14 December 2022

We see a great deal of uncertainty surrounding this Thursday’s highly-anticipated Bank of England meeting, which is likely to lead to heightened volatility in the pound either side of the decision. The MPC is overwhelmingly expected to raise its base rate for the ninth consecutive meeting this week, as it continues its quest to suppress UK inflationary pressures. We are pencilling in another 50bp hike, although we suspect that the decision on the magnitude of the rate increase will be far from unanimous. At its most recent meeting in November, rates were raised by 75 basis points, in line with expectations and the largest hike in more than three decades. There was, however, a three-way split among the MPC, with two of the nine members in favour of smaller increment moves (one for 25, the other 50).  We view the ‘jumbo’ interest rate hike in November as a one-off, and a move largely in reaction to the market turmoil caused by Liz Truss’ fateful mini-budget announcement. We’ve continued to see a range of views among MPC members as to the pace of tightening, and we cannot rule out another three-, or even four-way, voting split among the committee at this month’s meeting. The BoE has a very delicate balancing act to contend with. On the one hand, UK inflation has continued to break to fresh four decade highs above 11%. On the other, there remains an acute degree of uncertainty surrounding the economic outlook, with the MPC warning in November that the longest UK recession on record was on the way.While we believe that a 50bp hike is highly likely on Thursday, we acknowledge that this is not necessarily guaranteed. Swap markets are fully pricing in a half a percentage point move with a non-negligible possibility of a 75bp hike (almost one-in-three). We even think that some of the doves will vote in favour of a ‘standard’ 25bp move, with a possibility that one or two could side in support of no change. We have outlined below the arguments in favour of both a smaller and larger increment rate hike this week, and our view of how each MPC member could vote.

We view the ‘jumbo’ interest rate hike in November as a one-off, and a move largely in reaction to the market turmoil caused by Liz Truss’ fateful mini-budget announcement. We’ve continued to see a range of views among MPC members as to the pace of tightening, and we cannot rule out another three-, or even four-way, voting split among the committee at this month’s meeting. The BoE has a very delicate balancing act to contend with. On the one hand, UK inflation has continued to break to fresh four decade highs above 11%. On the other, there remains an acute degree of uncertainty surrounding the economic outlook, with the MPC warning in November that the longest UK recession on record was on the way.While we believe that a 50bp hike is highly likely on Thursday, we acknowledge that this is not necessarily guaranteed. Swap markets are fully pricing in a half a percentage point move with a non-negligible possibility of a 75bp hike (almost one-in-three). We even think that some of the doves will vote in favour of a ‘standard’ 25bp move, with a possibility that one or two could side in support of no change. We have outlined below the arguments in favour of both a smaller and larger increment rate hike this week, and our view of how each MPC member could vote.

We view the ‘jumbo’ interest rate hike in November as a one-off, and a move largely in reaction to the market turmoil caused by Liz Truss’ fateful mini-budget announcement. We’ve continued to see a range of views among MPC members as to the pace of tightening, and we cannot rule out another three-, or even four-way, voting split among the committee at this month’s meeting. The BoE has a very delicate balancing act to contend with. On the one hand, UK inflation has continued to break to fresh four decade highs above 11%. On the other, there remains an acute degree of uncertainty surrounding the economic outlook, with the MPC warning in November that the longest UK recession on record was on the way.While we believe that a 50bp hike is highly likely on Thursday, we acknowledge that this is not necessarily guaranteed. Swap markets are fully pricing in a half a percentage point move with a non-negligible possibility of a 75bp hike (almost one-in-three). We even think that some of the doves will vote in favour of a ‘standard’ 25bp move, with a possibility that one or two could side in support of no change. We have outlined below the arguments in favour of both a smaller and larger increment rate hike this week, and our view of how each MPC member could vote.Arguments in favour of a larger base rate change

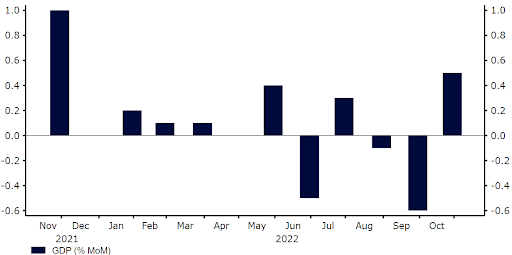

Unlike in some of the other major nations, notably the US, we are yet to see any signs of an easing in rates of UK inflation. The November CPI report will be released on Wednesday, with the headline measure of consumer price growth expected to break to fresh highs (11.5% consensus). Even in the event of a downside surprise here, inflation remains far too high for comfort and the BoE has made it clear that bringing down price growth continues to be the main priority. The IMF has warned that UK inflation will end 2023 above 7%, which they see as by far the highest in the G10.Since the November meeting, UK macroeconomic data has also held up rather well. The business activity PMIs have exceeded expectations and are only printing in modest contractionary territory, while the October GDP print showed solid growth. Tuesday’s labour report is also set to confirm that the jobs market remains healthy, characterised by low unemployment, high wage growth and a sizable mismatch between job vacancies and unemployed individuals.Figure 1: UK GDP Growth Rate (% MoM) (2021 - 2022)