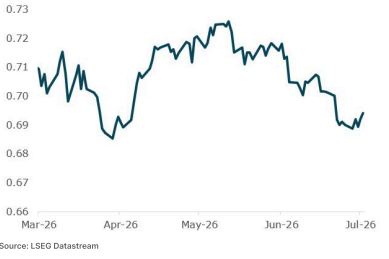

The Aussie improved modestly through the week, largely driven byweaker than expected US labour market data rather than domesticdevelopments.Locally, the key focus was the RBA minutes, which confirmed a hawkishrisk bias despite the Board's decision to hold. The minutes showed theBoard views the economy as running with excess demand and persistentinflationary pressures, with underlying inflation expected to rise furtherin the second quarter. The activity slowdown was deemed "as expected",while financial conditions were judged "somewhat restrictive" though theBoard is still assessing the full impact. The labour market has softened a little and the housing market is easingmore than expected, but the Board appears tolerant of this given theinflation outlook. Risks were skewed hawkish overall, with the MiddleEast conflict still viewed as an upside inflation and downside growth risk,and weak productivity a further threat, partly offset by downside riskfrom housing. The statement, however, did reiterate a willingness to hikefurther "if necessary". Separately, housing data confirmed the slowdown the Board flagged,with national house prices down 0.4% MoM in June and down 0.7% overthe June quarter. While the RBA doesn't target house prices directly, itdid note concern in the minutes about the risk of a material weakening inhousing markets inhibiting consumption growth, which is one reason wesee limited scope for a sharp correction. In our view, this likely suggeststhat a material downturn in dwelling prices would more likely bringforward rate cuts than validate them. We hold our view that the RBA remains comfortably on hold for theremainder of 2026 and into 2027, before cutting rates by mid-2027.

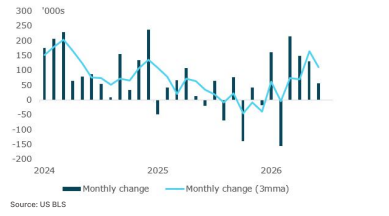

Globally, the key focus was US labour market data. June non-farmpayrolls rose just 57k through the month, well below expectations of114k. This also came a large 74k downward revision to the prior twomonths (with May jobs growth revised down to 129k from 172k). Addingto this, the three month average payroll growth has slowed sharply,easing to 111k (from 164k). And whilst the the unemployment rate fell to4.2% (from 4.3%), though this reflected a 0.3% drop in the participationrate to 61.5%, a 50 year low, rather than labour demand strength. Education and healthcare remain the key drivers of job growth, whilelosses were concentrated in leisure and hospitality, retail, andinformation. Fed pricing eased modestly on the data, with marketspricing around 30bps of hikes by year end, down from 36bps prior to thedata release. The US dollar also retreated off the back of the softer data. The soft report supports our call for no Fed rate hikes this year and agradual downward trend in the dollar over our forecast horizon, thoughthe labour market remains better described as a low fire, low hire, ratherthan being genuinely strong. Adding to this, energy prices havestabilised, with oil prices stabilising, which should limit inflationarypressure in the second half of the year and keep second round effectscontained, a dynamic already visible in core inflation measures. Indeed,this was evident in June Euro area inflation data, where both headlineand core measures came below expectations and surprised to thedownside, as headline inflation eased to 2.8% from 3.2% and moreimportantly, core inflation eased to 2.4% from 2.6%.In the Middle East, the situation remains uncertain despite reportedlypositive US Iran talks, though oil flows continue to normalise. Oil marketsreflected this modest improvement, with brent crude prices easing to aslow as $71/bbl. Strait of Hormuz traffic has also continued to recover,with Bloomberg ship tracking data showing 14 million barrels transitingthe waterway on 1 July and Saudi oil flows back to around 90% of preFebruary levels. Iran, however, is struggling to find buyers for its oildespite the sanctions waiver, with limited demand from major Asianrefiners weighing on its ability to capitalise on the relief.