The kiwi ended the week stronger, supported by the weaker US payrollsprint alongside building momentum into next week's RBNZ meeting,where markets are pricing a 76% probability of a hike. As noted in ourpreview last week, we continue to expect the Bank to deliver a hawkishhold rather than move on Wednesday, pausing before what we still seeas the start of a hiking cycle in September. Data released since the Maymeeting has been mixed and on balance supports patience overurgency. Q1 GDP pointed to an economy on solid footing heading intothe conflict, with household spending and business investment holdingup well, though the data only captured the first few weeks of disruption.Since then, higher frequency indicators have sent mixed signals, buthave largely skewed to the downside. This week's data reinforced the picture. ANZ business confidencerebounded sharply in June to 36.6 from 10.0, with own activityexpectations lifting to 36.9 as global tensions ease and oil prices fall,though activity gauges across trading, hiring and investment remainbelow pre-conflict levels. Pricing intentions softened to 50.7 from 56.7and inflation expectations eased to 3.36% (from 3.63%) - which stillremain elevated due to fuel costs, but are moving the right way.Consumer confidence echoed the improvement in sentiment, with theANZ Roy Morgan index rising by 4pts to 91.3. Interestingly, the time tobuy a major household item index, the best forward indicator forspending, rose 9pts to -11, which suggested a still weak but improvingoutlook for household spending. Most encouraging for the inflationoutlook, two year household inflation expectations fell to 4.6% from5.3%, back to levels last seen before the oil price spike.Again as highlighted in our preview, the recent easing in inflationarypressures will likely see Q2 CPI print coming below the RBNZ's May MPSforecast of 1.6% QoQ/4.2% YoY. We continue to expect the RBNZ to startits hiking cycle in September, followed by a further move in October andone more in February 2027, taking the OCR to 3.0%. This is a moredovish path than the market's current pricing, which expect four hikesby September 2027, bringing the OCR to 3.25%. We see the June quarter CPI print, due 21 July, as the key data point theCommittee will want to see before acting, with the case for anaggressive hiking cycle having weakened as energy prices fall fasterthan feared and second round inflation risks look more contained. Atnext week's meeting we expect forward guidance to remain consistentwith further hikes later this year, but with a tone that reads as more datadependent than in May.

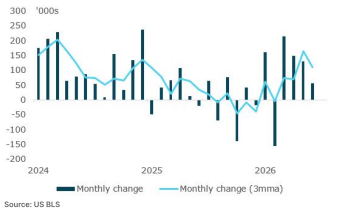

Globally, the key focus was US labour market data. June non-farmpayrolls rose just 57k through the month, well below expectations of114k. This also came a large 74k downward revision to the prior twomonths (with May jobs growth revised down to 129k from 172k). Addingto this, the three month average payroll growth has slowed sharply,easing to 111k (from 164k). And whilst the the unemployment rate fell to4.2% (from 4.3%), though this reflected a 0.3% drop in the participationrate to 61.5%, a 50 year low, rather than labour demand strength. Education and healthcare remain the key drivers of job growth, whilelosses were concentrated in leisure and hospitality, retail, andinformation. Fed pricing eased modestly on the data, with marketspricing around 30bps of hikes by year end, down from 36bps prior to thedata release. The US dollar also retreated off the back of the softer data. The soft report supports our call for no Fed rate hikes this year and agradual downward trend in the dollar over our forecast horizon, thoughthe labour market remains better described as a low fire, low hire, ratherthan being genuinely strong. Adding to this, energy prices havestabilised, with oil prices stabilising, which should limit inflationarypressure in the second half of the year and keep second round effectscontained, a dynamic already visible in core inflation measures. Indeed,this was evident in June Euro area inflation data, where both headlineand core measures came below expectations and surprised to thedownside, as headline inflation eased to 2.8% from 3.2% and moreimportantly, core inflation eased to 2.4% from 2.6%.In the Middle East, the situation remains uncertain despite reportedlypositive US Iran talks, though oil flows continue to normalise. Oil marketsreflected this modest improvement, with brent crude prices easing to aslow as $71/bbl. Strait of Hormuz traffic has also continued to recover,with Bloomberg ship tracking data showing 14 million barrels transitingthe waterway on 1 July and Saudi oil flows back to around 90% of preFebruary levels. Iran, however, is struggling to find buyers for its oildespite the sanctions waiver, with limited demand from major Asianrefiners weighing on its ability to capitalise on the relief.