2 March 2020

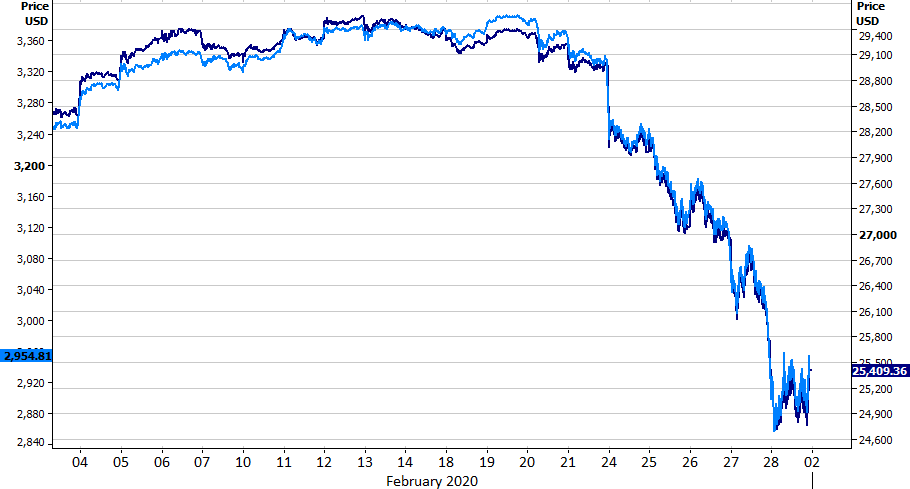

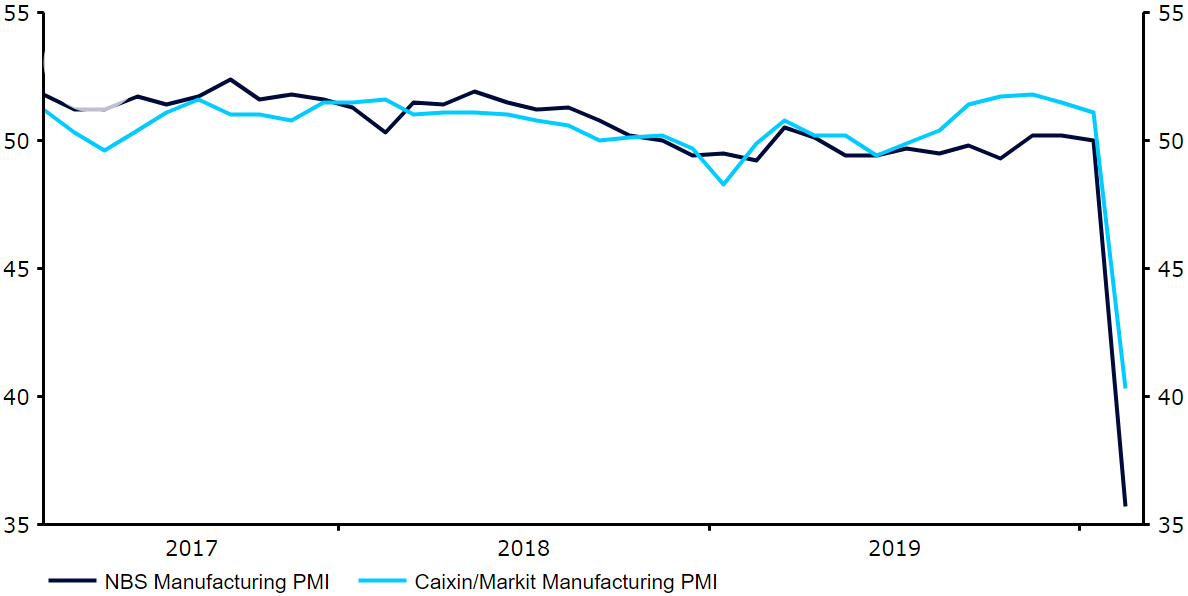

Escalating fears surrounding the coronavirus epidemic and the effect containment measures may have on the world economy sent stock markets worldwide sharply lower last week - the worst weekly sell-off since the crisis of 2008.Figure 1: S&P 500 and Dow Jones Indices (February 2020) The impact of the generalised flight to safety on FX markets was felt primarily in emerging markets, whose currencies sold-off hard against most G10 currencies. A curious exception was the Chinese yuan, which rose for the week as traders bet that the Chinese authorities have contained the epidemic. The euro had a strong week, which lends support to our view that its recent fall was due more to the establishment of "carry trades" that are now being unwound in a hurry.Three factors will drive currency markets this week. First, the daily drip of headlines about the expansion of the virus and any progress in its containment. Second, high-frequency economic data indicating the extent of the contraction in economic activity. Regarding the latter, the Chinese PMIs of economic activity released over the weekend were dire, showing easily the fastest pace of contraction since the data began in 2004 (Figure 2). Third, communication from central banks about the extent of monetary and credit easing markets can expect in response to the crisis. Expect plenty of volatility in markets.Figure 2: China PMIs (2017 - 2020)

The impact of the generalised flight to safety on FX markets was felt primarily in emerging markets, whose currencies sold-off hard against most G10 currencies. A curious exception was the Chinese yuan, which rose for the week as traders bet that the Chinese authorities have contained the epidemic. The euro had a strong week, which lends support to our view that its recent fall was due more to the establishment of "carry trades" that are now being unwound in a hurry.Three factors will drive currency markets this week. First, the daily drip of headlines about the expansion of the virus and any progress in its containment. Second, high-frequency economic data indicating the extent of the contraction in economic activity. Regarding the latter, the Chinese PMIs of economic activity released over the weekend were dire, showing easily the fastest pace of contraction since the data began in 2004 (Figure 2). Third, communication from central banks about the extent of monetary and credit easing markets can expect in response to the crisis. Expect plenty of volatility in markets.Figure 2: China PMIs (2017 - 2020)

The impact of the generalised flight to safety on FX markets was felt primarily in emerging markets, whose currencies sold-off hard against most G10 currencies. A curious exception was the Chinese yuan, which rose for the week as traders bet that the Chinese authorities have contained the epidemic. The euro had a strong week, which lends support to our view that its recent fall was due more to the establishment of "carry trades" that are now being unwound in a hurry.Three factors will drive currency markets this week. First, the daily drip of headlines about the expansion of the virus and any progress in its containment. Second, high-frequency economic data indicating the extent of the contraction in economic activity. Regarding the latter, the Chinese PMIs of economic activity released over the weekend were dire, showing easily the fastest pace of contraction since the data began in 2004 (Figure 2). Third, communication from central banks about the extent of monetary and credit easing markets can expect in response to the crisis. Expect plenty of volatility in markets.Figure 2: China PMIs (2017 - 2020)