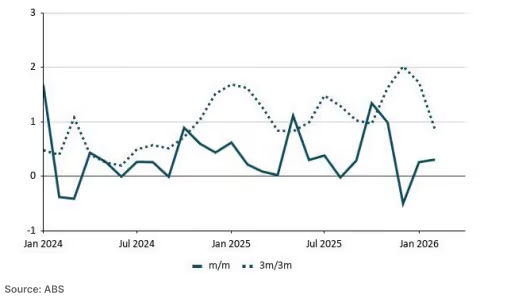

Locally, last week the data calendar was light, with the focus on theFebruary ABS household spending indicator. Nominal spending rose amodest 0.3% m/m, supported by recreation and food retailing. Whileannual spending edged up to 4.6% y/y, quarterly momentum eased, with3m/3m growth slowing to 0.9% from 1.7% in January. Although this datawas largely overlooked in favour of geopolitical headlines, it establishes asoftening baseline for domestic demand prior to the conflict's full impact.

However, AUD opened 0.6% lower this morning, trading around 0.702USD, following the collapse of weekend negotiations in Islamabad. Talksbroke down after Iran refused to abandon its nuclear weaponsprogramme, prompting President Trump to announce a full navalblockade of the Strait of Hormuz. Iran has since warned that anyapproaching military vessels will be treated as a ceasefire violation. Thisescalation has effectively erased the "truce premium," with AUD nowtightly bound to further Middle Eastern developments.

Looking ahead, Thursday’s March labour force survey will be the firstofficial read on how the conflict is impacting the local economy.Furthermore, sentiment surveys from WMI and NAB will offer timelyinsights into how Australian households and firms are navigating thecurrent geopolitical challenges. Until then, the local currency will remainhighly sensitive to any further escalations or diplomatic headlines fromthe Middle East.

Download the Full Report Here.