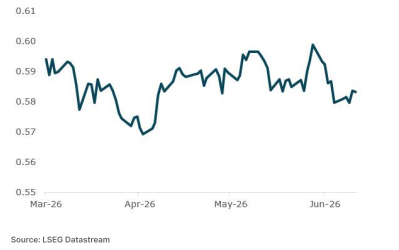

The kiwi had another volatile week, falling below 58 US cents for thefirst time in two months as US-Iran tensions flared before recovering toclose around 58.3 US cents, ending the week above where it opened asprospects of a peace deal lifted risk sentiment. Overall, the currencyexperienced sharp swings through the week, with movements largelydictated by geopolitical developments surrounding US-Irannegotiations.It was a quiet week on the local data front. The sole release of note wasthe Westpac NZ Retail Spending Pulse for May, which showed anothersoft month for the sector, with per-person card spending falling 0.3%month on month. The details pointed to continued pressure on the NZconsumer, with spending remaining skewed toward essentials as costof-living concerns persistLooking ahead, the key focus will be on the Q1 GDP release onThursday. Partial indicators pointed to decent momentum in the NZeconomy ahead of the Middle East conflict, with solid growth inhousehold spending and a bounce in manufacturing activity. We expectthe Q1 print to reflect this underlying strength. That said, the datalargely predates the fuel price surge and the broader economic impactof the Iran War. The more important question for the RBNZ is how theeconomy entered this volatile period and how well activity holds upthrough Q2 as the headwinds from the conflict feed through.

The USD continued to trade on a firmer footing this week, though itsurrendered some ground as risk sentiment improved on signs that aUS-Iran deal could come as soon as this weekend. The week wasdominated by Middle East developments, with oil prices swingingbetween $88-$98/bbl as the the situation moved between escalationand de-escalation in a matter of days. The trajectory of US-Iran negotiations proved highly volatile. Early inthe week, tensions surged after the US launched what it described asself-defence strikes against multiple targets in Iran, with PresidentTrump threatening to hit Iran hard, including seizing Kharg Island andtaking control of Iranian oil and gas infrastructure. Iran responded byannouncing the permanent closure of the Strait of Hormuz, drivingcrude prices sharply higher. The mood shifted materially later in the week. Trump cancelled theplanned further strikes, citing discussions with Iranian leadership, andsubsequently announced that final points of a potential deal had beenapproved by all parties involved, with a signing potentially as soon asthis weekend in Europe. Trump also noted that a secret US militarymission had enabled vessels carrying 100 million barrels of oil to exitthe Strait of Hormuz. However, Iranian news agencies had indicatedIran had not yet approved any agreement, leaving the situation stilluncertain.On the data side, the May CPI release was largely in in line at theheadline level, with headline inflation rising 0.5% MoM, lifting the annualrate to 4.2%. The rise was almost entirely an energy story, with energyprices rising 3.9% MoM. Core CPI, was a touch weaker than expected,rising 0.2% MoM and with the annual rate remaining at 2.9%. PPI datawas also released and showed headline producer prices rising sharply.PPI rose 1.1% MoM and lifting to 6.5% through the year. Core PPI,however, eased to 0.4% MoM, with the annual rate holding at 4.9%.Overall, while headline inflation remains elevated, the rise has largelybeen energy driven. Underlying inflation is more contained. Indeed, thislikely reflects weaker demand, limited pricing power and a fading tariffimpulse.Markets likely share this view. with market pricing for ratehikes by the Fed now having a 75% probability for a hike by year end(down from being fully priced earlier in the week).Away from the US, the ECB delivered a 25 basis point hike at its Junemeeting, lifting the deposit rate to 2.25% and becoming the first G3central bank to tighten since the Middle East conflict began. PresidentLagarde rejected the characterisation of the move as an insurance hike,framing it as standing on its own merits and drawing an explicit parallelto the bank's slow 2022 response. Markets are now pricing around a60% probability of a follow-up hike in July. The euro rallied on theannouncement before broadly stabilising.