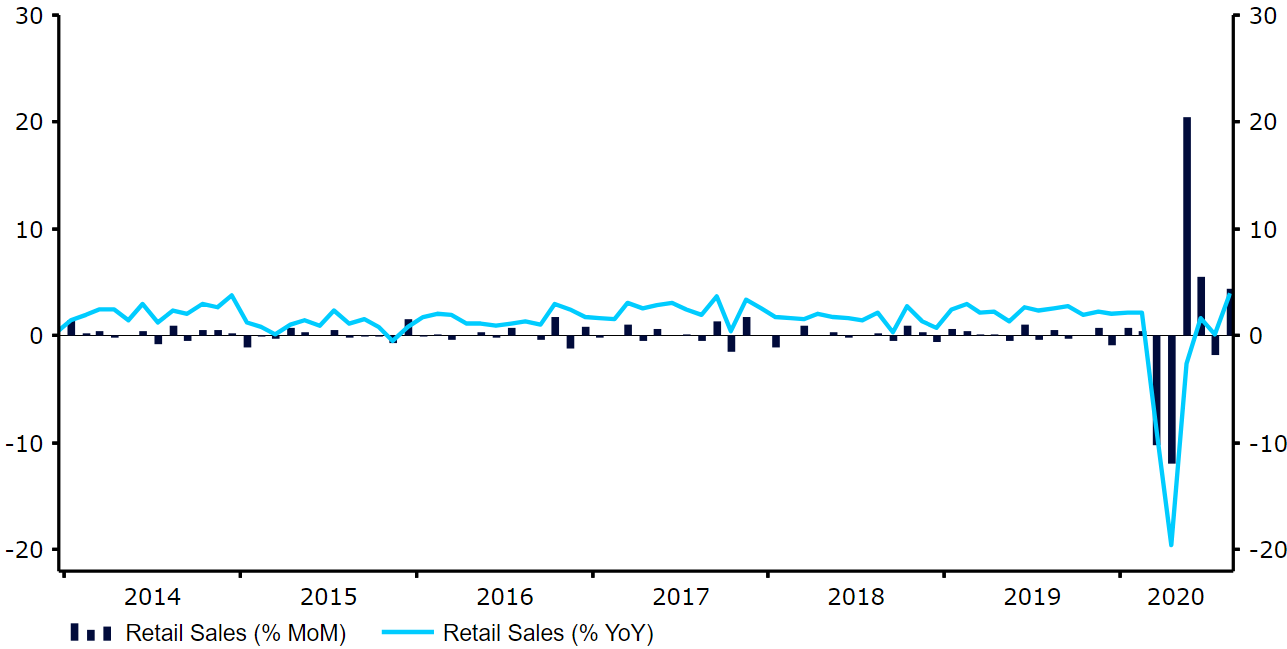

Euro Area retail sales post surprise expansion in August

Higher risk currencies have been well supported in the past 24 hours. EUR/USD jumped to just shy of the 1.18 level this morning, having opened trading yesterday only just above 1.17.

The common currency was also supported by upward revisions to the latest business activity PMIs and a robust set of retail sales data for August. Both the services and composite PMIs were revised upwards for September. The latter remains in expansionary territory at 50.4, helped largely by the jump in manufacturing activity, the index of which is now at its highest level since 2018. Retail sales also significantly surprised to the upside, dashing some concerns that the recovery in the bloc’s economy may be losing steam. Sales rose by 4.4% month-on-month in August, bouncing back well from July’s contraction amid a continued easing in coronavirus restrictions.

Figure 1: Euro Area Retail Sales (2014 – 2020)

Source: Refinitiv Datastream Date: 06/10/2020

Attention in the Eurozone for the rest of this week will be squarely on the ECB. President Lagarde is scheduled to speak both today and tomorrow, with fellow members Mersch and de Guindos also down to make public appearances. Investors will also likely be paying close attention to Thursday’s ECB meeting accounts, particularly for any comments regarding the bank’s view on the lack of inflationary pressure evident in the bloc.

Pound rallies on Brexit optimism, fading negative rate chances

Sterling also rallied yesterday, in line with almost every other risk asset. Investors are largely overlooking the latest COVID numbers around the world at the moment, with the UK reporting a record of more than 12.5k new cases yesterday. This lack of concern among investors is perhaps in part due to the much greater levels of testing conducted compared to the peak of the crisis and the lack of uptrend so far witnessed in new deaths.

The pound has instead been supported by both heightened Brexit optimism and dimming chances of negative Bank of England interest rates. The UK looks much more likely to strike a deal with the EU now that talks have been extended for a month, with the lack of consensus within the MPC causing the market to push back expectations for sub-zero rates deeper into 2021. BoE governor Bailey’s speech on Thursday could be an important one, with markets keen to hear his latest view on the potential effectiveness of negative base rates.

SHARE