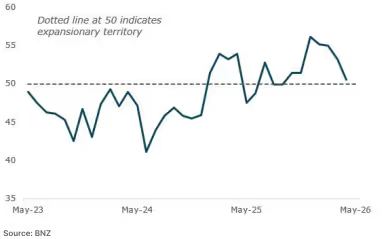

The kiwi was weaker last week, as USD caught a bid on the back ofhotter-than-expected US inflation data, with softer NZ domesticoutput and stalling US-Iran peace talks also adding further pressure tothe local currency.The BusinessNZ PMI eased to 50.5 in April from 52.8 in March,signalling that New Zealand's manufacturing sector is still expanding,but only marginally. Beneath the headline, employment and productionsub-indices held up, but new orders fell to their lowest since May 2025and deliveries of raw materials to their lowest since mid-2024 — bothpointing to meaningful headwinds for output ahead. The Iran conflict isweighing heavily, with 63.6% of respondents citing negative impactson business performance, centred on surging fuel and freight costs.Overall, the data reinforces our view that the NZ economy continues toface challenges, with weaker growth expected ahead.The Selected Price Index (SPI) for April provided little evidence thatinflation pressures are building further. Energy remained the dominantstory — petrol surged 12.6% mom while diesel rocketed 36.6%,reflecting the ongoing disruption from the Iran War. Electricity and gasalso rose meaningfully, up 2.4% and 0.3% mom respectively.Elsewhere, price pressures were contained — food was flat, alcoholicbeverages and tobacco fell 0.8%, and accommodation softened.Combined with the softer PMI, the data supports our view that theRBNZ should keep rates on hold later this month.The New Zealand housing market lost further ground in April. TheREINZ House Price Index fell 0.4% in seasonally adjusted terms, withannual price growth slipping to -0.9% from +0.3%, while sales volumesfell 2.7% mom to their lowest level since September. Despite tentativesigns of recovery in early 2026, the Iran conflict has undermined muchof that momentum. With weaker consumer confidence, softereconomic output, and the prospect of rate hikes later this year, theoutlook for the housing market remains challenging.

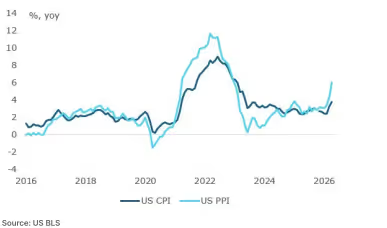

Offshore, the focus fell was on US inflation data for April, as US-Iranpeace talks seemed to stall. Headline CPI rose 0.6% mom, in line withexpectations, lifting the annual rate to 3.8% from 3.3%. Energy pricesjumped 3.8% — following a 10.9% surge in March — driven by the Iranconflict and the closure of the Strait of Hormuz. Shelter costs rose 0.6%(from 0.3%) and food prices climbed 0.5%. Core CPI came in slightlyahead of expectations at 0.4% mom, with the annual rate rising to 2.8%.More concerning, producer prices rose far stronger than expectedthrough April. US PPI surged 1.4% mom — well ahead of the 0.5%market expectation — pushing the annual rate to 6.0% from 4.3%, thelargest increase since December 2022. Goods prices jumped 2.0%mom, led by a 15.6% surge in gasoline, while services prices rose 1.2%mom. Core PPI was also strong, rising 1.0% mom against a 0.3%expectation, with annual growth lifting to 5.2% (from 4.0%). Import and export prices were also strong, rising 3.3% and 1.9% momrespectively in April. On the consumer side, retail sales were robust, up0.5% mom, with the control group - which feeds directly into GDPhousehold spending - also rising 0.5% mom. Taken together,broadening inflation pressures and resilient consumer spendingsuggests that the US economy is running stronger than most hadanticipated. Indeed, as a result, Fed rate expectations have repriced,with markets pricing in hikes by mid-2027. Overall, the dollarstrengthened sharply on the combination of the data and the resultinghawkish repricing.Additionally, President Trump and President Xi met in Beijing last week,agreeing to a "strategic stability" framework for the next three years, astrade envoys reached broadly positive outcomes. On the sidelines, theUS and China agreed to lower tariffs on some unspecified products topromote bilateral trade, per China's Commerce Ministry, which alsoconfirmed China's plan to purchase US planes and address USconcerns on agricultural imports. Trump invited Xi to visit the US inSeptember, though Xi issued a sharp warning over Taiwan.