20 March 2020

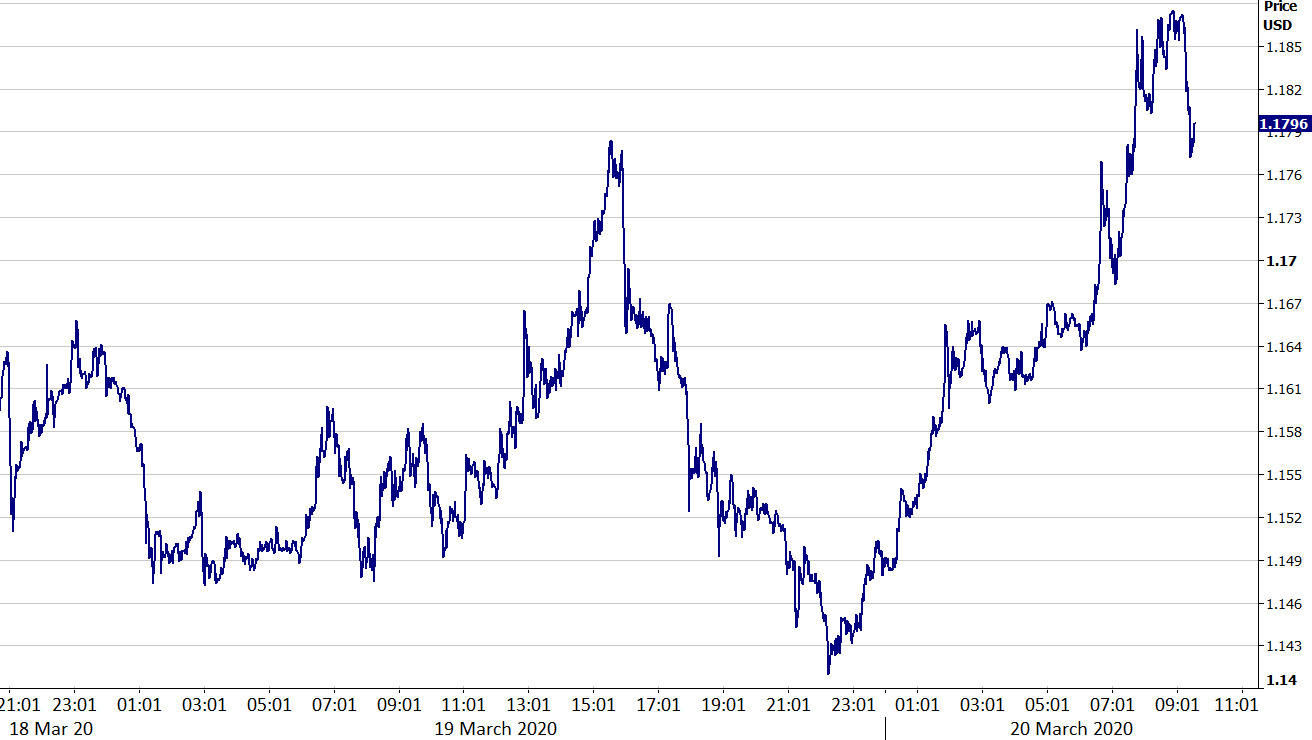

Monetary authorities around are continuing to battle hard to combat the economic risk posed by the coronavirus pandemic.As we mentioned in our afternoon note yesterday, the Bank of England cut interest rates to a record low 0.1%, an unprecedented 15 basis point rate cut, while also ramping up its QE programme by £200bn. Somewhat paradoxically, the initial reaction among investors was to send the pound sharply higher, up 2% in the immediate aftermath versus the dollar. Investors are now treating central bank action as a positive development, on hopes that their proactiveness can, at least to some extent, allay the economic impact to their respective domestic economies. In its statement, the bank noted that it will issue further guidance ‘in due course’. This to us suggests that even more stimulus is on the way on, or before, the next scheduled meeting on 26th March.But just as quickly as the pound rallied, it was sent sharply lower again soon after. The GBP/USD cross erased all of its gains for the day in late-afternoon London trading, as investors recommenced their flock to the safety of the dollar - briefly sending the pound to fresh 1985 lows. In yet another twist, the currency was on the front foot again this morning, soaring from around the 1.145 level versus the dollar to 1.19 in a matter of hours. News out this morning that the UK chancellor was planning to announce employment and wage subsidy packages later today may have been behind the move, although at this stage it is very hard to tell.Figure 1: GBP/USD (18/03 - 20/03) It is clear that the market is now in full-on panic mode, with the uncertainty surrounding the virus causing some violent and unprecedented moves in almost every currency. Volatility levels remain sky-high, with almost every duration of GBP implied volatility, somewhat incredibly, rising above June 2016 Brexit levels in the past few days (Figure 2).Figure 2: GBP Implied Volatility (2015 - 2020)

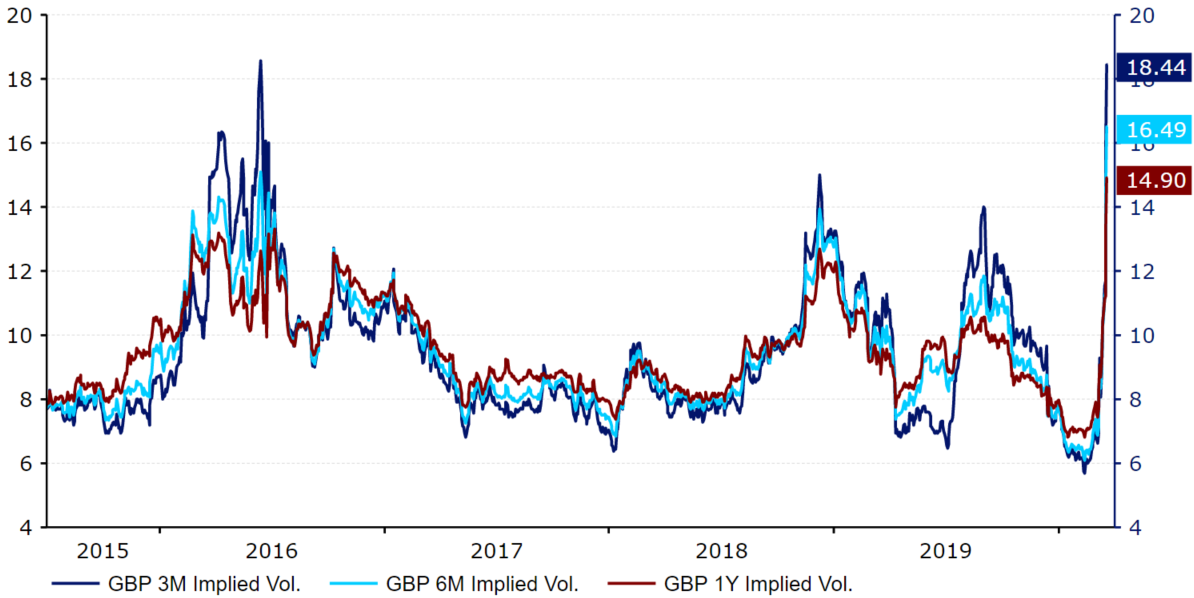

It is clear that the market is now in full-on panic mode, with the uncertainty surrounding the virus causing some violent and unprecedented moves in almost every currency. Volatility levels remain sky-high, with almost every duration of GBP implied volatility, somewhat incredibly, rising above June 2016 Brexit levels in the past few days (Figure 2).Figure 2: GBP Implied Volatility (2015 - 2020)

It is clear that the market is now in full-on panic mode, with the uncertainty surrounding the virus causing some violent and unprecedented moves in almost every currency. Volatility levels remain sky-high, with almost every duration of GBP implied volatility, somewhat incredibly, rising above June 2016 Brexit levels in the past few days (Figure 2).Figure 2: GBP Implied Volatility (2015 - 2020)