12 December 2022

Last week’s currency rankings had an unusual couple on top: the Chinese yuan and the Swiss franc. The former was buoyed by the increasing signs that China is moving away from its zero-covid lockdown policy, whereas the latter appears to have finally caught a break after a few weeks of improving risk sentiment, as traders brace for another outsized interest rate hike from the Swiss National Bank this week. Moves in currencies and financial markets in general were, however, rather subdued as traders marked time ahead of this week's avalanche of central policy news. The Federal Reserve, European Central Bank and Bank of England will all hold their last policy meetings of the year in a period of fewer than 24 hours on Wednesday and Thursday. All three are once again set to deliver sizable rate increases, although we expect to see a moderation in the size of these hikes, with 50 basis point moves priced in across the board. In addition, the US and UK inflation numbers for November both come out just before their respective central bank meetings. The potential for a surprise either way in those reports that upset the narratives just before the meetings is an underappreciated risk, we think. Either way, get ready for some serious volatility in currency markets this week, particularly surrounding the aforementioned central bank announcements. Figure 1: G10 FX Performance Tracker [base: USD] (1 week)

The Bank of England meeting is now in sight and we, like everyone else, expect the MPC to raise the bank rate by another 50bps. The key will be the expected split within the MPC, i.e. how many members express a hawkish dissent in favour of a 75bp move and how many do so for a dovish 25bp hike. We think that an unprecedented four-way split is not out of the question either, with Silvana Tenreyro indicating recently that she could vote in favour of no change. The publication of key labour market and inflation data in the days leading up to the meeting do, however, make forecasting this week’s meeting an unusually difficult one.

The Bank of England meeting is now in sight and we, like everyone else, expect the MPC to raise the bank rate by another 50bps. The key will be the expected split within the MPC, i.e. how many members express a hawkish dissent in favour of a 75bp move and how many do so for a dovish 25bp hike. We think that an unprecedented four-way split is not out of the question either, with Silvana Tenreyro indicating recently that she could vote in favour of no change. The publication of key labour market and inflation data in the days leading up to the meeting do, however, make forecasting this week’s meeting an unusually difficult one. Another drop in global oil prices last week compounded the misery for CAD. With no domestic news on tap this week, we expect the currency to continue to be driven largely by developments in commodity markets and the Fed announcement on Wednesday.

Another drop in global oil prices last week compounded the misery for CAD. With no domestic news on tap this week, we expect the currency to continue to be driven largely by developments in commodity markets and the Fed announcement on Wednesday. Inflation data released last week also weighed on the krone. Norway’s inflation rate eased more than expected to 6.5% in November, from October's 35-year high 7.5%. Core inflation also fell to 5.7% from 5.9% in the previous month, perhaps an indication that rate hikes are beginning to filter through to weaker demand and price pressures. In light of this development, we see it increasingly unlikely that Norges bank will return to rate hikes of 50 basis points or more, and expect another ‘standard’ 25bp move at its Thursday’s policy meeting. The market expects this to be the last rate hike in the current cycle, so any indication that this may not be the case could be bullish for the currency.

Inflation data released last week also weighed on the krone. Norway’s inflation rate eased more than expected to 6.5% in November, from October's 35-year high 7.5%. Core inflation also fell to 5.7% from 5.9% in the previous month, perhaps an indication that rate hikes are beginning to filter through to weaker demand and price pressures. In light of this development, we see it increasingly unlikely that Norges bank will return to rate hikes of 50 basis points or more, and expect another ‘standard’ 25bp move at its Thursday’s policy meeting. The market expects this to be the last rate hike in the current cycle, so any indication that this may not be the case could be bullish for the currency.

GBP

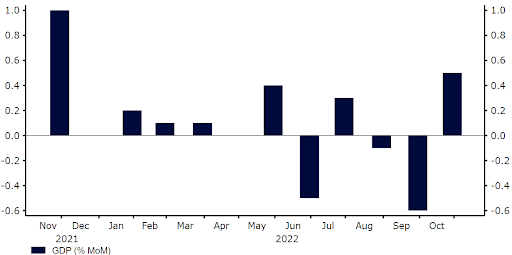

Sterling eked out yet another weekly gain last week against both the euro and the dollar, in a week almost completely lacking in major news, confirming that for now the path of least resistance for the pound is up. The pound was buoyed further this morning by strong GDP data for October, which showed a surprise expansion (+0.5%).Figure 2: UK GDP Growth Rate [% MoM] (2021 - 2022)The Bank of England meeting is now in sight and we, like everyone else, expect the MPC to raise the bank rate by another 50bps. The key will be the expected split within the MPC, i.e. how many members express a hawkish dissent in favour of a 75bp move and how many do so for a dovish 25bp hike. We think that an unprecedented four-way split is not out of the question either, with Silvana Tenreyro indicating recently that she could vote in favour of no change. The publication of key labour market and inflation data in the days leading up to the meeting do, however, make forecasting this week’s meeting an unusually difficult one.EUR

After an unusually quiet week in the Eurozone, all eyes turn to the December meeting of the ECB on Thursday. We expect the central bank to raise rates by 50bps, in line with consensus. We do, however, think that the gap between minimal market expectations for future hikes and economic reality is large, and we expect the communications from the ECB to push in a hawkish direction.The staff projections have (again) underestimated inflation, so we expect these to (again) be revised substantially higher, though (again) somehow future inflation will be expected to converge to the ECB target. However, the changes may not be dramatic and given the ECB’s track record, it is not clear whether anyone pays attention to these any more. Their impact could, therefore, be relatively muted. Overall, euro trading will depend as much, or more, on events across the Atlantic, particularly given the key inflation report will also be released out of the US.USD

The unusual juxtaposition between the November CPI release on Tuesday and the Fed meeting the next day will make for very volatile trading this week. The market is expecting a relatively mild outcome in the monthly number of less than 4% annualised inflation for both the headline and the core measures. An upside surprise here may be more upsetting than a downward one, as it would make it more difficult for the Fed to pivot towards a wait-and-see policy the next day.As for the Fed meeting, perhaps the key outcome will be the terminal rate that FOMC members expect to see in 2023, represented by the bank’s famous ‘dot plot’. Anything north of 5% could upend the positive narrative of the last few weeks, and provide some headwinds for the US dollar.JPY

The yen lagged behind most of its major counterparts last week, with the glaring omissions of the commodity-dependent currencies (NOK and CAD), despite some slightly better-than-expected economic news out of Japan. Last week’s Q3 GDP print beat consensus, though was still in line with a downturn. The Japanese economy contracted by 0.8% annualised in the three months to September according to the revised print, slightly stronger than the -1.1% priced in. A weak yen and uncertainties abroad do, however, continue to cloud the outlook, and a technical recession in 2023 remains a distinct possibility.Trade balance data (out on Wednesday) will be closely watched by market participants this week, though we suspect that the yen will be driven far more by the Fed’s announcement on Wednesday than any domestic news.CHF

In a rare turn, the Swiss franc outperformed all other G10 currencies last week. The franc’s volatility has, however, been limited and it ended the week little changed against the US dollar and the euro. After a rather uneventful week, we’re moving towards a hectic one, with the Swiss National Bank set to deliver another interest rate increase this week.We expect a 50bp hike from the SNB, which would take the policy rate to 1%, and the return to the initial pace of tightening following a jumbo 75bp move in September. We think that a slowdown in the pace of tightening is warranted given the decline in Swiss inflation, which has eased to 3% in the last two months. Aside from the rate decision itself, we’ll focus on the language on the franc and FX interventions, as well as the updated inflation forecast. All in all, the SNB will likely maintain its hawkish stance in the near-term, albeit we think that the bank will soon consider when to end the hiking process.AUDBoth the Australian and New Zealand dollars outperformed all of their major counterparts last week, with news of a relaxation in China’s zero-covid policy a disproportionately good developpement for the antipodean economies. The rally in AUD was, however, rather limited under the circumstances, particularly in light of the RBA’s moderately more hawkish than expected message following its policy meeting on Tuesday. The RBA raised rates by 25bps, no surprises there, though it did once again stress that it plans to continue hiking at future meetings - markets had braced for a softening in the bank’s forward guidance.The RBA has continued to indicate that future tightening will be contingent on macroeconomic data. This Thursday’s labour report and PMI figures will take on added importance, as investors weigh up whether the RBA will go again at its next policy meeting in February, or wait until the subsequent one in March.NZD

Similarly to AUD, the positive headlines out of China provided decent support for the New Zealand dollar, which advanced back above the $0.64 level towards the end last week. A pledge from PM Ardern that her government would prioritise the economy in 2023 has been the only real development of note in the the past few days. This lack of market news has led to minimal volatility in NZD - one month implied volatility in the NZD/USD pair fell to its lowest level since mid-September on Friday.We think that volatility should pick up markedly this week. Aside from the major central bank announcements elsewhere, Q3 GDP data will also be released on Wednesday.CAD

The BoC raised rates by 50bps during its policy meeting last Wednesday, more aggressive than priced in, although it signalled a potential pause in the hiking cycle by removing a commitment to raising interest rates at future meetings. The initial reaction in CAD was a positive one, as markets were only pricing in a rather modest chance of a half a percentage point hike, although the dollar found gains hard to come by and ended the week as one of the worst performers in the G10. Investors saw this tweak in communications as a signal that a pause in the hiking cycle may be on the way. Indeed, we think that future hikes now appear unlikely, barring a material blow up in inflation data.Figure 3: BoC Base Rate (2012 - 2022)Another drop in global oil prices last week compounded the misery for CAD. With no domestic news on tap this week, we expect the currency to continue to be driven largely by developments in commodity markets and the Fed announcement on Wednesday.SEK

In the absence of relevant data in Sweden last week, the Swedish Krona traded in line with risk assets. Trading in the EUR/SEK pair was choppy, although in the end, the krona ended last week virtually unchanged against the euro. Signs of division among policymakers in the Riksbank’s meeting minutes has further clouded the outlook, and provided no real clear direction for SEK.Volatility is expected to be high this week, as in addition to the ECB and Fed meetings, November inflation data will be released in Sweden. Both headline and core inflation are expected to increase from the previous month. Inflation is already at very high levels, so further signs of an upward trend could strengthen the case for the Riksbank to continue raising interest rates at an aggressive pace in the coming meetings and boost the currency.NOK

Last week, Brent crude oil prices fell below $80 for the first time since Russia's invasion of Ukraine, leading to a general underperformance in the commodity currencies. As a result, the Norwegian krone fell by more than 3.5% against the euro and was one of the worst-performers in the G10, alongside CAD.Figure 3: Brent Crude Oil Futures (2021 - 2022)Inflation data released last week also weighed on the krone. Norway’s inflation rate eased more than expected to 6.5% in November, from October's 35-year high 7.5%. Core inflation also fell to 5.7% from 5.9% in the previous month, perhaps an indication that rate hikes are beginning to filter through to weaker demand and price pressures. In light of this development, we see it increasingly unlikely that Norges bank will return to rate hikes of 50 basis points or more, and expect another ‘standard’ 25bp move at its Thursday’s policy meeting. The market expects this to be the last rate hike in the current cycle, so any indication that this may not be the case could be bullish for the currency.CNY

The Chinese yuan was a rare outperformer last week, posting substantial gains against most currencies as the country inched away from its zero-COVID policy. After an easing in restrictions on a local level, authorities are now lifting curbs nationwide. Most importantly, home quarantine will now be allowed and the QR health code will no longer be needed to visit most public places. This has given hope of an improvement in economic activity, especially in the services sector, which took a turn for the worse in November according to the latest PMI data. Last week’s export and import data also collapsed (-8.7% and -10.6% YoY in November respectively in dollar terms). Inflation remains low amid soft consumer demand, with prices increasing by only 1.6% last month, the slowest pace since March.Looking ahead we’ll continue to focus on economic data and COVID news. On Thursday, a set of hard data for November is scheduled for release. On that day, we’ll also keep an eye on the medium-term lending facility. Despite the subdued loan demand and low inflation, the MLF is expected to remain unchanged, and the focus should be on the rollover.Economic Calendar (12/11/2022 - 16/12/2022)