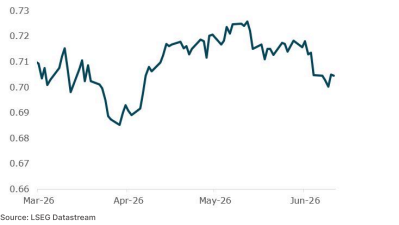

The Aussie dollar had a volatile week, falling below 70 US cents as USIran tensions escalated before recovering to close the week modestlyhigher at 70.4 US cents as prospects of a peace deal being signed assoon as this weekend lifted risk sentiment. The net move on the weekwas modest, but the intra-week swings were sharp, reflecting the fluidgeopolitical backdrop described above.On the domestic front, it was a quiet week for data. Consumer sentimentdeteriorated further in June, with the WMI index falling 2.9% to 80.6, nearits weakest level on record. Pessimists now outnumber optimists bynearly 20%, with cost-of-living pressures and higher rates continuing toweigh on household finances. A sharp fall in house price expectationsalso suggests some households are growing uneasy about the impact ofrecently announced tax changes alongside the RBA's recent rate hikes. NAB's business survey offered a modest reprieve, with confidencerebounding to -14 from -24 in April, though the index remains deeplynegative and well below long-run averages. Business conditions werebroadly unchanged, and despite the confidence bounce, the surveypoints to an extremely cautious outlook among firms. On a brighter note,purchasing costs eased, likely reflecting the recent decline in fuel pricesamid improved near-term oil supply.Looking ahead, the key local focus will be on the RBA meeting onTuesday and May labour force data Thursday. As outlined in our preview,the cash rate is widely expected to be held at 4.35%, a view we share.While headline inflation is set to move higher in the near term, the Boardis likely to look through this given the broader softening in growth andlabour market conditions since the May meeting. Markets will be focusedon the post-meeting statement, and we expect the Board to strike acautious tone. Any hawkish signal would likely provide a near-term lift tothe Aussie, though we see this as unlikely given the weight of evidencepointing to a soft domestic backdrop. Looking further out, we continue toexpect the cash rate to remain at 4.35% this cycle, with the next movebeing a cut in 2027.

The USD continued to trade on a firmer footing this week, though itsurrendered some ground as risk sentiment improved on signs that aUS-Iran deal could come as soon as this weekend. The week wasdominated by Middle East developments, with oil prices swingingbetween $88-$98/bbl as the the situation moved between escalationand de-escalation in a matter of days. The trajectory of US-Iran negotiations proved highly volatile. Early inthe week, tensions surged after the US launched what it described asself-defence strikes against multiple targets in Iran, with PresidentTrump threatening to hit Iran hard, including seizing Kharg Island andtaking control of Iranian oil and gas infrastructure. Iran responded byannouncing the permanent closure of the Strait of Hormuz, drivingcrude prices sharply higher. The mood shifted materially later in the week. Trump cancelled theplanned further strikes, citing discussions with Iranian leadership, andsubsequently announced that final points of a potential deal had beenapproved by all parties involved, with a signing potentially as soon asthis weekend in Europe. Trump also noted that a secret US militarymission had enabled vessels carrying 100 million barrels of oil to exitthe Strait of Hormuz. However, Iranian news agencies had indicatedIran had not yet approved any agreement, leaving the situation stilluncertain.On the data side, the May CPI release was largely in in line at theheadline level, with headline inflation rising 0.5% MoM, lifting the annualrate to 4.2%. The rise was almost entirely an energy story, with energyprices rising 3.9% MoM. Core CPI, was a touch weaker than expected,rising 0.2% MoM and with the annual rate remaining at 2.9%. PPI datawas also released and showed headline producer prices rising sharply.PPI rose 1.1% MoM and lifting to 6.5% through the year. Core PPI,however, eased to 0.4% MoM, with the annual rate holding at 4.9%.Overall, while headline inflation remains elevated, the rise has largelybeen energy driven. Underlying inflation is more contained. Indeed, thislikely reflects weaker demand, limited pricing power and a fading tariffimpulse.Markets likely share this view. with market pricing for ratehikes by the Fed now having a 75% probability for a hike by year end(down from being fully priced earlier in the week).Away from the US, the ECB delivered a 25 basis point hike at its Junemeeting, lifting the deposit rate to 2.25% and becoming the first G3central bank to tighten since the Middle East conflict began. PresidentLagarde rejected the characterisation of the move as an insurance hike,framing it as standing on its own merits and drawing an explicit parallelto the bank's slow 2022 response. Markets are now pricing around a60% probability of a follow-up hike in July. The euro rallied on theannouncement before broadly stabilising.